|

|

|

Archive for May, 2008

May 29th, 2008 at 12:50 pm

I was teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience here at Text is NewSpring Church and Link is http://www.newspring.cc NewSpring Church on Tuesday evening this week, and I had a gentleman raise his hand and ask this question.

"How Do I Stop Being Impulsive?"

My answer? I don't know to stop the impulsive nature, but I DO know how to control my impulse to spend recklessly.

I am a SPENDER. I am the type of person who would go out and accidentally buy a truck. I am a spender to my very core. I like buying things.

Here are some steps I have taken that helped me reign in my impulsive spending nature, and it has allowed us to win financially!

* Written Spending Plan Putting together a written spending plan EVERY month before the month begins using the budget forms that are available on the TOOLS page. Jenn and I do this EVERY month before the month begins. Did you catch that? EVERY month. It reinforces the fact that we cannot flippantly spend our money and expect to succeed.

* Cash Envelopes I am an impulsive spender, but even I will not impulsively spend money on the electric bill. I won't impulsively purchase gasoline. I don't impulsively send extra money to the cable company. There are some things that I am not going to impulsively spend money on. However, there are some things that I am VERY impulsive about. Items like groceries, dining out, clothes, spending money, and entertainment. I can go through some money really fast with these items! Since I KNOW that I am impulsive for these spending categories, I use cash envelopes. At the start of the month we add up the amount we have put in the budget for these categories. We then pull that amount out in CASH. The rule is that we can not pull more money out from the bank AND we can not use the ATM or debit card. I can not overspend cash.

* Chopped Up Credit Cards You may pay yours off every month, but the vast majority of Americans do not. I was part of the vast majority, and I had to admit that I was a completely LOSER with credit cards. I ran those stupid things up three different times. STUPID with them. They really catered to my impulsive nature. So I did what had to be done and applied the scissor blades to them and shut the accounts down.

If you are a fellow spender, what have you done to control your impulsive spending habits?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

You can read about how Jenn and I stopped being broke, and won with our money in my new book, I Was Broke. Now I'm Not. It is available via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL, Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM, or Text is BORDERS.COM and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go BORDERS.COM.

Posted in

Uncategorized

|

1 Comments »

May 28th, 2008 at 01:30 pm

Have you ever started something new that you really wanted to stay committed to?

Diets, budgets, exercise, prayer, earlier bedtime, more time with spouse/children.

We start off so great. We can't be stopped. In the gym by 5AM. No chocolate for a month. Asleep at 10PM. Prayed every day for a week.

THEN life happens. Our favorite show is on with a one-hour special. The ice cream truck came by. The snooze button was found. We get busy, life happens, and we fall off of the wagon.

I regularly counsel folks who have fallen off of the wagon with their finances. They are so crestfallen. So sorrowful. So frustrated. Maybe even depressed.

"What should we do?" they ask.

Get back on the wagon!

Put together a new spending plan. Recalculate the debt freedom date. Figure out what caused you to fall off of the wagon in the first place and seek ways to prevent it from happening again.

I know that YOU CAN DO THIS! I was able to do it. You can too! Anyone who has read Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/IWBNIN%20Book.htm I Was Broke. Now I'm Not. knows that I include a line at the end of each chapter that says "I believe in you!" You CAN do this.

Here are some common reasons for wagon bruises (develop when one falls off of the wagon).

* No emergency fund. This is the number one cause of wagon bruises. If there is no protection from "life happens" events, one will be highly susceptible to wagon bruising.

* Not saving for KNOWN, upcoming expenses. We know that Christmas is coming. That property taxes will come due. We know that the car WILL break down and that the tires will need replaced. Whether one saves for these expenses or not, the KNOWN, upcoming expense will still occur.

* Spouses not on the same page. If both spouses are not on the same page financially, it can really lead to some severe wagon bruising.

* Bad case of "I-Want-This-Now-Itis". If one can not say "NO!" when tempted to blow the spending plan, it will cause a financial mess.

* Lack of accountability. This really affects single folks a lot. There is no one to say, "Maybe you should reconsider that decision." It is really easy to overspend when there is no accountability.

Have you ever fell off of the wagon? Share how bad the wagon bruises were and what you did to get back on the wagon.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

May 27th, 2008 at 02:01 pm

Jenn and I were coming back from teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience recently, and I looked in the back seat and saw this.

Yes. That is my daughter reading a copy of my book. Very humbling.

Flash forward a few nights. I go upstairs and see my daughter lying in bed reading the book some more. Here is the conversation.

Me You reading the book again?

Her Yeah. I think it is so funny how you had so much debt and Mom did not.

Me You think that is funny?

Her Yes! You caused all of the debt problems.

Me Yes I did. But I stopped spending money, and we became debt-free.

Her Yeah, but you still caused all of the debt problems. That's funny!

It was so humbling, but I am so FIRED UP that I was able to say the "we became debt-free" part!

Yes, honey, Dad messed up with money, but I woke up one day, shouted " I HAVE HAD ENOUGH!", and we marched out of debt and into financial freedom.

Melea, that is why Dad is on a crusade. I am on a crusade to help as many people as I can get out of their financial mess and achieve financial freedom.

Posted in

Uncategorized

|

2 Comments »

May 22nd, 2008 at 06:20 pm

I know that many times, we feel like we need to wear the mask. The one that says everything is perfect, nothing ever goes wrong, and I have never struggled with anything.

It seems that when it comes to finances, most of us want to wear a mask. The mask that says "We are doing fine." One that says, "I am doing better than you are." Maybe one that says, "I have a lot of money. More than you. No, WAY more than you."

The mask that says, "I am doing well financially." even though one is financed up to their eyeballs.

Ultimately there is the truth. The truth is that over 70% of Americans are living paycheck-to-paycheck. If they miss ONE paycheck, they will fall behind on one or more bills. The truth is that somewhere around 20% of Americans are not only living paycheck-to-paycheck, but they are already behind on one or more bills.

The truth trumps the mask every single time, and I love it when people get real.

When they say, "I HAVE HAD ENOUGH!", and embark on the quest to take control of their finances. When they realize that they CAN win with their money, and they seek knowledge on how to do so. I love it when they get so real that they invite their friends, family, co-workers, and neighbors over to the house for dinner and then show them how to put together a budget that works.

I LOVE IT when that happens!

There was a day that I felt like I needed to show everyone that I was doing really well financially, but the reality was that I had an average bank balance of $4.13. I dropped the pose (PRIDE), said "I STINK at this!", and I went and got help.

Dave Ramsey absolutely rocked my world with his 7 Baby Steps. You can click Text is HERE and Link is http://www.daveramsey.com/media/pdf/fpu_babysteps.pdf HERE to print your own copy!

Are you being real about your financial situation?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

3 Comments »

May 21st, 2008 at 02:17 pm

Funny, but not funny cartoon from CartoonStock.com - Text is The TRUTH about pay raises at many corporations and Link is http://www.cartoonstock.com/newscartoons/cartoonists/mba/lowres/mban1971l.jpg The TRUTH about pay raises at many corporations.

"That $20 paycheck deduction is for new benefits - like the $10 raise you just got."

ARGH. You can't put enough spin on that statement to make it look pretty!

Has anyone experienced a similar situation where you received a "raise" and then an increase in benefit costs that completely vaporized the raise and then some?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

8 Comments »

May 20th, 2008 at 01:20 pm

I had a blast teaching the

Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience in Orlando, Florida at Text is C3 Church and Link is http://www.c3orlando.com/templates/cusc3orlando/default.asp?id=34510 C3 Church! I was blown away by the hospitality shown to me by their pastor Byron Bledsoe and executive pastor Barry Leathers. Totally blown away.

They were completely prepared for the FLE, and the crowd showed up ready to learn. It was awesome!

C3 Church - you guys rocked! I can't wait to hear the stories of debt freedom and dreams that are achieved all because you guys put together a plan to accomplish EXACTLY what you have been put on this earth to do.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

May 19th, 2008 at 07:13 pm

I went to my daughter's school to eat lunch with her on Wednesday. I was hoping for pizza, but instead it was chicken strips. I thought the chicken strips were good - especially when coated with honey mustard sauce. I was VERY disappointed when I saw that the side item was canned peas. Most people had received lima beans (which I am able to stomach - a little), but the kitchen ran out of lima beans. They ended up serving the rest of us the canned peas.

Of the twenty or so kids at my daughter's cafeteria table, only one ate their peas. I managed to eat one bite. It was AWFUL!

Many people believe that preparing a budget and living by it is the equivalent of eating canned peas. They might even try it a little bit, but they will hold their nose while doing so.

Budgeting does not have to be that way. It is nothing more than telling your money what to do BEFORE the money ever shows up! When you have a written plan for your money, it has a much better chance of going exactly where you wanted it to go.

Think of it this way. Would you hold a birthday party for your child without ensuring there was enough cake for each of their friends? No way! Would you invite guests over for dinner and wait until they were there to think about what you should prepare for them? Never!

So why would one wait until all of the bills show up before even thinking about how the money should be spent?

You can get started with your own budget TODAY by visiting the TOOLS page. They are FREE! You can prepare a weekly/bi-weekly/bi-monthly budget with the

Text is Weekly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=2 Weekly Budget Form (Excel). If you have enough saved up in the bank to pay all of your bills once a month or you are paid once each month, you can use the Text is Monthly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=1 Monthly Budget Form (Excel) budget.

Have a blast as you make your money behave! Take it from a huge reformed spendaholic, a budget is THE WAY that Jenn and I won with our money. It is not the equivalent of canned peas.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

May 18th, 2008 at 08:38 pm

I am BLOWN AWAY at the fact that as of May 4, 2008, I Was Broke. Now I'm Not. cleared 1,000 books sold.

I am stunned, humbled, and honored. One of my life goals was to write a book and sell at least one copy. I thought that maybe I could talk my mom into buying a copy if that was what it took to sell one. Moms always want to see their kid's achieve their dreams.

But for some reason people have bought the book.

Here are some of the reviews written by some different folks who bought the book:

* Kem Meyer wrote a review Text is HERE and Link is http://kemmeyer.typepad.com/less_clutter_noise/2008/04/i-was-broke-but.html HERE.

* Rob Singleton gave a copy away Text is HERE and Link is http://www.robsingleton.net/2008/01/27/dont-say-i-never-give-you-anything/ HERE to the person who shared the funniest/dumbest financial decision they ever made. Be sure to read all of the comments below that post. It was incredible!

* Lori Capace shared her thoughts Text is HERE and Link is http://loricapace.wordpress.com/2008/03/18/getting-out-of-debt/ HERE.

* Paul Neel wrote a post Text is HERE and Link is http://paulneel.blogspot.com/2008/02/book-4-i-was-broke-now-im-not-by-joseph.html HERE.

To everyone who has purchased a book - THANK YOU! Thank you for investing in this crusade to see people accomplish far more than they ever thought possible with their personal finances.

Why am I so passionate about this? Because when people are financially free, they are much more likely to do EXACTLY what they have been put on this earth to do - regardless of the income potential!

I am honored, and I am more FIRED UP than I have ever been!

Thank you.

Joe

Posted in

Uncategorized

|

1 Comments »

May 17th, 2008 at 01:20 am

Let me introduce you to the Virginia College Savings Plan.

This 529 plan is managed by one of my favorite mutual fund companies - Text is American Funds and Link is http://iwasbroke.savingadvice.com/2008/04/27/the-mutual-fund-series-american-funds_38314/ American Funds.

What I Like About The Virginia College Savings Plan

* CollegeAmerica. This is the partnership between the Virginia College Savings Plan and American Funds. You can read about it in detail Text is HERE and Link is http://www.americanfunds.com/college/college-america/index.htm HERE. I really like American Funds' mutual fund offerings.

* Choices. American Funds offers 22 different mutual funds as part of the CollegeAmerica plan. You can also choose to put together a selection of the Text is 22 different mutual funds and Link is http://www.americanfunds.com/college/college-america/investment-options.htm#all 22 different mutual funds and take an age-based approach toward your investment.

* Low Initial Investment Requirement. You only need $250 to get started with the CollegeAmerica plan. That makes this available to everyone!

* State Tax Deduction for Virginia Taxpayers. If you are a Virginia resident and contribute to this fund, you are most likely eligible to deduct those contributions from your state taxes! Virginia residents are allowed to deduct up to $2,000 PER ACCOUNT per year with unlimited carryforwards. NICE!

What I Would Like To See Improved

* This is a general improvement that I would like to see with all 529 plans, not just the Virginia College Savings Plan. I would really like to see contributions to ANY state's plan be DEDUCTIBLE from one's own state taxes. I know. I know. I am dreaming again, BUT it would really provide a huge incentive for states to have a great and competitive 529 plan.

Read reviews of other state 529 college savings plans Text is HERE and Link is http://iwasbroke.savingadvice.com/series-529-plans/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: 529 Plans

|

0 Comments »

May 15th, 2008 at 07:51 pm

During each part of this weekly series, I will be looking at a specific mutual fund company.

Today's company is Fidelity Investments.

Fidelity Investments is a very large full-service investment company. They manage over three hundred mutual funds and offer a variety of services. Some of the services they provide include retirement plan management and discount brokerage services.

What I Like About Fidelity Investments

* Options. Lots of them. With over three hundred mutual fund options, I can be certain that I can always find a fund that suits my investment goals.

* Target Retirement Funds. Along with Text is Vanguard and Link is http://iwasbroke.savingadvice.com/2008/04/16/the-mutual-fund-series-vanguard_37908/ Vanguard, Fidelity is a leading provider of target retirement funds. They call their target retirement funds " Text is Freedom Funds and Link is http://personal.fidelity.com/products/funds/content/DesignYourPortfolio/freedomfunds.shtml.cvsr?refpr=zdypff004 Freedom Funds". Target retirement funds are mutual funds that have a set retirement year attached to them. As the targeted retirement year approaches, the fund portfolio will be automatically shifted toward a more conservative mix. This is a really nice feature for those people who do not want to actively manage their retirement savings.

* Full-service Investment Company. I like companies that are well-rounded and can meet all of my personal investment needs.

* On-Line Capability. I have a 401(k) from a previous employer that I have left with Fidelity. I have left it with Fidelity for a variety of reasons, but one reason is that I really like their on-line capabilities. With a single click, I can see the total value of my investments, the individual return of each mutual fund, and the year-to-date performance of my overall portfolio. I like that (but only when it tells me double-digit POSITIVE growth!).

What I Would Like To See Improved At Fidelity Investments

* Lower "initial investment required". Most of Fidelity's funds require an initial investment of $2,500. This really blocks out beginning investors. This requirement is usually removed when investing in mutual funds via a company 401(k), 403(b), or other retirement plan. However, there are a lot of people who do not have access to such a company retirement plan, and it would be very helpful if Fidelity lowered the initial investment required to $250 (like Text is American Funds and Link is http://iwasbroke.savingadvice.com/2008/04/27/the-mutual-fund-series-american-funds_38314/ American Funds).

Fidelity Investment Mutual Funds That I Own

* ZERO.

Fidelity Investment Mutual Funds That I Am Considering Purchasing

* Text is Fidelity Magellan Fund and Link is http://personal.fidelity.com/products/funds/mfl_frame.shtml?316184100 Fidelity Magellan Fund [Ticker: Text is FMAGX] and Link is http://money.cnn.com/quote/mutualfund/mutualfund.html?symb=FMAGX FMAGX] It has been around since 1963, has generated a 18.09% average annual return, and has a lower expense ratio (0.54%).

What Fidelity Mutual Funds do you own?

Read about the other mutual fund companies reviewed as part of the Mutual Fund Series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-mutual-fund-companies/ HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Mutual Fund Companies

|

0 Comments »

May 14th, 2008 at 03:10 pm

Well, this weekend the family ventured out into the wild world of tent camping at a state park in the foothills of the mountains.

It was a very cheap weekend, AND we had a blast!

Cost Breakdown

* Camp Site (2 nights): $45.10

* Food (no extra cost - we brought our regular groceries): $0.00

* Stupid Tax (left our pan at home): $14.95

Total Cost: $60.05

We had an AWESOME time. Here are the highlights.

* We put up the tent. Our tent attracts rain. It POURED both nights. BUT both days were nice and sunny.

* We saw a copperhead snake up close. That always makes me feel comfortable.

* I ate three smores in one sitting and then proceeded to cook another dozen marshmallows. INCREDIBLE!

* We saw a pileated woodpecker up close. Beautiful.

* I got to spend time with my wife and daughter without the computer, internet access, or my cell phone.

* We all got our first sunburns of the season.

* There is nothing like breakfast cooked over a campfire. Bacon sizzling. Eggs frying. 100% purple grape juice. Yum.

* Melea started the fire herself with matches. I taught her how to responsibly use matches. I hope she remembers all of the rules.

* I had to make an emergency run to a Dollar General store for a frying pan, clothesline, and clothes pins. I need to go to Dollar General more often! They really have good prices, and the store was really neat, organized nicely, and clean.

* I caught ZERO fish. First time I have been skunked all year. I don't like that.

I need to put camping on the calendar more often!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

May 13th, 2008 at 06:13 pm

I love seeing how others are using the Pay-Off and Savings Spectaculars to track their own financial progress!

Derek has a cool twist on how he is using his Home Pay-Off Spectacular.

He has some savings that he is willing to commit toward the mortgage balance (PINK). When the amount owed on the house equals that savings amount, he is going to send the savings to the mortgage to kill it off.

Way to go, Derek! Click Text is HERE and Link is http://www.derekschwab.com/2008/05/house-pay-off-spectacular.html HERE to read about Derek's Home Pay-Off Spectacular.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

May 12th, 2008 at 12:36 pm

to announce that the Sangl Family "Economic Stimulus Payment" from the IRS has arrived in our bank account. I am thrilled, excited, and, yes, PUMPED to see it show up the bank. You see, I just could not wait to receive this money! I needed this money. I was desperate for this money. I needed it to do my part to stimulate the economy.

NOT!

Because Jenn and I save for (1) emergency expenses, (2) KNOWN, upcoming expenses, and (3) our dreams, when we receive "found money" like this it is truly a blessing - not just meeting some immediate, pressing need. What are we going to do with our ESP? We are putting it into savings to fund a dream.

Boring I know.

But perhaps I should tell you how things like this used to go down. We would know that we were going to get a tax refund, so we would buy things and say, "We will pay for it with our tax refund." By the time the tax refund showed up, we had already spent it seven times over. This left us frustrated, angry, and with a pile of debt. Just writing about it makes me mad all over again. I used to be such a horrible manager of my money.

Never again.

If you are wondering what to do with your ESP, check out the "

Text is Best Utilize Your Tax Refund and Link is http://www.josephsangl.com/?cat=26 Best Utilize Your Tax Refund" series.

Posted in

Uncategorized

|

0 Comments »

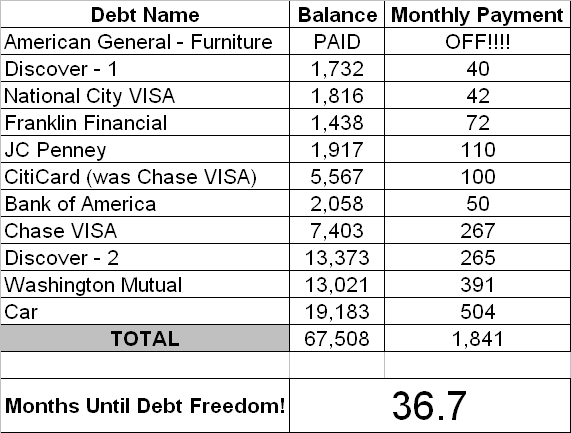

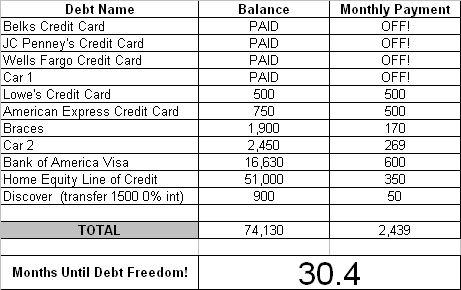

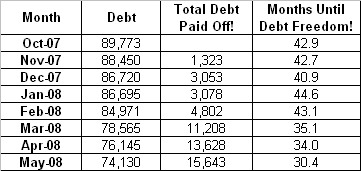

May 8th, 2008 at 02:57 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

What went well this month �

We changed car and homeowner's insurance companies saving us $672 a year! UNBELIEVABLE!

What were the challenges/struggles this month �

Well, we are so frustrated! We have called our credit card companies, and they are still not wanting to reduce interest rates. We have applied for transfers and can't get them right now b/c our balances are too high. So we are really focusing on paying these off even faster so we can tell these crooks to TAKE A HIKE! We are still calling and harassing them trying to get reduced rates - 1% here and there but it is lower than the previous month.

Updated Debt Freedom Date �

Our car balance is higher than it has been because we have the actual balance now and not a guess. Also, the Citi card stayed the same as it was a balance transfer and the Discover went up a little for the balance transfer fee.

Month By Month Progress �

Sangl Says �

When you have a pile of debt, it can take a little time to get the Debt Freedom March fully on track with a full head of steam! This is exactly what Couple #3 is experiencing. They are getting their debt balances organized and working hard to improve the interest rates on the debt. In just a couple of months, all of the restructuring will be complete, and I can not WAIT to see what happens to this debt then!

Readers �

As we all know, this is tough stuff! It is even harder when you put all of your financial information out there for the world to see. Will you encourage Couple #3 by leaving them a note in the "comments" section?

My book, I Was Broke. Now I'm Not, is available via Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM, Text is BORDERS.COM and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go BORDERS.COM, and Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL. You can read the Introduction Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book%20-%20Introduction%20P1.htm HERE.

Posted in

Uncategorized

|

0 Comments »

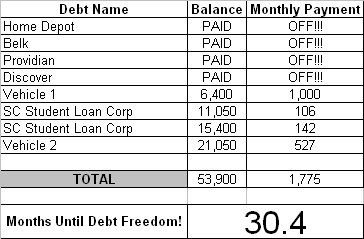

May 7th, 2008 at 03:05 pm

Introduction

This couple is THROUGH with debt! It has now been eight months since they announced that they were breaking up with debt. They have agreed to share their Debt Freedom March with everyone in the hopes to inspire others to do the same!

Here is this month's update.

What went well this month �

The whole process went well. We were able to pay more toward Vehicle 1, which is going to help us pay it off faster. We hope to keep doubling our payments, and pay it off eight months early. We kept to the cash envelopes and did not accumulate any new debt. Overall, it was a terrific month!!

Challenges and struggles this month �

We are doing so well now and we really don't face any challenges any more. We know what we need to do and we just stick with the plan.

Here is their updated Text is Debt Freedom Date and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation �

Month By Month Progress �

Sangl Says �

Couple #2 has been after their debt for just eight months, but look at how much they have gained! They have cut their "Months Until Debt Freedom" by nearly fourteen months! They have paid off $18,000 in debt! They could have used that money to go on some serious vacations, buy a new vehicle, or other fun item, but they have chosen to live this way for just a little while so that they can break the cycle of debt.

Think about what life will be looking like for Couple #2 in just a short time when they achieve debt freedom! They will free up $1,775 in monthly payments. That is TAKE-HOME pay! How much money does one have to earn to take home $1,775? About $2,500! So, Couple #2 is going to be able to give themselves the equivalent of a $30,000/year raise. WOW!

Readers �

If you dumped all of your debt (and its associated debt payments), how much of a raise could you give yourself?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

May 6th, 2008 at 06:56 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now EIGHT months into their march. How time flies!

What went well this month �

We are on plan!

What were the challenges/struggles this month �

I had to pay a large bill, but no sweat I had my emergency fund.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says �

Couple #1 has paid off nearly $15,000 in debt in the past eight months. That is nearly $2,000 PER MONTH! Unbelievable. In eight months, their Debt Freedom Date has dropped by TWELVE months. AWESOME!

Readers �

It is amazing to see what happens when a written plan is put together AND followed. You CAN do this too! Visit the free TOOLS page by clicking " Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" , and get started on your own Debt Freedom March!

You can read about my own Debt Freedom March and learn exactly how I did it in my recently released book, I Was Broke. Now I'm Not.. It is available via Text is PayPal and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PayPal, Text is Amazon.com and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& Amazon.com, or Text is Borders.com and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go Borders.com. You can read the Introduction Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book%20-%20Introduction%20P1.htm HERE.

Posted in

Uncategorized

|

0 Comments »

May 5th, 2008 at 12:32 pm

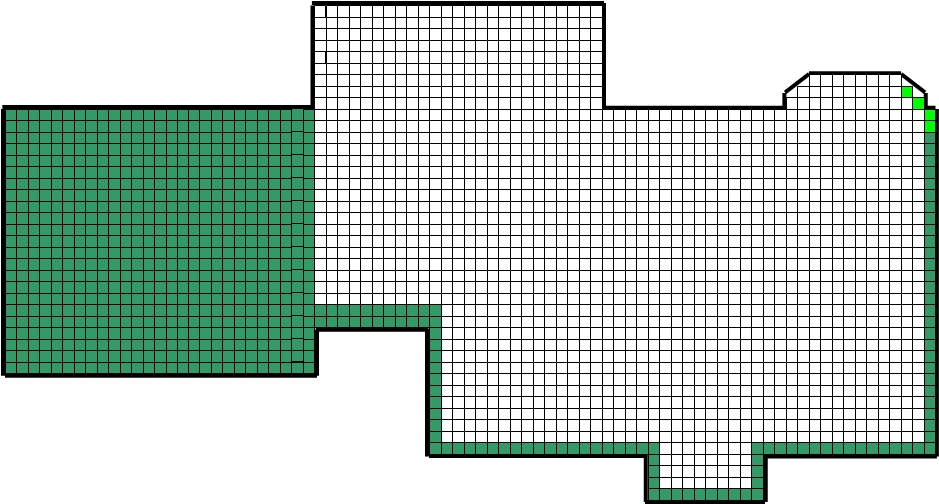

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS: 735 IS: 739

Squares Remaining: WAS: 1691 IS: 1687

% of House Owned By The Sangl's: WAS: 30.3% IS: 30.5%

% of House Owned By Wells Fargo: WAS: 69.7% IS: 69.5%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

We now own the entire south wall! For one more month, we remained on a slower path of paying off the mortgage as we prepare for known, upcoming expenses.

Frankly, it just plain stinks to slow down for a few months on this thing, but in just a little while we will be back attacking this mortgage in a way we never have before! Even though it is not fun to slow down on the mortgage payoff, it would be WAY WORSE to be slaughtering the mortgage and have a future expense derail our efforts! So Jenn and I have slowed down just for a few months to position ourselves in a way that will enable us to CRUSH this mortgage in a HUGE way.

How are you doing on YOUR house payoff spectacular? Don't have one? Get yours here => Text is Pay Off Spectacular - House and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=14 Pay Off Spectacular - House.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

1 Comments »

May 1st, 2008 at 04:04 pm

If you are moving or have recently moved, you can get a "10% Off" coupon for a purchase up to $5,000! There are a few limitations on what you can include in the purchase, but this coupon can really help!

Jenn and I used this coupon when we were in heavy "update the house" mode last year.

Get your Lowe's "10% Off" coupon Text is HERE and Link is http://www.lowesmoving.com/ HERE.

NOTE

NOTE: I figured that if Lowe's had a 10% Off deal, then Home Depot would too. A very short search showed that YES, Home Depot also has a very similar deal. One can get a "10% Off" coupon from Home Depot for a purchase up to $2,000 by registering at the Home Depot moving site. Get your Home Depot "10% Off" coupon Text is HERE and Link is http://www.homedepotmoving.com/moving/index.jsp?promocode=NORMAL#section=register&category=&module=&article=&step= HERE.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

|