|

|

|

Viewing the 'Uncategorized' Category

April 28th, 2008 at 06:49 pm

In this series, I will be reviewing 529 college saving plans offered by different states.

It might be helpful to first review what a 529 plan is. A 529 plan is a tax-advantaged college savings plan that is named for the section of tax code that outlines how they may operate - Section 529.

Today's 529 Plan is South Carolina's plan - Text is Future Scholar and Link is http://www.futurescholar.com/UserRelationship/UserRelationshipPage.htm Future Scholar.

The South Carolina Future Scholar 529 College Savings Plan is managed by Columbia Management (a division of Bank of America).

What I Like About The Future Scholar Plan

* Columbia Management. I like some of the funds that are offered by Columbia Management.

* Tax Deduction. Although there are some restrictions, most South Carolina residents can deduct their Future Scholar contributions from their SC state tax return!

* Self-Directed Option. Through the "Direct Program" SC residents can manage their own investments, and if one chooses to do so the "load" (sales charge) is $0! If one chooses to invest in the Future Scholar plan with the help of an advisor, there will be a sales charge of around 5%. The sales charge should not deter someone from investing for college however! If you are really intimidated by investing and mutual funds, it would be worth the sales charge to ensure you are getting good advice!

* Learning Center. The Future Scholar plan offers a great site to help one understand and plan for education costs. It is located Text is HERE and Link is http://www.futurescholar.com/Learning+Center/LearningCenterArticlesSection.htm HERE.

* Investment Options. The Future Scholar plan offers three investment options.

1. Automatic Allocation Choice - This option allows one to "set it and forget it" in regard to adjusting the portfolio. It is really aggressive when the beneficiary is very young and moves steadily to become more stable as the child approaches college time.

2. Asset Allocation Choice - This option allows one to make a more specific decision on how one's investments are allocated. This requires a more hands-on approach if one wants to adjust the portfolio.

3. Single Fund Portfolio - This option allows one to invest in specific mutual funds offered via Columbia Funds.

What I Would Like To See Improved

* Expense Ratios. I would love to see the expense ratio of the funds reduced. The average expense ratio is around 1.40% to 1.50%. This is an every year fee and erodes the growth of the investment.

My daughter's college savings is in the SC 529 Future Scholar plan. The tax benefit was the final straw for me to move the investment from another state's plan to the SC plan.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

April 24th, 2008 at 05:34 pm

Someone sent this picture to me, and I thought it was very appropriate!

I am ready for gas prices to go DOWN for once!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

April 23rd, 2008 at 01:51 pm

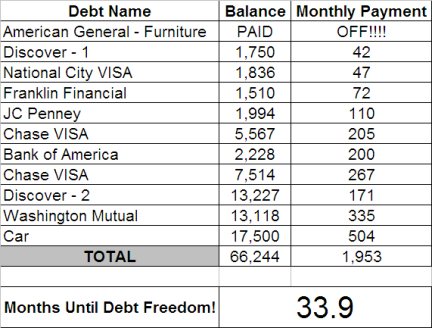

You may have caught in yesterday's post that I absorbed a major expense like the transmission going on my GMC truck. Well, that happened this month.

So here is the story.

I bought this truck from my brother nearly seven years ago. He had purchased it new. Early on, I noticed that the automatic transmission would shift hard whenever I drove the truck over long distances. Once it had cooled, it would go back to shiftly nice and smooth.

So way back in 2002, I took it in to my trusted car repair guy, and he said that I should just drive it until it broke.

So I did. It took nearly seven years for it to fail. I won that gamble!

I took it in to my new trusted car repair guy, and he diagnosed it as "Dead On Arrival". Upon opening the transmission, he could not believe that I was able to even put the car in reverse.

The cost? $1,953.35. That included replacing a broken door handle, an oil change, and some other small stuff.

Man, am I glad I have a savings account for just this sort of stuff! In the old days, I would have been pulling out the credit card.

Maybe I should ask you the question. Do you have money saved up for a car repair?

I am not a prophet, but I can guarantee you that your car WILL break down. It may be today. It may be ten years from now. But something is going to break. When it does, will it crush your finances or will it just be an annoyance that you have saved for?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

My book about how Jenn and I broke free of being broke with $4.13 in the bank was released January 20. It is titled, I Was Broke. Now I'm Not, and it is available via Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM, Text is BORDERS.COM and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go BORDERS.COM, and Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL. You can read the Introduction Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book%20-%20Introduction%20P1.htm HERE.

Posted in

Uncategorized

|

0 Comments »

April 22nd, 2008 at 02:52 pm

There was a day that I was completely broke and had an average bank balance of $4.13. It was awful living with no margin. Anytime an issue cropped up, we had a problem AND a money problem.

One of the best things that Jenn and I did was save money into an emergency fund. What can the money be spent on? I am not sure � I have NEVER spent the money! Seriously, in over five years of having an emergency fund, we have never spent the money.

Did I have an emergency? Well, others might have called them emergencies, but the Sangl household did not. Let me list just a few of the events that have occurred.

* Jenn had major surgery that blew up the $2,300 insurance deductible.

* Ten months later, Jenn had to have the surgery AGAIN. AND it was in another deductible year.

* Power steering went out on the car.

* Transmission went out on the truck.

* The dryer died.

* Huge leaky roof problem.

* I had hernia surgery that blew up the $3,000 insurance deductible.

The Sangl household did not use the emergency fund for ANY of the above expenses. Why? Because they are not really emergencies!!!

Think about it this way.

* Is it a surprise that humans get sick and need surgery? NOPE.

* Is it a surprise that cars break down? NOPE.

* Is it a surprise that an appliance breaks? NOPE.

* Is it a surprise that roofs will leak? NOPE.

When I really think about it, I am not sure we will ever use the emergency fund but it is incredible knowing that it is there!

I wonder if HAVING an emergency fund in place scares off emergencies?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

2 Comments »

April 21st, 2008 at 02:41 pm

Observed today on a sticker - �I know the difference between right and wrong, but I choose to ignore it.�

When it comes to finances, I have learned a lot about what is right and wrong. I hope I do not EVER choose to ignore it!

I have learned that:

* Saving money is right and that spending all of my money is wrong

* Having an emergency fund for emergencies is right and using a credit card for emergencies is wrong

* Giving to worthy causes and individuals is right and not giving at all is dead wrong

* Paying cash for purchases is right and paying on payments is wrong

* Including your spouse in the budgeting process is right and not including them is wrong

* Calling our money �ours� is right and our money �mine� and �yours� is wrong

* Working together as husband and wife toward common financial goals is right and working separately is wrong

* Having medical and life insurance is right and not having this insurance is wrong

* Dealing with one's financial situation is right and just throwing up one's hands and declaring bankruptcy is wrong

* Developing a plan and following it is right and handing one's financial mess over to rip-off credit counseling without changing one's spending behavior is wrong

* Facing one's finances is right and choosing to ignore it is plain wrong

I would love to hear some other truths you have learned as you have dealt with your finances!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

1 Comments »

April 17th, 2008 at 08:16 pm

I had a blast teaching the Financial Learning Experience at Oak Leaf Church last night in Cartersville, GA!

Text is Mike L and Link is http://www.oakleafchurch.com/blog/ Mike L� (You try to spell it!), pastor of Oak Leaf, was there. Lots of people were there.

I went without a microphone which allowed me to completely yell as loud as I wanted to. It was awesome!

I get so FIRED UP about teaching these classes because the stuff I teach is EXACTLY what Jenn and I used to win financially! Every single tool that is available via the "Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" page are tools that we use TO THIS DAY to manage our money. Guess what? It works!!!! And the great thing about teaching it to others is that it is so simple, that ANYONE can do this! If I could figure it out, I KNOW you can do this!

So, Cartersville crew, THANK YOU for attending the FLE last night. I can't wait to hear the stories of saved money, debt freedom, and having a written plan that works. But more than anything, I can't wait to hear your stories of being able to fire yourself from your J.O.B. and being able to go do EXACTLY what you have been put on this earth to do - regardless of the income potential!

If you have any questions, remember you can click on the "Email Joe HERE" link on the sidebar. Thanks!

COMING UP THIS WEEKEND - I will be at Text is Fusion Church and Link is http://www.createfusion.com/ Fusion Church in Suwanee, GA THIS SUNDAY, April 20th, speaking during the morning service and then teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience at 3:00PM. Childcare is provided. I would love to see you there!

PODCAST: Have you checked out the weekly podcast lately? To subscribe to the podcast via iTunes, click Text is HERE and Link is http://phobos.apple.com/WebObjects/MZStore.woa/wa/viewPodcast?id=263126368 HERE. If you do not have iTunes, you can download a mp3 by clicking Text is HERE and Link is http://feeds.feedburner.com/JSFinancialFreedom HERE.

Posted in

Uncategorized

|

0 Comments »

April 15th, 2008 at 01:53 pm

It is so important to continue learning about personal finances. I thought I would share who I am learning about finances from right now.

* Clark Howard - his daily radio show

* Dave Ramsey - his daily radio show (I've read all of his books)

* CNN Money - I love the web site

* Those I counsel - I learn so much from the people I meet with!

* Mary Hunt - Her website (she has good books too!)

* Those who write in questions/comments through the website - I love helping others work through their financial decisions!

That is how I am learning right now.

Who should I be adding to the list?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

April 14th, 2008 at 12:56 pm

Student loans. They are so nice to have around. NOT!

I remember inviting this gal named Sallie Mae over to my house and she did not leave for 8.5 years!

After 8.5 years, I decided that it was time to break up with Sallie Mae. She was not really pleased about it.

Anyway, about four years into the pay-off, I received a letter in the mail that said �

"Congratulations. Because you have made 48 consecutive on-time payments, your interest rate has been reduced by 2%!"

That was awesome!

If you have student loans, did you know that YOU could receive the same interest rate deduction?

In fact, I checked out several of the larger Student Loan companies to find out their current policies. Here is what I found.

* Sallie Mae - If you make your first 33 monthly payments on time, you will receive a check for 3.3% of the amount borrowed! If you opt to have the 3.3% credit applied to your loan amount (I would), it will save about 5.35% of the amount borrowed due to interest savings! Click Text is HERE and Link is http://www.salliemae.com/after_graduation/manage_your_loans/repaying-student-loans/benefits/cash_back.htm HERE for Sallie Mae's Cash Back details.

* SC Student Loan - Through their Quarterback Program, borrowers can automatically receive a 0.25% interest rate reduction for allowing monthly drafts for your payments. Through their Best Interest Program, after making 36 consecutive on time payments, borrowers will receive a 2% interest rate reduction. If you make all of your payments on time, then the last portion of your loan will be forgiven - up to $750! Read all about SC SLC's benefits Text is HERE and Link is http://www.scstudentloan.org/wp270.aspx HERE.

* Wachovia Student Loan - They will provide a 1% rebate when loan repayment begins. Another 1% rebate after 12 months of consecutive on time payments. Another 1.5% rebate after making 24 on time payments! You can read about that Text is HERE and Link is http://www.wachovia.com/personal/page/0,,325_496_8292_8315,00.html HERE.

The common thread through all of this is ON TIME PAYMENTS!!!

Have fun saving money! By the way, I love the automatic draft feature. I use automated drafts for all of my investments. It really helps me stay on the wagon (it is one of my wagon staplers!).

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

April 13th, 2008 at 08:43 pm

At NewSpring Church, we are able to provide FREE one-on-one financial counseling for hundreds of people each year. I have a crew of awesome volunteer financial counselors who help people develop a plan that works! I love it!

One thing we have all seen is the fact that over HALF of the people that we meet with no longer have a home phone. They have dumped the home phone and are using their cell phones instead.

For those who still have a home phone, I am seeing a cost ranging from $35 to $50/month.

Let's think about this in a larger way.

$50/month = $600/year

How much money do you need to earn to bring home $600? Think about it. If you want to bring home $600 extra in your paycheck, you will need to earn something like $900.

So � By getting rid of the home phone, you are giving yourself a $900/year raise!

I LOVE giving myself pay raises!

Have you dumped your home phone? Select your answer in the survey below!

Have you dumped your home phone?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

April 12th, 2008 at 01:49 pm

I was traveling to teach the Financial Freedom Experience this weekend, and I heard a radio commercial about make-up.

The voice-over person said, "Discover how our make-up can change your life."

Really? It can change my life?

Wow. I am going to go order a bucket of it now.

Readers: What other outrageous claims have you heard as part of product/service marketing?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

3 Comments »

April 11th, 2008 at 06:59 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

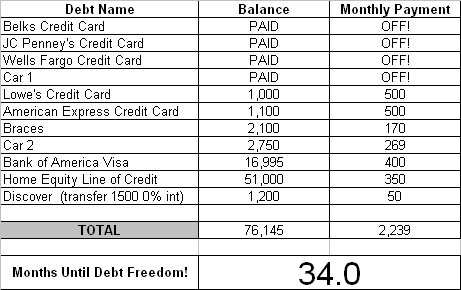

What went well this month �

We transferred part of our Bank of America balance to the "Discover - 2" card at a much lower interest rate. We are trying to eliminate the Bank of America card due to the fact that they are increasing interest rates, even though they have not "attacked" us yet. We also transferred the 29.9% VISA to a 0% Citi Card. We are also able to TITHE (give to the church)! That is so exciting to us!

What were the challenges/struggles this month �

The bonus we were expecting was not nearly what we had hoped for. We decided to plop it in the ING Direct Savings Account and save it for property taxes.

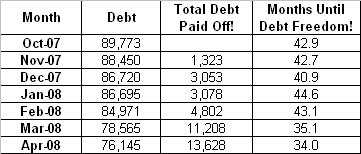

Updated Debt Freedom Date �

Month By Month Progress �

Sangl Says �

Couple #3 transferred a 29.9% balance to a 0% interest card. That is AWESOME! The balance on that card was $5,629. With this one change, they are able to save over $1,600 a year in INTEREST! That means that nearly $140 of the $205 monthly payment was going toward interest. It is now going to principal reduction. WAY TO GO!

Continue working the interest rates to 0% or close to it. It will really speed up your Debt Freedom March!

Couple #3 has been able to start tithing to their home church as well. That is AWESOME! I know that if Jenn and I were not able to give, I would be very unhappy. I love giving! There is something so powerful in being able to support someone or something that you really believe in.

I can not wait to see next month's update!

Readers �

As you can see from Couple #3's Debt Freedom March, it takes work to get some traction. Couple #3 is doing the work necessary to take their finances to the next level. Are you doing the work necessary to manage your money to the ABSOLUTE BEST of your ability?

Posted in

Uncategorized

|

0 Comments »

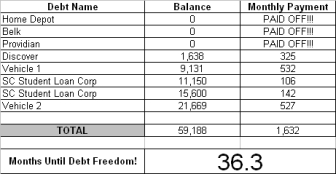

April 10th, 2008 at 07:45 pm

Introduction

This couple is THROUGH with debt! It has now been five months since they announced that they were breaking up with debt.

Here is this month's update!

What went well this month �

This was a good month. We stuck to our cash envelopes and, of course, did not add any new debt. We got money back from our taxes, which we used to PAY OFF OUR LAST CREDIT CARD!!!! Yes, that's right�no more credit card debt!!!!!! As Joe suggested, we saved a little of our tax reFUNd for ourselves, and used the rest to pay toward debt. We had enough money to put an EXTRA $1,000 toward paying off Vehicle #1. It was a great month!!

Challenges and struggles this month �

Some of our cash envelopes ran out quicker than usual this month. We made it a point to pull money from another envelope and not use our debit card. Other than that, we don't have any "real" struggles with the plan. We know what needs to be done and we stick to it.

Here is their updated Debt Freedom Date calculation �

Month By Month Progress �

What has kept you on track for seven months? What motivates you to stick with it?

When we first started this we had meetings with Joe every month or so. The fact that we had someone holding us accountable for our actions made a difference in the beginning. Of course, we wanted to do what he said and be able to show him we were making progress each month. But, as time went by we really got into it. The fact that we could be debt free in 2 or 3 years (other than our home) was really exciting to us. Especially since I thought I was going to pay on my student loan for the next 15 years!! Once we got started there was no turning back. We love paying for things in cash, we love having a plan and we love paying off our debt and not adding to it. It is freeing!! Our focus starting in April is paying off Vehicle #1. I think that is key�taking it one month at a time, having a focus and celebrating each feat, no matter how big or small.

One last thing that has help my husband and I stay focused is we are a team. It takes 100% TEAM WORK!! When one of us is weak, the other is strong. We make decisions together and stick to the plan together!!!!

Sangl says �

It is AWESOME to see what is happening in Couple #2's lives!!! I am BLOWN AWAY every single time I see people "get it" and catch a vision of what life will be like without payments. In just SEVEN months, this couple has paid off $16,339 in debt AND eliminated ALL OF THEIR CREDIT CARDS!!! In just SEVEN MONTHS, Couple #2 has reduced their Debt Freedom Date by TEN MONTHS. They are already THREE MONTHS ahead of plan! This is typical for folks who say "I HAVE HAD ENOUGH!"

I would not be surprised to see Couple #2 achieve Debt Freedom twenty months from now. That would make Christmas 2009 and AWESOME Christmas! Think about it � Imagine saying to each other at Christmas, "Honey, I bought you Debt Freedom for Christmas! We now have over $1,600 a month that we can spend on other cool things like investments, vacations, and giving!"

Posted in

Uncategorized

|

2 Comments »

April 9th, 2008 at 04:56 pm

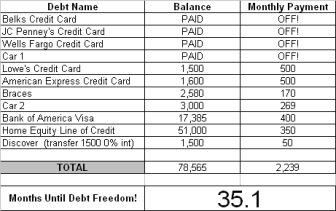

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now SEVEN months into their march. Here is this month's update.

What went well this month �

We are working the plan. I jacked up the emergency fund to $5,000 and payed a little more on some bills.

What were the challenges/struggles this month �[/b[

NONE

[b]What has kept you on the wagon for SEVEN months?

I sleep at night. I owe this to my family. God has blessed us with so much, and I need to take good care of it.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says �

Incredible progress again this month! This is outstanding. By my calculations, this family will be debt-free except for their house (1st Mortgage and Home Equity) in less than TWELVE MONTHS! That will be INCREDIBLE!

Lowes and American Express are going to be leaving within the next few months and then the dentist is going to be VERY CONFUSED when the office receives a snowball payment of $1,170 ($500 Lowes + $500 AMEX + $170 Braces)! It is so fun to watch the debts just leave!

Readers �

THIS is what happens when you experience your IHHE Moment and get intensely focused! This debt does not stand a chance. I love it! This stuff works! I can't wait to receive an invitation to YOUR debt freedom party!

Posted in

Uncategorized

|

0 Comments »

April 8th, 2008 at 04:04 pm

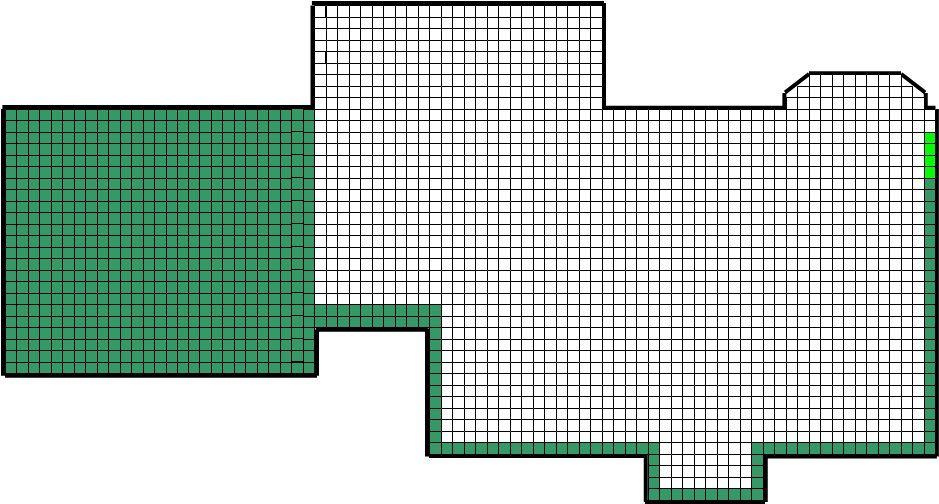

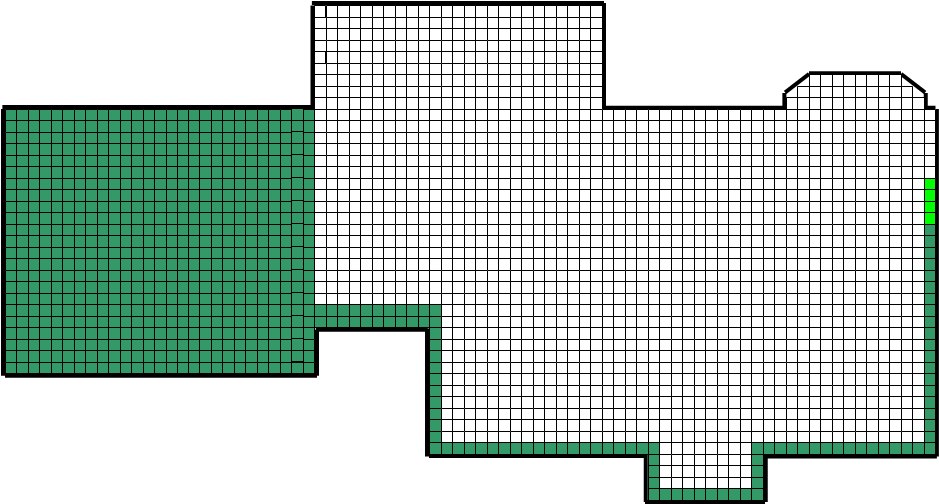

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular! The sixth monthly update is TODAY!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: 735

Squares Remaining: 1691

% of House Owned By The Sangl's: 30.3%

% of House Owned By Wells Fargo: 69.7%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

As stated last month, we remained on the "slow path" for another month to ensure we have adequately prepared for known, upcoming expenses. The worst thing in the world would be for us to be blasting this mortgage and be cash-poor. I can't wait until we attack this mortgage with some huge payments again. A few more months of slowed up payments. ARGH!

Posted in

Uncategorized

|

0 Comments »

April 5th, 2008 at 03:21 am

Welcome to the latest series - "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One What is a mutual fund?

Part Two Establish investment goals

Part Three Types of mutual funds

Part Four Locate mutual funds that meet individual criteria

Part Five Start Now!

What a great series this has been! I love talking about investing because it is what allows us all to achieve dreams! As you might guess, I am FIRED UP!!!

I end the series with Nike's slogan - Just Do It!

I carry this crusade to help others win with their money all over the place, and I still can't believe the number of people that have not begun to invest. People in their 30s! People in their 40s! People in their 50s! People in their 60s!

So no matter where you are, I have to tell you what Charles Schwab once said �

"The best place to start is where you are with what you have."

It is time to get started. At least invest enough to get the company's match. It's FREE money!!!

If you have non-house debt, I recommend that you follow my hero's (Dave Ramsey) 7 Baby Steps. Click Text is HERE and Link is http://www.daveramsey.com/media/pdf/fpu_babysteps.pdf HERE to print your very own copy of his 7 Baby Steps. Invest enough to catch the free company match and then kill your debt. Then get a huge emergency fund of three to six months expenses and invest at least 15% of your gross income into tax-advantaged investments. That is where the real fun begins - when you are able to fund your God-given hopes/plans/dreams!!!

Read the entire "Choosing Mutual Funds" series by clicking Text is HERE and Link is http://iwasbroke.savingadvice.com/series-choosing-mutual-funds/ HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

April 4th, 2008 at 02:26 am

Welcome to the latest series - "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One What is a mutual fund?

Part Two Establish investment goals

Part Three Types of mutual funds

Part Four Locate mutual funds that meet individual criteria

Once I have determined the category of mutual funds that meet my criteria, it is time for me to review actual mutual funds. To find the mutual funds, I use a three-part approach.

1. Mutual Fund Screens - I really like Text is CNN's Mutual Fund Screener and Link is http://money.cnn.com/data/funds/screener/ CNN's Mutual Fund Screener and Text is Morningstar's Mutual Fund Screener and Link is http://screen.morningstar.com/FundSelector.html Morningstar's Mutual Fund Screener. For example, I used the CNN screener to select Small Growth Diversified Funds that have delivered an average of 10% annual return OR LARGER for the past 10 years. It delivered 36 mutual funds that met that criteria! This really helps me narrow down the search!

2. Review Retirement Plan Mutual Funds - If your employer has a retirement plan such as a 401(k), 403(b), Simple IRA, or TSP then be sure to review the options available. My employer has a Simple IRA with American Fund investment options. Usually an employer helps absorb some of the fees or the fees are reduced by the plan administrator. This can really help preserve financial gains!

3. Seek Professional Guidance - I meet with a financial advisor about once a year. This professional advice helps me look at my investments with more clarity.

Once I have found funds to look at, I look at the following characteristics of each fund:

* Age of the Mutual Fund I like mutual funds that are older than me!

* Investment Growth I look at the 1, 5, 10, and Lifetime track records.

* $ Needed To Start This is really important for beginning investors.

* The Fund's Objective This helps me understand the direction of the fund.

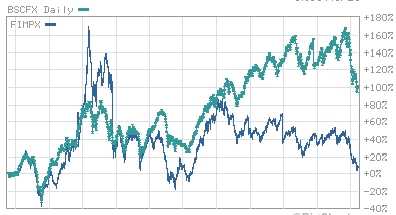

I used the CNN screener in part one above and found two funds to use as an example - First American Small Growth Opportunities Class Y Mutual Fund (Text is FIMPX and Link is http://money.cnn.com/quote/mutualfund/mutualfund.html?sid=861954&symb=FIMPX&time=all&compidx=aaaaa%7E0 FIMPX) and Baron Small Cap Fund (Text is BSCFX and Link is http://money.cnn.com/quote/mutualfund/mutualfund.html?sid=44478&symb=BSCFX&time=all&compidx=aaaaa%7E0 BSCFX).

I use the CNN Money Snapshot feature to analyze funds. Click on the "Stock Ticker" symbols next to each mutual fund above to see the Snapshot for each of the two funds above.

I also like to compare mutual funds to each other using the "Advanced Charts" feature on CNN Money. You can view the actual chart and details on CNN Money by clicking the below chart.

Looking at the two charts over their lifetimes, which would you choose?  Hmmmmmm. One thing I always remember is that history is just that: history. But it is all I have to go on, so that is why I really like mutual funds that have proven track records and have been around longer than I have. These two mutual funds are not even teenagers yet, so the jury is still out for me (Maybe that's why I don't OWN either of these). Hmmmmmm. One thing I always remember is that history is just that: history. But it is all I have to go on, so that is why I really like mutual funds that have proven track records and have been around longer than I have. These two mutual funds are not even teenagers yet, so the jury is still out for me (Maybe that's why I don't OWN either of these).

So that is a glimpse into how Joe chooses mutual funds. Many times it ends up with a dead end, and I go back to the starting point again to get more mutual funds to compare.

Tomorrow, this series includes with the most important part of the entire process!

Read the entire "Choosing Mutual Funds" series by clicking Text is HERE and Link is http://iwasbroke.savingadvice.com/series-choosing-mutual-funds/ HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

Uncategorized

|

2 Comments »

April 3rd, 2008 at 01:27 pm

Welcome to the latest series - "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One What is a mutual fund?

Part Two Establish investment goals

Part Three Types of mutual funds

There are literally THOUSANDS of mutual funds available in the marketplace today. Each mutual fund is usually assigned to a particular family of mutual funds.

Here are some common categories of mutual funds �

* International Stock Fund

* Aggressive Growth Stock Fund

* Growth Stock Fund

* Growth & Income Stock Fund

* Equity-Income Fund

* Balanced Fund

* Bond Fund

* Value Fund

* Industry-Specific Funds (like Healthcare Fund or Pharmaceutical Fund)

* Index Funds (S&P 500, Russell 2000, etc.)

If you purchase ownership in an International Stock Mutual Fund, you can bet that it is primarily investing in international companies. If it is an Aggressive Growth Stock Mutual Fund, you would expect to see the mutual fund purchasing shares of companies that are growing like crazy.

Each family of funds has a general "feel" to it. The International and Aggressive Growth Stock Mutual Funds tend to have wild swings in performance. One year it could grow 40% and the next it could lose 25%. It feels like you are on a great roller coaster ride at Six Flags!

Growth & Income, Equity-Income, and Balanced Funds are more stable and predictable.

Index Funds track specific market indexes like the S&P 500 and the Russell 2000.

In the next post, I will be sharing how to find mutual funds that meet your investment goals.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Posted in

Uncategorized

|

0 Comments »

April 2nd, 2008 at 03:16 pm

Welcome to the latest series - "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

In Part One, I reviewed what a mutual fund is.

Part Two - Establish Investment Goals

My personal investment goals guide my mutual fund choices. First you should know a couple of things about me.

1. I view my investments as money that I will not touch for at least five years.

2. I prefer mutual funds over individual company stocks. I do own one individual company stock, but I will not allow an individual company stock to exceed 10% of my overall portfolio.

My investment goals are GROWTH, GROWTH, and more GROWTH. I do not need my investments to produce income for me as I am in my early 30s. I want my money to GROW. This means that I invest in mutual funds that are purchasing stock of companies that are experiencing major growth (like Google).

Now, if I were retired, I would want my investments to produce income so I would be searching for mutual funds that invest in companies that are paying dividends to its shareholders (like Wal-Mart, Microsoft).

If I were approaching retirement, I would be moving the money that I would need in the next five years to much more stable and secure investments.

In the next part of this series, I will be reviewing the different types of mutual funds. Knowing one's individual investment goals makes the selection of a mutual fund category much easier.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Posted in

Uncategorized

|

0 Comments »

March 24th, 2008 at 12:38 pm

Just found out that my book, I Was Broke. Now I'm Not., is now available at Borders.com!

YAY!

So now, I Was Broke. Now I'm Not., is now available via �

Text is Borders.com and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go Borders.com

Text is Amazon.com and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& Amazon.com

Text is Paypal and Link is http://www.josephsangl.com/IWBNIN%20Book.htm Paypal

Woohoo! By the way, if you want to read the Introduction you can click Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book.htm HERE.

Posted in

Uncategorized

|

1 Comments »

March 23rd, 2008 at 08:22 pm

In Text is THIS POST and Link is http://www.josephsangl.com/?p=384 THIS POST back in August 2007, I shared several of the mutual funds that I own. A quick glance will reveal the name "American Funds" six times in my mutual fund portfolio. Why do I own them? Because they had great track records and lower ongoing management fees than most of their peer mutual funds.

Image borrowed from www.AmericanFunds.com

However, American Funds mutual funds are front-end loaded mutual funds. A load means that there is a sales charge to purchase a share of the mutual fund. If one is just getting started out, there is a 5.25% sales charge. This means that if you have a $100 bill to invest, only $94.75 will make it to the mutual fund. Which is annoying.

BUT, I still invested in American Funds' mutual funds because they simply had great track records.

So, as I was reading CNN's Personal Finance web site, I was very interested to read an article titled "Text is Are American Funds A Good Buy? and Link is http://money.cnn.com/2008/03/18/pf/funds/Ask_the_mole.moneymag/index.htm?postversion=2008031910 Are American Funds A Good Buy?"

Very interesting.

By the way, I don't sell mutual funds or ANY investment product. I DO sell copies of my book, I Was Broke. Now I'm Not. I truly believe that the information in this book will help you take control of your finances and achieve financial freedom. You can purchase a copy via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL or Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

Uncategorized

|

0 Comments »

March 22nd, 2008 at 02:52 am

CNN posted Text is THIS ARTICLE and Link is http://money.cnn.com/2008/03/17/pf/taxes/rebates_payment_schedule/index.htm?postversion=2008031713 THIS ARTICLE that shows the dates that the IRS will be shipping out the Economic Stimulus Payments.

Not sure what to do with your rebate check? Consider reading the "Text is Best Utilize Your Tax Refund and Link is http://www.josephsangl.com/?cat=26 Best Utilize Your Tax Refund" series at www.JosephSangl.com.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

Uncategorized

|

0 Comments »

March 17th, 2008 at 01:50 pm

I love hearing the success stories of those who have had their Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment and began the journey to debt freedom!

Would you take the time to inspire others with your success story? Click the blue "Success Stories" box on the sidebar and share your story. While you are there, check out some of the other stories that have been shared!

I (and the readers) want to hear YOUR success story and celebrate with you - no matter how large or small!

Best story shared by Wednesday receives a FREE copy of "I Was Broke. Now I'm Not." (available via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL or Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON)!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 14th, 2008 at 01:15 pm

I will be saving a ton of money by following the advice of the Text is Coupon Mom and Link is http://www.couponmom.com Coupon Mom!

I recommend you click on the YouTube link on the first page of Coupon Mom's web site to see how it works.

Genius!

Posted in

Uncategorized

|

0 Comments »

March 12th, 2008 at 12:39 pm

I had a BLAST sharing my story at the three Sunday morning services at Text is Hyde Park Baptist Church and Link is http://www.lovinglumberton.com/templates/cushydepark/default.asp?id=21533 Hyde Park Baptist Church in Lumberton, NC this past weekend! After speaking on Sunday morning, Pastors Dennis Harrell and Text is Mike Pittman and Link is http://wholeheartedlife.typepad.com/ Mike Pittman had everything ready to roll for the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience to launch on Sunday afternoon.

We had a fantastic turnout and the audience was ENTHUSIASTIC (to say the least!) about putting together a plan that enables them to go do EXACTLY what they have been put on this earth to do! That FIRES ME UP!

Thanks Hyde Park! You can read what Mike had to say about the weekend Text is HERE and Link is http://wholeheartedlife.typepad.com/wholeheartedlife_dot_com/2008/03/sunday-nite.html HERE and Text is HERE and Link is http://wholeheartedlife.typepad.com/wholeheartedlife_dot_com/2008/03/really-proud-of.html HERE.

With that, I am PUMPED to announce the next two month's upcoming events!

Text is FLE and Link is http://www.josephsangl.com/FLE%20Details.htm FLE (2 hour class) & Text is FFE and Link is http://www.josephsangl.com/FFE%20Details.htm FFE (6 hour weekend conference OR 5 week class)

March 13, 2008 Text is NewSpring Church UNLEASH CONFERENCE and Link is http://www.newspringonline.com/245602.ihtml NewSpring Church UNLEASH CONFERENCE Anderson, SC

March 14 & 15, 2008 FFE Text is 5 Point Fellowship and Link is http://www.5pointfellowship.org/ 5 Point Fellowship Easley, SC

All Tuesdays in April FFE Text is NewSpring Church and Link is http://www.newspring.cc NewSpring Church Anderson, SC

April 4 & 5, 2008 FFE Text is Cornerstone Community Church and Link is http://www.mycornerstone.org/index.php?pr=Home Cornerstone Community Church Galax, VA

April 16, 2008 FLE Text is Oak Leaf Church and Link is http://www.oakleafchurch.com/ Oak Leaf Church Cartersville, GA

April 20, 2008 FLE Text is Fusion Church and Link is http://www.createfusion.com/ Fusion Church Suwanee, GA

May 4, 2008 FLE Text is Avalon Church and Link is http://www.avalonchurch.net/ Avalon Church McDonough, GA

I am FIRED UP! Lives are being changed, and I get to be a part of it! Can I just say (again) that I am so glad I was able to fire myself from Corporate America and go do this?

I would love to take the crusade to California, Texas, New York, and Wyoming. If you are interested in having me speak, contact me by clicking Text is HERE and Link is http://www.josephsangl.com/?page_id=2 HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 11th, 2008 at 01:53 pm

There was a time when I was not passionate about my job. There used to be a time where I went to work at a J.O.B every day and wondered what I was put on earth to do.

Ever been there? It is not fun to go through such times, but I have found that it was absolutely necessary for me to go through that time to be adequately prepared for "what was next".

When you have been through the passionless, listless, awful, and confusing times, you can truly understand how awesome it is to a have a clear, unmistakable, resounding call on your life.

My calling became immensely clear as I began to take real action to improve my financial condition. As Jenn and I broke free financially, it was as if cataracts fell off of my eyes. I saw how huge and real the financial burden was for the majority of my neighbors, co-workers, friends, and family. I saw how huge the problem was for all of America! I simply couldn't take it anymore. I HAD to do something. In fact, the day that I announced that I had fired myself from Corporate America I wrote Text is THIS POST and Link is http://www.josephsangl.com/?p=116 THIS POST which really captured what I was feeling at that decisive moment.

Reading that post from eighteen months ago really brings the emotion of the moment back to me.

Here is why I do what I do �

* Person 1 - Put together a written plan, became debt-free, and is going on a cash paid-for-in-advance vacation to Europe this summer!

* Couple 2 - Put together a written plan, sold the fine luxury car, and will be debt-free before the end of the year. Yes, he cried when the Jaguar left (I would too!), but it is just a car.

* Person 3 - Put together a written plan and will become debt-free in less than HALF the time calculated using the Debt Freedom Date Calculator!

* Couple 4 - Put together a written plan, and are now able to give faithfully to their local church for the first time in their lives!

* Couple 5 - Put together a written plan, built an emergency buffer fund, and are now experiencing a job lay-off - BUT they have savings to help them weather the storm! They have PEACE even in the midst of this issue.

* Person 6 - Put together a written plan because his gift to his bride on their wedding day is for BOTH of them to be 100% debt-free. On the day they are married!

* Couple 7 - Put together a written plan, they will become debt-free before their children start college AND be able to pay for their children's college - something they did not even think was possible! But it was - and is!

* Couple 8 - Did not do so well with money management the first thirty years of marriage, but now have a written plan that will allow them to retire with ZERO debt and with SOME retirement savings - way ahead of what they thought was possible.

* Person 9 - Has always had a written plan, and is flat killing it - but he is buying tons of copies of I Was Broke. Now I'm Not. for his friends and family to ensure they also learn how to win!

* Couple 10 - Put together a written plan, and it has ROCKED their marriage (in a great way!) - it is the first time they have ever talked about money - let alone have a plan they both agree on! (Why do I hear Barry White singing?)

Those are just some of the HUNDREDS of stories of life change that FIRE ME UP! They are THE REASON I do what I do.

I can't believe I get to do this for a living! I am truly living a dream!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

March 11th, 2008 at 12:05 am

I have the great opportunity to help hundreds of people put together a great financial plan.

Something that has been rocking my world lately is the frequency that I hear the following statement during my meetings �

"My parents - UGH! They are terrible with their money."

Is that your story?

One thing that I have learned from my hero, Text is Dave Ramsey and Link is http://www.josephsangl.com/?p=389 Dave Ramsey, is to listen to HOW people say things. To hear the tone in which it is said. To listen to what is being left unsaid.

What do I hear? Regret. Disappointment. Sadness. Shame. Discouragement. Frustration. Anger.

Here is what I can say for certain. HOW you manage your money WILL impact your children!

Proverbs 22:6 comes to mind - "train a child in the way he should go �"

So does Proverbs 13:22 - "A good man leaves an inheritance for his children's children �"

Are you ashamed of your parent's financial management? Resolve to break the cycle with your family.

Are you ashamed of your own financial management? It's time to have your IHHE Moment and change the story!

You CAN do this! I believe in you.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

March 7th, 2008 at 01:27 pm

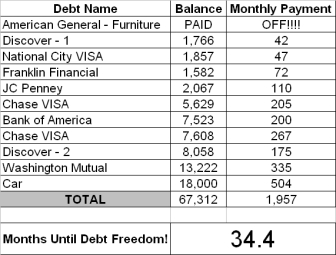

I am excited to introduce Couple #3 - the newest members of the "Marching To Debt Freedom" crusade.

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

What went well this month �

We transferred our Bank of America card balance to another card at a much lower interest rate. We also got the interest rate reduced on one of the Discover cards. We "spent" our tax refund before we actually received it, and it went much further! Half of it funded our emergency fund which is now over $2,900!

What were the challenges/struggles this month �

Not really any this month � except we want it all paid off!

Updated Debt Freedom Date �

Sangl Says �

I am excited about the progress of Couple #3! One debt is already paid off, and more are getting ready to fall! It is AMAZING how fast debt can leave when you have your IHHE Moment!

I challenge everyone to seek lower interest rates on any debt you are carrying. Many times you can obtain a lower interest rate just by calling your credit card. Or you can avoid the conflict altogether by rolling the balance over to a "0% for 12 months" card.

Readers �

Will you take a moment to leave a comment for Couple #3 and thank them for sharing their personal financial information with everyone? It takes a lot of courage to do this, and I am PUMPED to watch this debt fly away!

Read the Debt Freedom March updates for Text is Couple #1 and Link is http://www.josephsangl.com/?cat=19 Couple #1 and Text is Couple #2 and Link is http://www.josephsangl.com/?cat=20 Couple #2

Want to start your own Debt Freedom March? Check out the free tools Text is HERE and Link is http://www.josephsangl.com/?page_id=151 HERE. My book also teaches you how to use all of the free tools. You can purchase your copy at Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM or via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL!

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

1 Comments »

March 6th, 2008 at 06:22 pm

Introduction

This couple is THROUGH with debt! It has now been five months since they announced that they were breaking up with debt.

Here is this month's update!

What went well this month �

Things are going great, and we are sticking to the plan.

Challenges and struggles this month �

I really don't have anything different to say as far as the challenges and struggles for this month.

Here is their updated Text is Debt Freedom Date calculation and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation �

Month By Month Progress �

What are the biggest changes you have seen as a result of the first six months of this march �

The biggest changes we have seen as a result of the first six months of this debt freedom march is that we don't take our money for granted anymore. Before we met Joe we spent our money very foolishly and unconsciously. As a result, we are still paying for our past purchases today (aka: DEBT!). We appreciate our money now and make it a point to think about each purchase we make. I have to say, the march to debt freedom is one of the best things we have ever done. We have not accumulated any new debt and we are well on our way to paying off what we owe.

I am very proud of my husband and myself and extremely thankful for Joe and his brilliant plan. We really started this year off right. As of right now we have a plan for just about everything; Christmas, vacation, vehicle maintenance, taking care of the yard for Spring & Summer, car insurance, car taxes, pet care, birthdays, holidays, etc. Knowing we have the money set aside to take care of the "known upcoming expenses" takes a lot of stress off of us each month. There are no surprises!!

Overall, it feels great knowing we have a plan. This makes us feel in control of our money and our future. If there is anyone questioning whether or not to give Joe a call, please do not hesitate. If I had one regret it would be that we did not meet with Joe and start our journey to debt freedom sooner!!!!!

My husband and I want to say Thank You to Joe for all of his encouragement and support. He has been a wonderful blessing to us and our future. God Bless You, Joe!!

Sangl says �

[BLUSH] I am humbled by the kind words that Couple #2 has shared. All I did was show Couple #2 the tools that I used to become financially free. They have taken it to heart, and I can not wait until I receive an invitation to their debt freedom party. My prediction is that this couple will be debt-free (except for the house) in 24 months or less. I know. I know. The Debt Freedom Date Calculation says 36.3 months, but I have seen way to many people who have had their IHHE Moment. They become debt-free way sooner than the calculation.

Way to go Couple #2!

Readers �

Everything I taught Couple #1 and Couple #2 and thousands of others is in my newly released book, I Was Broke. Now I'm Not. It can be purchased via Text is PayPal and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PayPal or Text is Amazon. and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& Amazon. It is NOT rocket science. I wrote this book in such a way that it can be read in less than 1.5 hours and can be immediately applied to your financial situation.

Would you share with Couple #2 how their sharing of their personal financial situation is inspiring you?

Text is Read Previous Updates For Couple #2 and Link is http://www.josephsangl.com//?cat=20 Read Previous Updates For Couple #2

You can receive each post via E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE!

Posted in

Uncategorized

|

0 Comments »

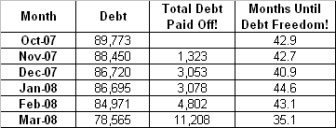

March 5th, 2008 at 01:29 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now SIX months into their march. Here is this month's update.

What went well this month �

WOW! This is like when you can fit into your skinny jeans again. God blessed us and sent us a bonus check and instead of blowing it, I put it to good use. I paid off my car, and paid $3,000.00 on the other car. I am stoked! In about three months, I will be shed of all debt except the big stuff. We are also getting a tax refund, and I am hurling that at debt too. I feel like David reaching for the stones, baby!

What were the challenges/struggles this month �

The only struggle is feeling guilty because we did not do this early on. I would be a freaking gazillionare by now. God rocks. Joe rocks. Not being broke rocks. Yee Ha!

What are the biggest changes you have seen as a result of the first six months of this march �

This has made us focus like a laser beam on our finances - both good and bad. It has let us have a glimpse of what life will be like with no debt, and I like it. I can only wish that anyone who reads this takes it to heart. Don't let credit cards ruin your happiness. I will always remember my Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment!

Updated Debt Freedom Date �

Month By Month Progress �

Sangl Says �

ANOTHER DEBT IS GONE! Couple #1 has definitely had enough. Look at the progress they have made in just six months! Their initial Debt Freedom Date calculation was 42.9 months. They are now down to 35.1 months AND they have avoided all new debt. They had to slow down during Christmas so that they could avoid debt that month, but it allowed them to stay on the path toward financial freedom. In just six months, Couple #1 has made FOUR different debts leave their life!

Way to go, Couple #1! I am FIRED UP by the progress you guys are making!

Readers �

How are you doing on YOUR debt freedom march? You can do this!

Read Previous Monthly Updates For Couple #1 Text is HERE and Link is http://www.josephsangl.com//?cat=19 HERE

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 4th, 2008 at 02:52 pm

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular! The fifth monthly update is TODAY!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 727 IS 731

Squares Remaining: WAS 1699 IS 1695

% of House Owned By The Sangl's: WAS 30.0% IS 30.1%

% of House Owned By Wells Fargo: WAS 70.0% IS 69.9%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

Yes. We slowed down this month. We have some known, upcoming expenses approaching, and we are slowing down for a short period of time. One of the most essential things that I have learned about money is that there WILL be known, upcoming expenses and they WILL come due. Jenn and I are ensuring that we are more than prepared for these expenses.

By the way, we are STILL committed to paying the mortgage off by October 2011 with the same stretch goal of October 2010!

Read previous Sangl Home Pay-Off Spectacular Updates Text is HERE and Link is http://www.josephsangl.com//?cat=16 HERE

Get your own Debt Pay-Off Spectacular Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE and join the FUN!

Already debt-free? Get your own SAVINGS Spectaculars Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

|