|

|

|

September 15th, 2008 at 12:57 pm

For the past several weeks, I have had an overwhelming sense of thankfulness. I am so blessed that it is hard to put it into words.

Here are some random things for which I am thankful:

* My healthy family

* The opportunity to run a marathon - not everyone has the health to even attempt one

* An emergency fund and the peace it brings to my family

* Great friends - I have met so many cool people through this crusade to help others with their personal finances

* HOPE

* Opportunity

* My friend who was diagnosed with cancer has been given a clean bill of health

* Being able to participate in life-changing work and the FLE, FFE, IWBNIN, Money Help, and other resources that help make the life-change possible.

* Volunteers who help me with this crusade. There are literally dozens of people who make this thing work.

* NewSpring Church

* Two paid-for cars that run well.

* A wife who participates in the budgeting process.

As I look at this list, I realize that many of them are interconnected. Many of them could not exist alone. But I can tell you this, as I wrote this list, my heart overflows with thankfulness, and I am overwhelmed. I simply can not believe I get to do this stuff for a living.

If you were to take three minutes to write down what you are thankful for, what would you write?

Posted in

Uncategorized

|

2 Comments »

September 11th, 2008 at 05:36 pm

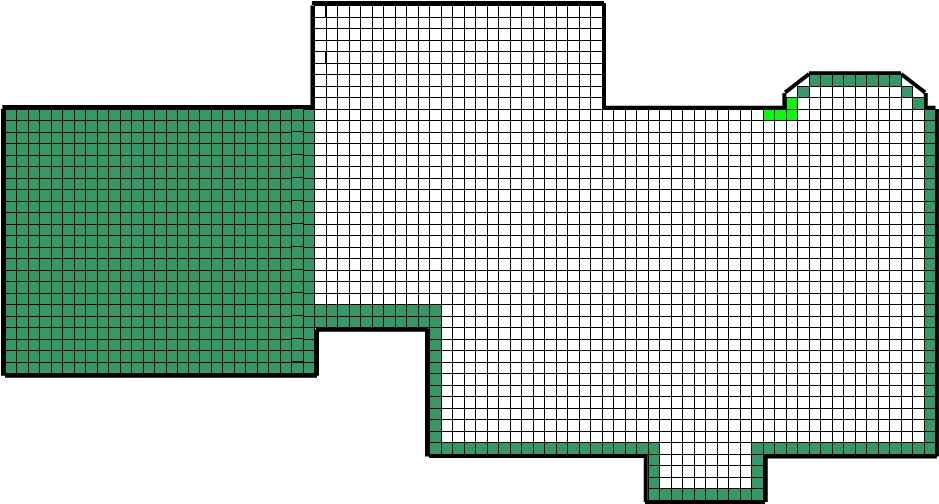

As I look at my Sangl Family Home Pay-Off Spectacular, I get the very real feeling that I am mowing my lawn. (Click on the image below to see the actual spectacular.)

I am working along the outside perimeter of the house to ensure that we own at least all of our exterior walls. It makes me feel like I am mowing the lawn. I always start by mowing the outside perimeter and then work toward the center. I am certain that this is a mental game that I play, but here is why I mow my lawn with this technique (and color in the squares on the Sangl Family Home Pay-Off Spectacular).

* I want the longest and hardest part to be done first.

* As I work toward completion, the time to complete each complete pass is shorter.

* This method helps me see that I am making progress with every pass that I make.

Have you ever mowed your lawn for months or years with a small push mower and then had the opportunity to mow it with a riding mower that had a 48" deck? All of the sudden, the push mower seems totally puny and inferior. That is EXACTLY what it has felt like to slow down on our mortgage pay-off for the past six months. It felt like I had to jump off of the riding mower and start push mowing again. I am PUMPED to know that we are again back on the riding mower starting this month!

What techniques are you using to color in your Spectaculars?

If you do not have a Pay-Off or Saving Spectacular, click Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE to peruse the different ones available.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Home Pay-Off Spectacular

|

1 Comments »

September 9th, 2008 at 05:42 pm

In keeping with the completely PRACTICAL nature of this website, I thought I would provide some important reminders.

* Christmas is 107 days away

* Car tires wear out

* Water heaters fail

* Kids grow

* Debt freedom is worth every sacrifice it took to achieve

* Third-graders will enter college in ten years

* Wives appreciate nice anniversary gifts - especially the years that have multiples of 5

* Property taxes are known, upcoming expenses for those who own property

* Income is necessary to make Income - Outgo = Exactly Zero

* Payday loans are destructive to one's finances

* Purdue University did not lose a football game last week

* It is now nine days into September. Did you prepare a written budget BEFORE the month began?

What other reminders do you have?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

September 8th, 2008 at 02:59 pm

Pardon me while I rant for a moment �

For some reason, I have been encountering a lot of people lately who simply can not believe that they can become debt free.

They present numerous reasons as to why they can not become debt free - income, uncooperative spouse, children, huge home mortgage, student loans, interest rates on various loans, and the fact that it takes too long.

I agree that all of these reasons can create obstacles to achieving debt freedom, but NONE has the ability to prevent you from becoming debt free. ALL of them can be addressed. ALL of them might require tough, hard, and gut-wrenching decisions, but it is worth it to become free from debt!

If freedom from debt is your goal, you CAN do it! I believe that one of the most important things one can do when launching their Debt Freedom March is to prepare a written spending plan every single month.

If today is the day that you are going to start planning your spending, I recommend that you read the series of posts I wrote titled Text is "How Do I Budget?" and Link is http://www.josephsangl.com/category/series/how-do-i-budget-series/ "How Do I Budget?".

Chances are that if you have already launched your March To Debt Freedom, you have encountered the naysayers who say it is not possible. Stick with it! It is so worth it.

In summary, let me just say that I have been Debt-Free (Text is except for the house and Link is http://iwasbroke.savingadvice.com/series-home-pay-off-spectacular/ except for the house) and LOVING IT since February 2004.

Posted in

Uncategorized

|

0 Comments »

September 3rd, 2008 at 02:32 pm

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

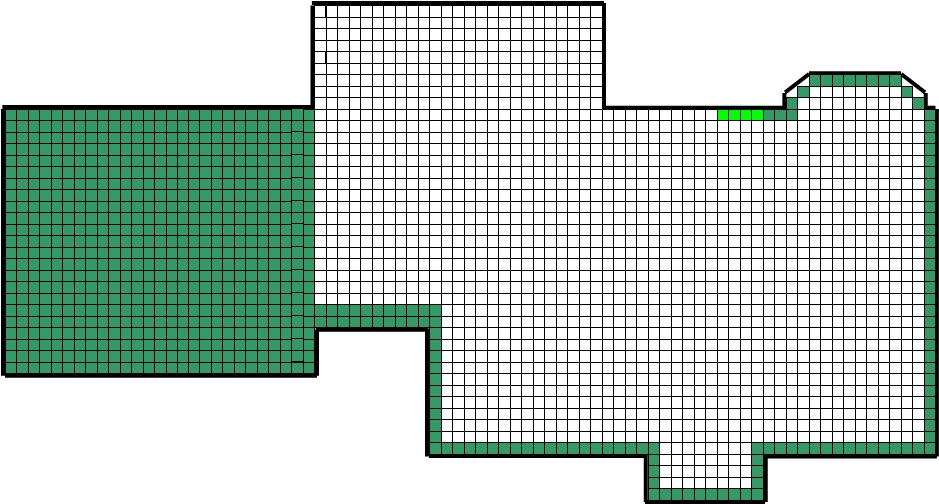

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 752 IS 756

Squares Remaining: WAS 1674 IS 1670

% of House Owned By The Sangl's: WAS 31.0% IS 31.2%

% of House Owned By Wells Fargo: WAS 69.0% IS 68.8%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger, cleaner version)

Next month, we are ramping up on the payoff spectacular again. After several months of backing off the attack on our mortgage, it looks like we will be able to sustain larger payments for the forseeable future. I am PUMPED to be able to start coloring in more squares every month!

At least eleven squares are going to be colored in this coming month due to the Text is FNBO Direct semi-finalist prize money and Link is http://iwasbroke.savingadvice.com/2008/08/11/i-can-not-believe-this_42044/ FNBO Direct semi-finalist prize money!

How are you doing on YOUR house payoff spectacular? Don't have one? Get yours here => Text is Pay Off Spectacular - House and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=14 Pay Off Spectacular - House.

Read previous Text is Sangl Home Pay-Off Spectacular Updates and Link is http://iwasbroke.savingadvice.com/cpanel/category_edit.php?category_id=3121 Sangl Home Pay-Off Spectacular Updates

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Home Pay-Off Spectacular

|

0 Comments »

September 2nd, 2008 at 12:12 am

I am not sure why I am doing this again, but I have signed up for another full marathon. That is 26.2 miles of nonstop running. That is 26.2 MILES. That is a 10K race PLUS 20 more miles!

I decided to re-read Text is THIS POST and Link is http://www.josephsangl.com/2006/05/30/how-a-marathon-is-like-personal-finances/ THIS POST I wrote before I ran my first full marathon back in June 2006. I found myself saying "Amen." and "Absolutely." as I read that post. (Sidenote: Is it OK to do that for stuff you have written yourself?)

On Sunday, January 18, 2009 @ 7:00AM, I will embark on another marathon with 18,000 runners in the Chevron Houston Marathon in Houston, TX. The great thing is that I will have two brothers running with me (the other three are slackers). If, strike that, WHEN we all finish, we are going to Ruth's Chris Steakhouse for a fine celebration meal.

There are so many parallels between marathon training and personal finances. Not the least of which is self-discipline. Look for a ton of posts focused on my training and how I feel that it relates to personal finances over the next several months.

I have started training several months ago, but the formal training program begins September 15th.

I ran my last marathon in 4 hr 27 min 35 sec. My goal this time? 4 hr 10 min 00 sec

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

3 Comments »

August 31st, 2008 at 01:29 pm

Jenn and I budget every single month. We spend all of the money we expect to receive in the upcoming month in the Text is Monthly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=1 Monthly Budget Form (Excel) and AGREE on how that money will be spent.

THAT is the easy part. The hard part is following the plan for the entire month - especially at the end of the month.

It is easy to follow the budget at the start of the month because I have spending money, we have grocery money, we have dining out money, and we have entertainment money.

But as we arrive at the end of the third week and the start of the fourth week, it is not so glorious of a picture. You can bet that I have spent every dime of my spending money. The dining out fund is at or near zero. The grocery envelope is tapped out, and the entertainment envelope has kicked the bucket as well.

That is our story nearly every single month of the 62 consecutive months that we have planned our spending. Yet we stick with the budget, and it is where I see a ton of people fall off of the wagon.

How do we ensure that we stick to our plan? We hold each other accountable. We KNOW that if we spend more than we planned on these fun categories, then that extra money will be taken from another fund like vacation, Christmas, car repairs, retirement savings, or college savings. We simply refuse to mortgage our future just so we can have a little extra fun today.

That is HOW we stick to our plan and that is WHY we stick to our plan.

I would love to hear from others on HOW you ensure that you stick to your plan and WHY. Start the conversation in the comments below!

Posted in

Uncategorized

|

2 Comments »

August 30th, 2008 at 11:59 pm

Many of you know that I have a house cat named Kiki. My daughter was given this nice kitty cat four years ago for Christmas, and it has been a great cat.

Until we moved back to South Carolina and bought an older home. An older home that used to have other animals in it. The smell of the other animals has ignited the stupid instinct to spray and mark its territory.

The cat has peed all over the tile floor of the laundry room. It has peed all over a box of shipping envelopes for my book. (Don't worry - I threw them away.)

It has pooped all over the new carpet. And we decided that the cat was going to get ONE MORE CHANCE to stop being instinctive with its pooping and peeing.

Well, it seemed as if our cat was behaving and things have went OK for a couple of months.

Let me stop that story to introduce a new storyline.

A new kitten showed up on our back deck two weeks ago. It was emaciated with its ribs sticking out and it had no tail. Melea immediately fell in love with it and started nursing it back to health. Me, being the sucker that I am, agreed that after a trip to the vet this new kitten could move in with us last Thursday.

Last Wednesday, the day before the kitten was going to move in, Jenn discovered that Kiki had been spraying FOR MONTHS in an undiscovered area. The undiscovered area? On our brand new carpet and TWO BOXES OF I Was Broke. Now I'm Not.!!!!!! Now, I know some budget-haters would love to do what Kiki has done, but THAT WAS IT.

Kiki has been kicked outside. The new kitten is not being allowed in the house. I wanted to see if Kiki could fly through the floor at a very high rate of speed, but I kicked her out instead.

In spite of ALL of that, this was still a very hard decision. You see, Kiki slept next to Melea every single night. Snuggled right up next to her, purring so nicely. Ever since Melea can remember, Kiki has been bounding around the house with her. Now, Kiki sits outside in tropical storm Faye, meowing forlornly and totally confused as to why she can not come inside.

In spite of the fact that the stupid cat had ruined two boxes of books. In spite of the fact that our new carpet smells like cat pee. In spite of the fact that it had sprayed an entire box of shipping envelopes. In spite of the tremendously annoying damage, it was still a very difficult decision.

It made me pause. This situation helps me understand just a little bit more why some people can not bring themselves to make the decisions necessary for them to win with their money. They KNOW that the car payments are peeing all over their ability to gain financial traction. They KNOW that the credit cards need to be chopped up because they are stinking up their ability to win with money. They KNOW that their finances are continually being trashed because they are unwilling to make a tough decision.

Folks - throwing out your eight year old daughter's cat is a difficult decision. So is selling a car and taking a second job. But I will tell you this - the relief I feel now that the decision has been made is AWESOME!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

5 Comments »

August 28th, 2008 at 05:39 pm

Welcome to the latest series - Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Text is Part One - Know What You Are Paying and Link is http://iwasbroke.savingadvice.com/2008/08/19/series-restructuring-debt-part-one_42322/ Part One - Know What You Are Paying

Text is Part Two - Lower The Interest Rates! and Link is http://iwasbroke.savingadvice.com/2008/08/20/series-restructuring-debt-part-two_42370/ Part Two - Lower The Interest Rates!

Text is Part Three - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/21/series-restructuring-debt-part-three_42420/ Part Three - Lower The Interest Rates! - Continued

Text is Part Four - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/24/series-restructuring-debt-part-four_42511/ Part Four - Lower The Interest Rates! - Continued

Text is Part Five - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/25/series-restructuring-debt-part-five_42529/ Part Five - Lower The Interest Rates! - Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, it was the debt consolidation option. In Part Five, it was the credit score option. In Part Six, I will be sharing my most favorite way to restructure debt.

Part Six - CRUSH IT, SMASH IT, HAMMER IT, DESTROY IT

I used to be broke. I used to have $4.13 in my bank account after paying all of my bills, and I was pumped because it was a positive balance. Yet, I was sending hundreds of dollars every single month to banks for debt. I finally experienced my I Have Had Enough Moment (IHHE Moment) and attacked my debt.

I know that the interest is annoying. I know that trying to get the lenders to lower their interest rates is frustrating and humiliating. Besides that - much of that is out of our control. But controlling how we spend our money from now on IS in our control. Not signing up for more debt IS in our control. Going to work for sixteen hours a day to eliminate our debt superfast IS in our control. Selling our car, boat, truck, collectibles, and other niceties IS in our control. No, it might not be fun, but paying hundreds and thousands of dollars a year in interest is MISERABLE and robs us of the ability to go do EXACTLY what we have been put on this earth to do!

So I end this series with two questions and their answers.

Q: How much interest do you have to pay when you have zero debt?

A: ZERO

Q: How much interest is paid to you when you have money in the bank or invested?

A: Anywhere from 3% to 12% or more! Paid TO you! I decided long ago to choose to have interest paid to me instead of paying it to someone else.

I trust that this series has helped you.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 26th, 2008 at 06:11 pm

I am PUMPED to hear how people are applying the Total Interest Tool taught in Part One of the

Text is Restructuring Debt and Link is http://iwasbroke.savingadvice.com/series-restructuring-debt/ Restructuring Debt series.

I would love to see how you are using the tool to formulate your plan of attack for restructuring your debt and gaining traction for your Debt Freedom March!

For example, Kings Pray has blogged about how he used the Total Debt Interest tool. You can read that post Text is HERE and Link is http://kingspray.wordpress.com/2008/08/13/joe-sangl-starts-a-new-series-restructuring-debt/ HERE. Be sure to click on the link in the blog that actually shows the tool with his Total Debt Interest calculation. I love transparency and people being real.

If you blog about it, please comment below and provide a link to your post.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 25th, 2008 at 01:14 pm

Welcome to the latest series - Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Text is Part One - Know What You Are Paying and Link is http://iwasbroke.savingadvice.com/2008/08/19/series-restructuring-debt-part-one_42322/ Part One - Know What You Are Paying

Text is Part Two - Lower The Interest Rates! and Link is http://iwasbroke.savingadvice.com/2008/08/20/series-restructuring-debt-part-two_42370/ Part Two - Lower The Interest Rates!

Text is Part Three - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/21/series-restructuring-debt-part-three_42420/ Part Three - Lower The Interest Rates! - Continued

Text is Part Four - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/24/series-restructuring-debt-part-four_42511/ Part Four - Lower The Interest Rates! - Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, it was the debt consolidation option. In Part Five, I will be covering the credit score option.

Credit Scores Matter!

I know. I am brilliant. But it matters so much when it comes to reducing the interest that lenders will charge on your existing debt (this is a no-new-debt zone!). As your credit score improves, your credit card surfing and bill consolidation loan options will improve.

There is a company that actually specializes in consolidating loans for people with excellent credit. I was told about this company by a banker friend who has been extremely impressed with the way this company is doing business. It is called Text is FirstAgain.com and Link is http://www.firstagain.com/ FirstAgain.com. It is actually stated on their web site that "Excellent and Substantial Credit Required". No need to apply if you have trashed credit, but it looks like a good option for those who are looking restructure their debt and gain traction with their Debt Freedom March.

Of course, there are also companies that specialize in loans for people with horrible credit. Payday loan joints, title loan sharks, pawn shops, and various other organizations provide loans that have HORRIFIC interest and should never be considered a viable option for someone who expects to gain traction on their Debt Freedom March. I have yet to meet the first person who became debt free because of their rip-off payday loan. I have met hundreds who have became completely hopeless because of their rip-off payday loan.

In the sixth and final installment of the Restructuring Debt series, I will be sharing my favorite way to restructure debt.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 25th, 2008 at 01:22 am

Welcome to the latest series - Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Text is Part One - Know What You Are Paying and Link is http://iwasbroke.savingadvice.com/2008/08/19/series-restructuring-debt-part-one_42322/ Part One - Know What You Are Paying

Text is Part Two - Lower The Interest Rates! and Link is http://iwasbroke.savingadvice.com/2008/08/20/series-restructuring-debt-part-two_42370/ Part Two - Lower The Interest Rates!

Text is Part Three - Lower The Interest Rates! - Continued and Link is http://iwasbroke.savingadvice.com/2008/08/21/series-restructuring-debt-part-three_42420/ Part Three - Lower The Interest Rates! - Continued

Part Four - Lower The Interest Rates! - Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, I will be covering the debt consolidation option.

Debt Consolidation/Home Equity Loan

Another option to consider is to visit your local bank or credit union with your current debts and interest rates and see what they can do to lower your interest rates. Be careful with this, though. Banks are very likely to try to get you to use your home equity to consolidate your higher interest debts. If used properly, this can be a good thing because you are probably going to be able to deduct the home equity loan interest from your taxes.

But one thing that I see way too often is the fact that folks will consolidate their debts using their home equity and then NOT change their financial behavior that led to the debt in the first place. The results? A mortgage, home equity loan, AND the high interest debts have showed back up. My advice is to prove to yourself that you truly have changed your spending behavior for at least six months before using this option.

I speak from experience here. Several years ago, I obtained a debt consolidation loan for several credit cards and some department store debt. We paid $315.60 a month (I still remember the amount) for FOREVER. Finally the day came when the last payment was made. Guess what? Our credit cards were loaded back up with an amount equal to what we had consolidated in the first place! We had not changed our spending behavior, and it cost us. If we had consolidated the debt AND stopped our financial misbehavior, it would have been a great decision.

I know that Text is Couple #3's Debt Freedom March and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-3/ Couple #3's Debt Freedom March has been significantly improved by obtaining a 401(k) loan. I am NOT a big fan of this type of debt consolidation, but they had explored the "negotiation" and "surfing" options thoroughly and had run out of other options. As a result, they have decided to obtain a 401(k) loan. Guess what? It has lowered their interest SUBSTANTIALLY and if you check on their monthly progress (Text is HERE and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-3/ HERE), you will see that this move has given them the traction they so desperately needed.

In Part Five, I will be sharing a resource available on-line that can be a huge help to those with excellent credit who are looking to lower their interest rates.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 22nd, 2008 at 12:23 am

Welcome to the latest series - Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Part One -

Text is Know What You Are Paying and Link is http://www.josephsangl.com/2008/08/13/series-restructuring-debt-part-one/ Know What You Are Paying

Part Two - Text is Lower The Interest Rates! and Link is http://iwasbroke.savingadvice.com/2008/08/20/series-restructuring-debt-part-two_42370/ Lower The Interest Rates!

Part Three - Lower The Interest Rates! - Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. Today, we will discuss moving the debt.

Surf The Debts To Lower Interest/Zero Interest Offers

If you live in America or any other heavily-leveraged society, then the chances are that you will receive numerous offers of debt every week. Most of these offers have a "trickeration" ploy that generates consumer interest. The trickeration is typically a "Zero-percent for some number of weeks/months/years" ploy. The reason I call it a trickeration ploy is the fact that the majority of these debts are not paid off within the set timeframe and the interest rate is back-dated all the way to the date of purchase - usually at a very high rate.

But the zero-percent surfing game CAN work for you. I have seen MANY people gain substantial traction with their Debt Freedom March through this technique alone.

Here is how the surfing game works. You receive a "zero-percent for twelve months" credit card offer. There is usually a $75 balance transfer fee, but there is no interest for the twelve month period. One simply applies for the 0% card and transfers their high interest debt to the credit card. When that introductory period is drawing to a close, surf the balance to another "zero-percent for twelve months" card. Keep surfing the balance until the debt is paid off to $0.

If you successfully do this, you have actually tricked the trickeration ploy into working for you!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 20th, 2008 at 01:57 pm

Welcome to the latest series -

Text is Restructuring Debt and Link is http://iwasbroke.savingadvice.com/series-restructuring-debt/ Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Text is Part One - Know What You Are Paying and Link is http://iwasbroke.savingadvice.com/2008/08/19/series-restructuring-debt-part-one_42322/ Part One - Know What You Are Paying

Part Two - Lower The Interest Rates!

There are several ways to lower the interest rate that you are paying on your debt. Here are several ways that have been used very successfully.

Call The Debt Owner

This really catches some people off-guard. For some reason, they believe that the interest rate is truly fixed on their debt. Well, just as "fixed rates" on credit cards are not truly fixed and can be (will be) changed at any time, your "fixed rates" are negotiable.

Paying high interest on a debt? Call the customer service line and try some of these lines out (only if they are true, of course!).

* "I am really trying to eliminate my debt, but these high interest rates are really hurting my ability to do that. Can you please lower the interest rate?"

* "Can you please lower the interest rate on this loan? I have been a very loyal customer, and I could really benefit from some help right now."

* "What can you do to help me lower the interest rate on this loan?"

Things NOT to say �

* "You stink. Your company stinks. You are lying, cheating, good-for-nothing scammers. I wish a 1,000 SPAM e-mails per minute upon your life."

* "You're ugly. You're responsible for the recession. I am going to talk about you on my Facebook page."

The first person you talk to will probably not have the authority to change the terms of your loan. Be persistent and ask to speak to their manager. I have had people tell me that it has taken several separate phone calls before they got their interest rates lowered. Many times in spite of a great effort, folks have been unsuccessful and the interest rate was not lowered at all. That brings us to another option. - Move The Debt - and this will be discussed in the next part of the Text is Restructuring Debt Series and Link is http://iwasbroke.savingadvice.com/series-restructuring-debt/ Restructuring Debt Series.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

August 19th, 2008 at 12:53 pm

Welcome to the latest series - Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Part One - Know What You Are Paying

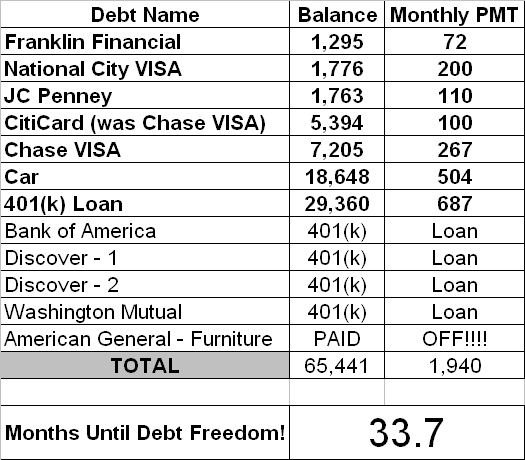

I have said and will continue to say that I believe that the top causes of financial failure are disorganization and the lack of a plan. If you want to gain the maximum traction on your Debt Freedom March, you need to pay the minimum interest possible.

In many of my financial counseling appointments, we add up the amount of interest that is being paid each year, and it SHOCKS the ones who have been paying it! There is something about SEEING IT ON PAPER that really connects us to the fact that paying interest is not a healthy financial plan.

I have developed a tool to help you easily calculate the amount of interest you are paying every month and year. The

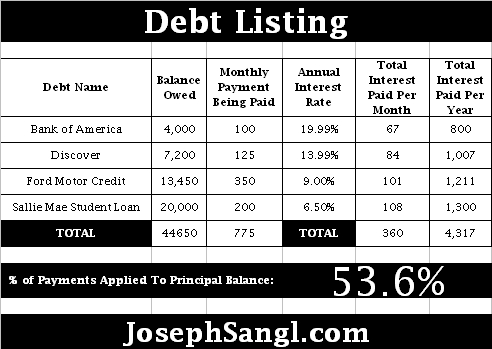

Text is Debt Listing (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=70 Debt Listing (Excel) is an Excel spreadsheet tool that will help you organize your debts and clearly understand the amount of interest that is being paid on the debt.

The form is very user-friendly. All you have to do is enter the debt name, the balanced owed, the monthly payment you are actually paying, and the annual interest rate of the debt. Below is an example.

In this example, you can see that this person has four debts totaling $44,650. The big issue is that $4,317 is being paid in interest every year. In fact, only 53.6% of the monthly payments is being applied to principal reduction.

Now that we are organized it is time to look for ways to reduce/eliminate the interest being paid. That will be covered in Part Two of "Restructuring Debt"!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Restructuring Debt

|

0 Comments »

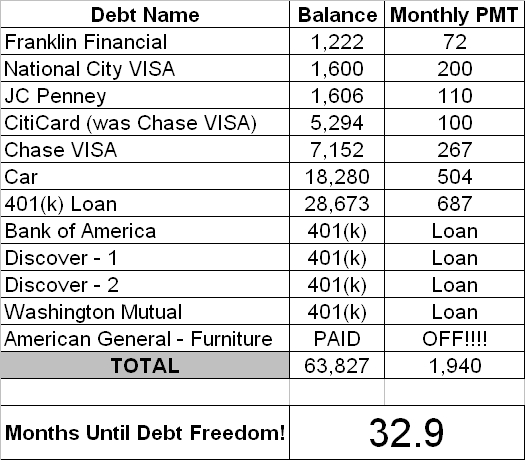

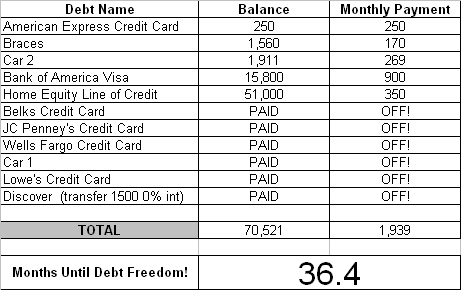

August 18th, 2008 at 01:11 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

This month's update

We have still increased our payment on the National City card and are determined to get it paid off SOON! We absolutely could not do this without the budget/budget form. It is AMAZING how much that tool helps us! (Get your own budget form Text is HERE and Link is http://www.josephsangl.com/tools/ HERE)

Struggles? Hmmm� Nothing specific really.

We have transferred two of the credit cards a couple days ago that will show up on the next month's sheet and that what went well!  More on that one next month!

Updated Debt Freedom Date �

Month By Month Progress �

Month By Month Progress �

Sangl Says �

Sangl Says �

When Couple #3 started out, they had an incredible level of high-interest debt. The high interest was absolutely crushing their efforts to become debt-free. They have taken the first few months of their Debt Freedom March to restructure their debt such that they can make tremendous strides toward their goal of ZERO debt. Nearly all of the debt has been restructured at this point, and you can see that fact very clear through their progress in just one month. They are sending the same amount toward their debt each month, but now it is nearly all going toward the principal balances.

Watch out Franklin Financial, National City, and JC Penney!

Readers

Do you have high interest debt that is crushing your attempts to lower your debt? Restructure it! A series on restructuring debt will be appearing soon on this wildly popular website known as JosephSangl.com!

Help Is Available!

If you have tried to put together a budget that works and it just is not working, I want you to know that help is available. We provide FREE one-on-one financial counseling here at NewSpring Church - both the Anderson and Greenville campuses. There are about fifteen incredible volunteers who are passionate about helping others win with their money. You can request an appointment by clicking Text is HERE and Link is http://www.josephsangl.com/?page_id=2 HERE. We even provide a limited number of on-line appointments too!

You might consider picking up a copy of Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not. In this book, I spend four chapters telling my family's story of walking out of debt and into financial freedom. In the final nine chapters, I teach the practical tools that we used! It is a fast read at 121 pages, and it might just change your life!

Posted in

SERIES: Debt Freedom March - Couple #3

|

0 Comments »

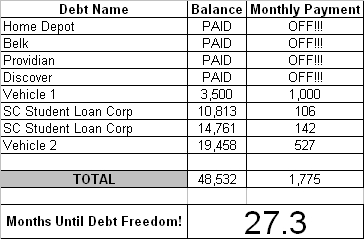

August 13th, 2008 at 02:33 pm

Introduction

This couple is THROUGH with debt! It has now been eight months since they announced that they were breaking up with debt. They have agreed to share their Debt Freedom March with everyone in the hopes to inspire others to do the same!

Here is this month's update.

We are still on the wagon, just very busy. Everything is still going well. We are still using our Text is cash envelopes and Link is http://www.josephsangl.com/2007/01/20/why-i-am-such-a-big-fan-of-cash-envelopes/ cash envelopes �and loving it!! We have really gotten the hang of things and luckily we don't have a whole lot of ups and downs. Everything is running steady and smooth. Our upcoming goal is paying off vehicle #1. It won't be long!!! The most exciting thing for us right now is seeing our balances (debts) get lower and lower. One vehicle balance is less than $4,000 and the other just dropped below the $20,000 mark. Seeing little accomplishments like those keep us going. We are seeing the light at the end of the tunnel, and it is very exciting.

Here is their updated Debt Freedom Date calculation �

Month By Month Progress �

Month By Month Progress �

Sangl Says �

Sangl Says �

Couple #2 is in a time of financial blessing, and they have decided that they are going to manage it to the very best of their ability. In just 10 months, they have reduced their Debt Freedom March by 16.9 months. At this rate, they will be be 100% debt-free in just 16.1 months!

Vehicle #1 will be gone just in time for Christmas! There is nothing like a paid-for car. The $1,000/month payment will then be applied to the SC Student Loan. Too bad for SC Student Loan. They expected that Couple #2 would be paying toward that loan for the next ten years. Instead, it will be gone in the middle of 2009.

Simply awesome.

Readers �

Couple #2 is on a roll. You can do the exact same thing! Pull up the Text is Debt Freedom Date Calculator (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=4 Debt Freedom Date Calculator (Excel) and put together your own Debt Freedom Date!

If not now, when?

Text is Read Previous Updates For Couple #2 and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-2/ Read Previous Updates For Couple #2

You can receive each post via E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE!

Posted in

SERIES: Debt Freedom March - Couple #2

|

0 Comments »

August 12th, 2008 at 01:19 pm

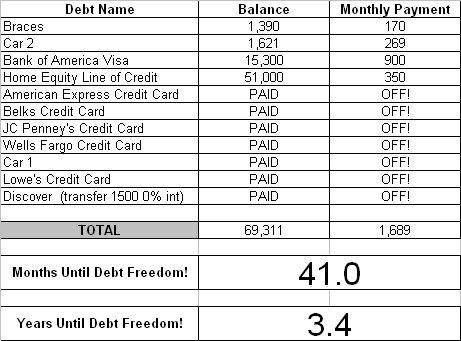

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now ELEVEN months into their Debt Freedom March.

Good/Bad This Month

We are really struggling with the economy right now. We are in sales and am currently way below last year's figures. For the first time in twenty years, we laid off people in our home office. Things are really scary. On the bright side, we are not carrying near as much debt as this time last year so we are not creating new debt which to me is the most important thing. I thank God for all we have and pray for those who are struggling way more than my family. Thanks for all of your help and wisdom.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Another debt has left Couple #1's household! The American Express has been kicked out forever. Nice!

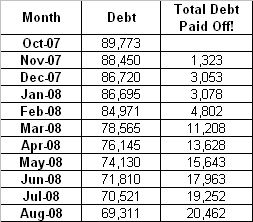

Here is what is so incredible - Couple #1 began attacking their debt just eleven months ago, and they have paid off $20,462! Way to go Couple #1 - I can't wait to see where you guys stand at the end of your first full year of attacking your debt!

Readers �

How is your own Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction Text is HERE and Link is http://josephsangl.com/iwasbroke/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

August 11th, 2008 at 01:17 pm

I had an amazing Monday a week ago.

First, I had an incredible weekend teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience and the Financial Counseling Experience at NewSpring Church.

And then Monday showed up. As I walked out of the door, I saw a FedEx envelope wedged in the door. It said it was from "First National Bank". I was not expecting anything from FedEx, especially from a bank. Then I noticed that it was from First National Bank of Omaha. FNBO. As in FNBO Direct. As in the on-line savings account provider that is currently paying 3.50% interest.

Let me set this up before I tell you what was in the envelope.

A couple of months ago, a reader wrote me saying that I should enter a contest being sponsored by FNBO Direct called "Pay Yourself First". All I had to do was prepare a video that shared a major savings obstacle and why I was focused on paying myself first. I did that and uploaded it to YouTube as instructed. A few weeks later, I was awarded a $10 Amazon.com gift card for being one of the early entrants.

Well, here is where Monday and the FedEx envelope rolls in.

The letter inside stated that I have been selected as one of the twenty semi-finalists and that I have been awarded $500 for reaching the semi-finalist level! FIVE HUNDRED DOLLARS!!! I am BLOWN AWAY!

From the twenty semi-finalists, FNBO Direct will select five finalists who will compete in a six-month savings journey. FNBO Direct will match the savings dollar-for-dollar up to $5,000! FIVE THOUSAND DOLLARS! Are you kidding me?! I am so blessed. SO BLESSED.

You can check out my YouTube entry Text is HERE and Link is http://www.youtube.com/watch?v=m6TJVxmoj3g HERE. In the video, you will see/hear me mention the Sangl Home Pay-Off Spectacular. I am so focused on eliminating our mortgage that I provide monthly updates on our pay-off spectacular.

What a great Monday!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

4 Comments »

August 7th, 2008 at 03:45 pm

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 748 IS 752

Squares Remaining: WAS 1678 IS 1674

% of House Owned By The Sangl's: WAS 30.8% IS 31.0%

% of House Owned By Wells Fargo: WAS 69.2% IS 69.0%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

You can read about how Jenn and I stopped being broke and won with our money in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

Posted in

Uncategorized

|

0 Comments »

August 6th, 2008 at 02:28 pm

After nearly two years of pursuing this crusade to help others accomplish far more than they ever thought possible with their personal finances I still can not believe I get to do this for a living!

In less than two years, this thing has went from a mere passion and a book manuscript to a full-service, full-tilt crusade.

If you are preparing to teach about personal finances at your church or business organization, I would love to be able to partner with you! It is my passion and call to help people win with their money. Why? Because when people are financially free they are much more likely to go do EXACTLY what they have been put on this earth to do!

This stuff FIRES ME UP!

Here are options that are available to help you implement a finance curriculum at your church or business.

* Speaking I love to speak and teach on personal finances. But be ready for a FIRED-UP, high-energy speech as I am more than a little PUMPED to teach people about money management. You can watch me speak Text is HERE and Link is http://www.josephsangl.com/hearsee-joe-speak/ HERE.

* Experiences Some call them classes. Others call them seminars. I call them experiences. Why? Because I teach PRACTICAL tools that can be immediately applied. I do not teach theoretical and hypothetical material. The tools that I teach are what Jenn and I personally did to win with our money. The two-hour experience is the most popular - Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience, but the six-hour Text is Financial Freedom Experience and Link is http://www.josephsangl.com/FFE%20Details.htm Financial Freedom Experience has been very successful too.

* Group Study Course This six session study is based on my book, I Was Broke. Now I'm Not. I have found that my home group is where I am challenged AND held accountable. Accountability is so huge when it comes to making the tough decisions that might be necessary to win with money. Find out more about the Group Study Text is HERE and Link is http://www.josephsangl.com/IWBNINHomeGroupStudy/IWBNINHGS.htm HERE.

* Financial Counseling Training In the Financial Counseling Experience, I train people to use the process that we have used here at NewSpring Church to provide one-on-one financial counseling to over 400 people each year! If you are interested in providing financial counseling, this is a great place to start! Since I am an engineer, you can bet that this training will involve a checklist or two.

* Personal Finance Book In I Was Broke. Now I'm Not., I share my family's story of walking out of financial mismanagement and into financial freedom. THEN I share exactly HOW we did it. I share exactly HOW to use the tools and all of the tools are available FREE through the web site. Find out more about the book Text is HERE and Link is http://www.josephsangl.com/iwasbroke/ HERE.

You can contact me Text is HERE and Link is http://www.josephsangl.com/about/ HERE.

I LOVE THIS STUFF!

Posted in

Uncategorized

|

0 Comments »

August 5th, 2008 at 01:50 pm

John Bartlett had some really kind words about Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

I am so humbled by this type of feedback. I am a teacher through and through and any teacher will tell you that seeing others carry the message on to others is the ultimate compliment.

Thanks, John, for the kind words.

You can read his post Text is HERE and Link is http://barlaybrainstorm.blogspot.com/2008/07/goals.html HERE.

Posted in

Uncategorized

|

1 Comments »

August 3rd, 2008 at 10:17 pm

I had the opportunity to meet with Text is Chris Kakaras and Link is http://www.josephsangl.com/wp-admin/www.chriskakaras.com Chris Kakaras this week. He is a young man who is passionate about helping people manage their money God's way. One of the key groups that he speaks to are college students, and I had the opportunity to review some of his materials when we met.

There was a section of questions in his training that really caught my eye. It was good. Very good.

Here is one of the questions (participants in the class are required to answer these questions).

Did you eat today? YES NO

If YES is the answer, then you are blessed and have enough.

So basic, but SO TRUE!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

July 31st, 2008 at 01:59 pm

I wonder how many people are currently at risk of having an article like Text is THIS ONE and Link is http://www.independentmail.com/news/2008/jul/24/anderson-woman-suffers-22k-loss-when-sock-stolen/ THIS ONE written about them?

This is why I am in favor of "cash envelopes" and not "cash socks".

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

July 29th, 2008 at 01:16 pm

Text is Tony and Link is http://www.tonymorganlive.com Tony has placed a picture of his desktop picture on his website with the question, "Does your desktop picture say anything about you?"

So I am posting my desktop picture to see if it says anything about me.

What do you think? Does my desktop picture say anything about me?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

3 Comments »

July 28th, 2008 at 06:54 pm

I have written before about the fact that I have a thirty-year-old house that has thirty-year-old house problems. One of the problems is that the downstairs AC is the original AC for the house.

Problem 1 - January 2008

It was making a "banging" sound.

Diagnosis: Low on refrigerant - $75.

Problem 2 - May 2008

It was not cooling at all, and it was making a loud electrical "HUMMMMMMMM" sound.

Diagnosis: Condenser unit fan was not operating - $200+

Problem 3 - June 2008

It stopped cooling again. It was a day before vacation so I decided to have it looked at when I got back home two weeks later.

Diagnosis: Electrical wiring insulation had worn through and was shorting out the fan - $105

So we are back to enjoying the nice cool air conditioning in the dead-middle of a South Carolina summer.

I wonder when I will have to replace this unit? Part of me wants to bury my head in the sand and hope that it runs another thirty years. The realistic side of me says I should go ahead and start pricing out units. Initial looks have shown a cost of $5K - $7K. Just what I want to spend my money on � an air conditioner.

Why do I bring all of this up? Because it is so important to look ahead when preparing a financial plan. Jenn and I could pretend that this issue does not exist and then have a financial "emergency" when this AC really does fail permanently. In the past (when we were always broke), we would ignore this issue and then be surprised when it failed. Now, we recognize it as a known, upcoming expense, and we plan for it.

I do hope that it lasts another thirty years, though.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

July 21st, 2008 at 05:11 pm

Last month, I wrote that I ordered more copies of I Was Broke. Now I'm Not.

I have now received that order of books.

I have to say I was stunned. STUNNED.

Why?

Let me go back to January 2006 �

It had been about two years since Jenn and I had become debt-free, and it was becoming very clear that we needed to go teach this personal finance stuff full-time. I really felt compelled to write a book that shared our journey out of debt and into financial freedom.

That last line I just wrote is FUNNY. I mean laugh-out-loud HA-HA FUNNY. I had never written a book. How does one write a book? What about copyrighting? What about barcoding, LCCN, and all of that stuff? What about the editing? Not to mention the formatting, editing, and PUBLISHING! I was totally intimidated.

I remember that Jenn and I made the trip down to

Text is NewSpring and Link is http://www.newspring.cc NewSpring to visit Text is Perry and Link is http://www.perrynoble.com Perry, Text is Ken and Link is http://www.avclub.us Ken, and friends for New Years weekend. Perry and Ken had starting doing this new thing called blogging. I quickly realized that this was a way for me to start getting my thoughts written down on paper. At that time, I did not care if anyone read this blog. It was simply a tool for me to get my thoughts down on paper to possibly use in a book some day.

Fast forward two years later to January 2008. I took a HUGE leap of faith and self-published the book - I Was Broke. Now I'm Not. Let me break down what "self-published book" means. It means that I paid cash to a book printer to print this book. In other words, a publisher did not lay out the cash for me. Jenn and I had to lay out the cash. Lots of it.

We took a chance. We took a step of faith.

Fast forward to today and why I am so STUNNED. This week I received the same amount of books that I ordered in January. When I stacked the new delivery of books next to the first shipment, it DWARFED the first set. Why? BECAUSE SO MANY PEOPLE HAVE BELIEVED IN THIS CRUSADE! I am blown away, humbled, and very honored that so many people have invested in this crusade by purchasing a book. I am blown away and humbled by the kind words that have been shared by people whose lives have been impacted by what they have learned and applied through the book.

For all who have invested in this crusade, thank you. I am overwhelmed that I get to do this stuff for a living.

Posted in

Uncategorized

|

0 Comments »

July 17th, 2008 at 09:14 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

What went well this month?

The 401(k) loan payment won't be taken out of the paycheck until July 1, so we were able to increase our payment to $200 on National City this month! YEAH!! We are hoping once the loan payment comes out we can continue doing this��. It is nice to see some balances coming down�..

What were the challenges/struggles this month?

We are just trying to stay on track and see the big picture at the end�BECOMING DEBT FREE!!! The cost of gas and groceries going up is impacting our budget some�but we are shifting things around so that INCOME - OUTGO = EXACTLY ZERO��we couldn't live without the budget sheet!!! It helps us out TREMENDOUSLY!!!!!

Updated Debt Freedom Date �

Month By Month Progress �

Have you taught any of your friends/family this stuff? If you have, how did it go?

My husband has shared this with several co-workers who were excited about it�.he gave them the website so that they could learn more about it.

Sangl Says �

Couple #3 is in position to make dramatic debt reduction. Will it happen? Let us watch and see!

Readers �

If you have debt, what steps do you need to take to position yourself to make dramatic improvements to your debt situation? What will it take to make you take those steps?

Posted in

SERIES: Debt Freedom March - Couple #3

|

0 Comments »

July 16th, 2008 at 07:44 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now NINE months into their Debt Freedom March.

What went well this month?

Staying on schedule. I am glad we started this months ago. I would hate to be carrying that extra debt through these tough times.

What were the challenges/struggles this month?

Expenses are taking all the disposable income right now. Food and gas are unbelievable. We are determined not to create new debt. We are being very creative about saying no.

Updated Debt Freedom Date

Month By Month Progress

What has helped you stay on this Debt Freedom March?

The day that I can say I owe no money to anyone will be a benchmark in my life!

Sangl Says �

Next month, Couple #1 will clear $20,000 of debt paid off in the first 11 months of their Debt Freedom March! That is AWESOME! Also, it appears that the American Express card will be ditched completely! This stuff works!

Readers �

How is your own Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction Text is HERE and Link is http://www.josephsangl.com/iwasbroke/ HERE.

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

July 8th, 2008 at 07:01 pm

Recently, my family loaded up the car and embarked on the longest vacation we have ever taken - for two weeks.

We journeyed through the following states: South Carolina, North Carolina, Tennessee, Kentucky, Indiana, Illinois, Wisconsin, Minnesota, Iowa, and South Dakota.

The first key stop was a week at a fishing cabin in northern Minnesota. I won all of the big fish contests (pictures below to prove it).

Northern Pike

Walleye (my biggest walleye ever)

Bass

After the week in northern Minnesota, the family traveled to a couple of family reunions in Iowa and then we traveled over to the western edge of South Dakota with the ultimate goal of visiting the Badlands, Custer State Park, and Mount Rushmore. The vacation's top moment was the Independence Day Fireworks at Mount Rushmore. Everyone needs to experience them at least once.

What a great vacation! Lifetime memories were made. Lots of time was spent with family. We all got to rest.

Best of all - it was paid for in cash before we ever left. There is NOTHING like a vacation that does not have debt following it home. You can learn how to save for Known, Upcoming Expenses like vacation and Christmas Text is HERE and Link is http://www.josephsangl.com/?p=425 HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

2 Comments »

|