|

|

|

|

Home > Archive: February, 2008

|

|

Archive for February, 2008

March 1st, 2008 at 04:57 am

A random list of great questions to ask about money �

* Can you offer this to me at a lower price?

* I'm looking for a deal. Can you also include "X" if I purchase this item today.

* If I keep managing money they way I currently manage money, will I be able to accomplish my future hopes/plans/dreams?

* Who can I bless today?

* If my wife or child had to have emergency surgery today, would I be able to absorb the financial impact?

* If I died today, would those who depend on your income be protected?

* Do I really NEED this?

* Do I work for a paycheck or am I doing what I love to do?

* Do you add huge value to your business? Why not objectively ask for a raise. Look, you delivered "X" results that benefited the company. Why not improve the income?

* What could I do with all of this money that I send toward debt payments each month?

* What does life look like without ANY payments. No house payment. No student loan payment. No car payment. No credit card payments. NO PAYMENTS!

Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

3 Comments »

February 28th, 2008 at 08:01 pm

Just 301 days from now, we will be celebrating Christmas again.

How much are you going to spend on Christmas this year?

Will you pay cash for Christmas 2008, or will you finance it?

I highly recommend planning Christmas 2008 on paper! The Text is Mini-Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=3 Mini-Budget Form (Excel) is a great tool to use to plan your Christmas spending.

Here's an example of how to use the Mini-Budget for planning Christmas. I have entered the amount that we plan to spend on each item for Christmas. This helps me understand the amount needed for Christmas.

You can see that "Cash - Expenses" shows a RED $1,080. To make it GREEN, I enter $1,080 in the "Cash Budgeted" line.

I know that I have experienced sticker-shock when I have put together my initial mini-budget for Christmas! The great thing about planning ahead is that I still have the opportunity to change how much I will spend!

So, go ahead and plan for Christmas 2008. Yes, you will be weird. Yes, no one else in your family is doing it. BUT, you will have a plan and be able to pay CASH for this year's Christmas! How many of your friends and family will be able to say that?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

2 Comments »

February 27th, 2008 at 01:53 pm

I recently discovered a new web site that is helping me save money.

It is called Text is www.RetailMeNot.com and Link is http://www.retailmenot.com/ www.RetailMeNot.com.

This web site has discount codes and promo numbers that allow you to save money at thousands of different e-tailers.

Home Depot, Wal-Mart, Victoria's Secret, Barnes & Noble � There are over 10,000 companies represented.

One thing I really like about this web site is it allows the users to rate the promo codes. If it did not work for you, you can communicate that to the next user so that they don't waste their time with it.

Try it out, and see if you can save some money!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

1 Comments »

February 26th, 2008 at 02:12 pm

I HAVE HAD ENOUGH!

I had an Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment recently.

My family traveled up to Burlington, NC to teach the Financial Learning Experience. We arrived on Saturday evening and went out to get dinner.

My lovely bride spotted a restaurant that does not exist near our home, so we went there.

It did not go well. It was 8:00 PM, but we had to wait twenty minutes to be seated.

I took one look at the menu, and began to employ my hero, Paul Marshall's method of choosing what to eat. I looked for the cheapest item on the menu and decided it was palatable.

This place sells hamburgers. HAMBURGERS. But not just any hamburger. They sell $10 hamburgers. What a RIP-OFF!

And then I see that the kid's menu has mac-n-cheese for only $4.99.

ONLY $4.99. I can buy AT LEAST twenty BOXES of mac-n-cheese for that amount of money.

I suffered through the experience. And, NO, I did not let my daughter order the ridiculous, outrageous, enormous, cruddy, massively overpriced mac-n-cheese. She had to share my $10 burger.

What a rip-off.

I am really sick of being ripped off by the so-called kid's menus at restaurants.

Who's with me?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

8 Comments »

February 25th, 2008 at 02:58 am

I have been PUMPED by the number of copies of Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/IWBNIN%20Book.htm I Was Broke. Now I'm Not. that have been sold!

Over 460 books have been shipped out in just 27 days! AWESOME!

So I have named my book an official "Sangl Times Bestseller".

Oh, and some book reviews and thoughts about Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/IWBNIN%20Book.htm I Was Broke. Now I'm Not. have been surfacing around the web.

* Rob Singleton gives his thoughts about the book and gave a copy of it away Text is HERE and Link is http://www.robsingleton.net/2008/01/27/dont-say-i-never-give-you-anything/ HERE.

* Paul Neel provides his review Text is HERE and Link is http://paulneel.blogspot.com/2008/02/book-4-i-was-broke-now-im-not-by-joseph.html HERE.

* Tally Wilgis provides a review Text is HERE and Link is http://tallywilgis.blogspot.com/2008/01/i-was-broke.html HERE.

By the way, you can also purchase I Was Broke. Now I'm Not. on Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

February 20th, 2008 at 03:28 pm

This is the latest series - "Are you STUCK?"

If you feel stuck financially, this can help you!

In part one, I asked WHY are you stuck?

Part two is Plan what you have!

Part three is Remember the priorities!

Part Four: Fill the "Go Get This" Gap

I am sure that some read this as "Go work like crazy and earn more money". I would certainly not disagree with working more and earning more! It is a GREAT way to fill in the "Go Get This!" Gap.

But there are many more ways to fill in The Gap! Here are quite a few.

* Pray. I am a Christ-follower, and I have seen the power of prayer.

* If married, ensure that your spouse is on board. There is POWER when you work TOGETHER on your finances! How do you get a spouse on board could be a year-long series, but it is so necessary. Jenn and I work together because we wrote down all of our earning and spending. When we saw that our OUTGO exceeded our INCOME, we knew that it was a serious issue! One strategy to try is to mail the kids off to Grandma & Grandpa's (eliminate distractions) and tell your spouse that you want to talk to them about something that you really need them to hear. Something that is really important to you. Very important to you. And then show them your family's finances planned out on paper. When it is written on paper, it tends to reduce the emotion toward each other and has the opportunity to become a unified effort!

* Govern your business. If your business is struggling, it might be worth putting some "mileposts" in place. Mileposts are points one month, three months, six months, and twelve months away. An example of a milepost is "If we are at $5,000 sales in three months, we will keep the business. If it is at $3,000, we will keep it open for three more months. If it is less than $3,000, we are going to have to shutter the business." The hardest thing in the world for an entrepreneur is to close their business. Tough, but necessary sometimes.

* Sell something. Maybe your house payment is eating you alive. Sell the house. Sell the motorcycle. Sell the boat. Sell the truck. Sell the swing set. Sell the four-wheeler. Sell the LCD 50" TV.

* Reduce OUTGO. Many times you can substantially lower your credit card payment just by calling them! I lowered my cable/internet bill by 75% just for calling! Get rid of the home telephone - you never use it anyway. Use cash envelopes for the categories you tend to spend impulsively (groceries, restaurants, shopping, entertainment, spending money). Call and get a new quote on your homeowner's/auto insurance.

* Chop up the credit cards. If they are a crutch that keeps trapping you, it is time to chop them up. December 2002 was the month I chopped mine!

* Make it a family effort! There is NOTHING like a unified family. Nothing.

* Pay secured debt before unsecured debt. If you can't pay everybody, consider paying just the secured debts. Call the unsecured companies and tell them that you will not be able to pay them this month, but that you fully intend to pay them. Tell the truth! There is power when you call someone and ask for help! They may or may not work with you, but when you are in bad shape financially you can't pay them if you want to!

Readers: What are some other ways to fill in the "Go Get This!" Gap?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Read the entire "Are You Stuck" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-are-you-stuck/ HERE.

Click Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE to receive each post automatically in your E-MAIL

Posted in

SERIES: Are You Stuck

|

0 Comments »

February 18th, 2008 at 03:51 am

This is the latest series - "Are you STUCK?"

If you feel stuck financially, this can help you!

In part one, I asked WHY are you stuck?

Part two is Plan what you have!

Part Three: Remember the priorities!

When you have an extremely limited amount of funds, it is important to remember the priorities. I have met a lot of people who have been tricked, guilted, and shamed by credit card companies into paying the credit card bill instead of the house payment.

You have completed step two and planned what you do have, so now the next step is figuring out who gets paid and who does not.

My priorities are:

* Essentials: House payment (or rent), basic utilities, car payment, gasoline, and food. Does NOT include cable, internet, phone, restaurants, fashion clothes, etc.

* Secured Debt: If money remains after covering the essentials, then it is time to pay for the secured debts. If secured debts are not paid, the creditor has the right to come take the item. They will usually sell it at wholesale and come after the rest from guess who? So I would pay the secured debt next.

* Unsecured Debt: They cannot immediately come take something so they can be paid later if the money runs out.

* Fun: This is last on the list.

Besides I can have fun for free. Pickup basketball games, watching old movies, etc.

Who is the manager of YOUR money? It should be YOU! Not your creditors! YOU choose where it goes.

Even if you don't have enough money to pay all of the bills, go ahead and put all of the bills into your spending plan. This is a KEY step! You need to clearly understand how large the gap is between your INCOME and your OUTGO.

I call this gap the "GO GET THIS" gap. That is the next part of the series!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Click Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE to receive each post automatically in your E-MAIL

Posted in

SERIES: Are You Stuck

|

0 Comments »

February 17th, 2008 at 01:37 am

Welcome to the newest series - "Are you STUCK?"

So � are you? Do you wonder where to begin? This series is for you.

In part one, I asked WHY are you stuck?

Part Two: Plan what you have!

Now that you have written down the reasons that you are stuck, it is time to prepare a written spending plan.

Yes, a budget. Here is something I have learned - managed money goes farther than unmanaged money.

I know that what you have is limited. In some cases, VERY limited. BUT, it is imperative that you plan what you do have.

You can obtain FREE helpful budget forms by clicking the right one for you below.

Text is Monthly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=1 Monthly Budget Form (Excel) If you are paid once per month, this is the budget tool for you.

Text is Weekly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/wp-downloadMonitor/download.php?id=2 Weekly Budget Form (Excel) If you are paid multiple times per month (twice/month, bi-weekly, bi-monthly, weekly, etc.), this is the budget tool for you.

If you want to learn how to put together a great budget, you might want to read the Text is "How Do I Budget?" and Link is http://www.josephsangl.com/?p=469 "How Do I Budget?" series.

Next we will discuss how to choose who gets paid and who does not!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Are You Stuck

|

0 Comments »

February 15th, 2008 at 03:54 pm

Welcome to the latest series - "Are you STUCK?"

Have you ever been stuck financially? I mean STUCK. Do you feel so stuck that you can't even gain any traction to get control of your finances?

Perhaps you have no income because you have lost your job. Maybe you are in college and accumulating debt to pay for it. Perhaps your spouse spends money faster than you make it. Or maybe you are just lost when it comes to managing money. It might even be the fact that you have so much unsecured debt that you feel that the creditors should just change the amount owed to a cool $1,000,000 because it might as well be that much! Maybe you are disabled, and can't figure out what to do to earn more money.

If this is you, this is a series for you!

In this series, I will be sharing steps you can take to become unSTUCK.

I am FIRED UP about this series.

Part One: WHY are you stuck?

It is important to understand why you are stuck. There are some situations that have definite ends to them (college) and other situations that have indefinite ends to them (job loss, disability, and overwhelming debt).

Why are you stuck?

Write it down on paper. Right now. Write "I am stuck financially because � ".

When I encounter situations where I don't know what to do, I start writing. Writing enables me to put all of my thoughts on paper.

After writing all of my jumbled thoughts down, I set it aside for awhile. After a day or two, I revisit what I have written and identify the repetitive thoughts. This helps me identify the core issue.

Readers: Would you comment on why you are stuck or what caused you to be stuck in the past?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Are You Stuck

|

2 Comments »

February 15th, 2008 at 03:26 am

I am FIRED UP to announce that you can now purchase my book via AMAZON.COM! Click Text is HERE and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& HERE to view I Was Broke. Now I'm Not. on AMAZON.COM.

You can also purchase my book via PayPal by clicking Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book.htm HERE.

Want to read the Introduction? Click Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book%20-%20Introduction%20P1.htm HERE.

Volume discounts are available if you are purchasing 10 or more. Contact Joe Text is HERE and Link is http://www.josephsangl.com/?page_id=2 HERE for more information.

Text is Read Recent Posts and Link is http://iwasbroke.savingadvice.com Read Recent Posts

Posted in

Uncategorized

|

1 Comments »

February 12th, 2008 at 07:26 pm

Have you read the weekly newspaper article that I have been writing for the Anderson Independent-Mail?

It is published each Sunday on the front page of the Business section.

You can read them all by clicking Text is HERE and Link is http://www.independentmail.com/staff/joe-sangl/ HERE!

This is yet another opportunity to help people take their finances to another level, and I love it!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Automatically receive each post in your e-mail by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

February 11th, 2008 at 03:42 pm

I was running on the treadmill at the YMCA (I'm training for another marathon) the other day, and ESPN was talking about baseball.

They ran the clip of Hank Aaron's 715th home run, and while watching it I saw something I had not seen before.

There, dead-center in the middle of the shot showing the home run ball leaving the park is a huge credit card billboard.

This was April 8, 1974. I remember the home run very well since I was nine days old at the time.

It was 1974 and credit cards were just taking off.

Look closely at the billboard. What does the the "Bank Americard" (now known as VISA) purport itself to be? MONEY

"Think of it as money."

Genius branding. Too many people have viewed credit cards as money, and now realize that it is really BORROWED MONEY.

By the way, you can watch Hank's home run Text is HERE and Link is http://www.youtube.com/watch?v=Z57uJv9Mxp4 HERE.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

February 11th, 2008 at 02:07 am

My first credit card was an Advanta VISA card with a really low limit.

How did I get it? I signed up for a free t-shirt during my first few weeks as a freshman on the campus at Purdue University.

What did I do with it when I received it? I went and charged it up!

It was so easy! Yet, it began a ten year mess of debt. I was a huge loser with credit cards. Maybe you have done better. Maybe not.

So my question today is:

What was YOUR first credit card?

AND

Did it help you or hurt you?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-Mail by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE .

Posted in

Uncategorized

|

3 Comments »

February 8th, 2008 at 06:01 pm

Introduction

This couple is THROUGH with debt! It has now been five months since they announced that they were breaking up with debt.

Here is this month's update!

What went well this month �

This is month five, and as you can see (from our Debt Freedom Date calculation) we are on the way to debt freedom. Joe's system gets much easier with time! We've really changed our financial lifestyle.

Challenges and struggles this month �

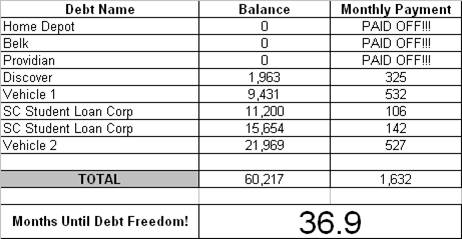

This month was fairly easy. We'd like to pay more than $325 on the Discover, but some other things came up and we had to plan for them. However, we didn't accumulate any new debt! We'll use our tax refund to pay off the Discover balance, and begin working to pay vehicle #1 off about ten months early!

Here is their updated [b] Text is Debt Freedom Date calculation and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation �[/b]

Month By Month Progress �

Anything else you want to share?

We get paid on the 15th and 30th every month. A few months ago I couldn�t wait for those checks to come in because we were dependent on them.

About three months in to this, the �pay days� became regular days.

Any challenges you want to issue to others who are reading the web site?

My wife basically dragged me to our first meeting with Joe. Our finances weren�t horrendous, but weren�t great either. We had a few thousand dollars in savings, but were living pay check to pay check with some debt. I was embarrassed for an outsider to look into our personal business. My first question to Joe was, �What qualifies you to tell me how to handle my money?� Joe briefly told his story and I began to listen and realized I wasn�t going to be judged on my past financial decisions. This put me at ease.

We�ve been doing this for 4-5 months now, and it has changed our lives. I still buy what I want, eat what I want and go where I want, it�s just budgeted. We are paying off debt quickly, and working towards financial freedom.

My point � I know someone out there is skeptical or embarrassed about their situation, its okay. Call Joe!

Sangl says �

I am so fired up by Couple #2's progress! I am ready to CRY!

Couple #2 is ON FIRE! They have been on this journey for just FIVE months, and they have already paid off $11,693! They are experiencing a time of blessing, and they are taking full advantage of this time to knock out their debt! While they did not totally eliminate a debt this month, they did reduce their debt by $1,720. Simply amazing.

Readers - What you are seeing unfold before you with Couples #1 and #2 is what I am seeing literally HUNDREDS of people do! There are HUNDREDS of people who have taken control of their finances, developed a written spending plan, and are absolutely changing their entire financial future!

Couple #2 - You guys are inspiring others to take their finances to the next level! Thank you so much for sharing!

Readers �

Have you had enough? Have you had your "I Have Had Enough" Moment? It's time to put together a plan that helps you win with your finances. You can start by putting together a written plan using one of the budget forms available on the "Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" page.

Want to read my story and learn how to take your finances to a new level? Purchase a copy of Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/IWBNIN%20Book.htm I Was Broke. Now I'm Not. I can promise you that it is written at a level you can understand and immediately apply to your finances!

Text is Read Previous Updates For Couple #2 and Link is http://www.josephsangl.com//?cat=20 Read Previous Updates For Couple #2

You can receive each post from www.JosephSangl.com FREE via E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE!

Posted in

Uncategorized

|

0 Comments »

February 7th, 2008 at 04:31 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now five months into their march. Here is this month's update.

What went well this month �

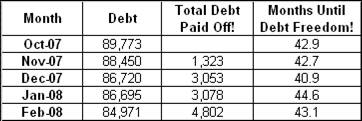

Well, it's January, and we are back on track. I am jacked because this year we are putting a lot of debt in our rear view mirror. Look for next month's update, big things are going to happen. Thank you, Joe, and thanks to all with encouraging words! It is great to do something really meaningful. Now if I can shed about 20 lbs along with my debt.

Challenges and struggles for this month �

The challenge is being impatient. I want to pay everything all at once. I must remember that I did not get here overnight, and I won't be paid up overnight. Text is I'm Not Broke and Link is http://www.josephsangl.com/IWBNIN%20Book.htm I'm Not Broke is big medicine, share it with your friends!

Updated Debt Freedom Date �

Month By Month Progress �

Sangl says �

Couple #1 PAID OFF ANOTHER CREDIT CARD! Couple #1 is making excellent progress. Based upon their update this month, I suspect that they are going to be receiving a tax refund or bonus! They also gained 1.5 months toward debt freedom! This couple are beginning to emerge from the toughest months - the beginning months. Pretty soon this is going to be second nature and this debt will start dropping like flies!

Think about it - Couple #1 has paid off $4,802 in just FIVE months! That is nearly one thousand per month! It is amazing what you can do when you have had your Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment!

Readers �

Are you receiving a tax refund this year? You might want to read the series "Text is Best Utilize Your Tax Refund and Link is http://www.josephsangl.com/?cat=26 Best Utilize Your Tax Refund" before you spend it!

Also, take a moment to consider your own personal finance situation. What would it be like to share it with the world like Couple #1 is? Will you take a moment to thank them and encourage them on their journey?

Read Previous Monthly Updates For Couple #1 Text is HERE and Link is http://www.josephsangl.com/?cat=19 HERE

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

February 7th, 2008 at 02:33 am

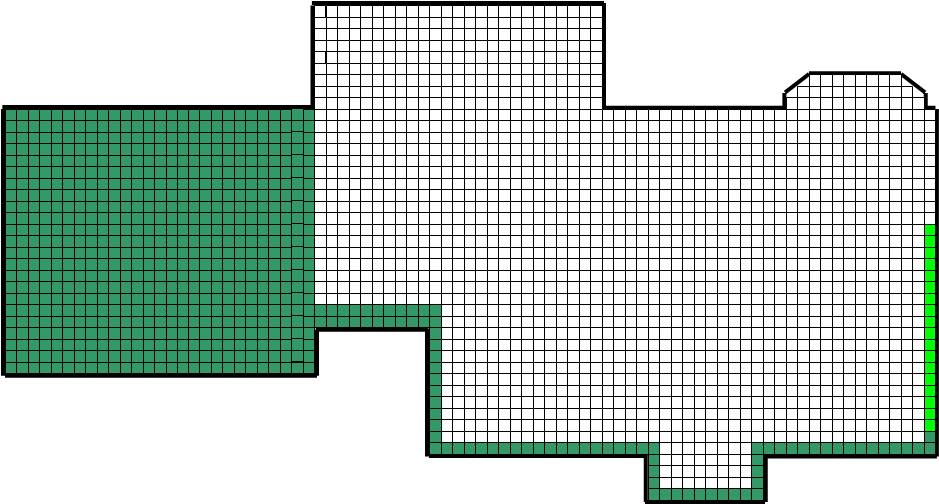

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular! The fourth monthly update is TODAY!

Jenn and I are even more fired up about getting rid of the mortgage!!! Why? Because we are one month closer to 100% freedom from debt!!! Jenn and I have shook hands and made an agreement that the house payments will be gone by October 2011. You guys will all get to watch the mortgage leave by watching the "Sangl Family Home Pay-Off Spectacular" turn green! By the way, I have a stretch goal of October 2010. It is a HUGE STRETCH.

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: 709 727

Squares Remaining: 1719 1701

% of House Owned By The Sangl's: 29.2% 30.0%

% of House Owned By Wells Fargo: 70.8% 70.0%

We now own nearly all of the side wall AND we own 30% of the house free and clear! That's exciting! Again this month we sent even more money - more than ever before - to this stupid mortgage.

I am SICK of sending HUGE interest payments to Wells Fargo. I like Wells Fargo, but I would rather they pay me interest! Who is with me?!

Text is Read previous Sangl Home Pay-Off Spectacular Updates and Link is http://www.josephsangl.com//?cat=16 Read previous Sangl Home Pay-Off Spectacular Updates

Get your own Debt Pay-Off Spectacular Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE and join the FUN!

Already debt-free? Get your own SAVINGS Spectaculars Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE.

Text is Read Joe's recent blog posts and Link is http://iwasbroke.savingadvice.com Read Joe's recent blog posts

Text is Subscribe to the feed and Link is http://feeds.feedburner.com/JosephSangl Subscribe to the feed

Posted in

Uncategorized

|

0 Comments »

February 6th, 2008 at 03:18 pm

My Text is ING Direct On-Line Savings Account and Link is http://www.jdoqocy.com/7e102js0ys-FIMJIPNMFHGKIGLOL ING Direct On-Line Savings Account dropped it's rates to 3.65% as a result of the Fed lowering rates by 3/4 of a point.

You know that you are winning with money when you are mad that the Fed is lowering interest rates!

I know that Emigrant is currently at 4.05% and HSBC is at 3.55%.

I have money in ING Direct and HSBC. Hey, 3.40% and 3.55% is WAY BETTER than the crappy 0.25% and nuisance fees that my old savings account had. Are YOU earning this type of interest on your savings? If not, you should check out these great banks/accounts.

I think I would probably be motivated to move my money if there was more than 1% disparity.

Are you a rate-chaser for your savings account money? If you are, how much is enough to make you move your money?

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Posted in

Uncategorized

|

2 Comments »

February 5th, 2008 at 04:17 pm

Welcome to the latest series at www.JoeSangl.com - Financial Software!

In Part 1, I shared the reasons that I use Text is Microsoft Money and Link is http://astore.amazon.com/wwwjosephsang-20/detail/B000SKZHM8/002-8206364-8578457 Microsoft Money.

Now I want to share how the use of this software has enabled Jenn and I to take our finances to another level.

First, let me go back a few years to explain how I discovered this software �

It was in early 2000, and I was sitting in a leadership meeting for Text is NewSpring Church and Link is http://www.newspring.cc/ NewSpring Church. It was me, Text is Perry Noble and Link is http://www.perrynoble.com/ Perry Noble, and Jason Wilson.

The new church was just getting off the ground (less than four months old), and Perry pulled out these incredible looking financial reports. When I say "incredible", I mean just that. I was floored. I was amazed about two things - (1) the incredible reports and (2) that PERRY had them!

"What �? How �? Where did you get those?", I stammered.

"Your wife printed them out for me.", Perry said.

They were INCREDIBLE! These statements were more professional than anything I had seen in Corporate America.

I asked my wife (who was the church secretary at the time) how she did it. "With Microsoft Money", she said.

I immediately switched our personal finances from my paper-based system to Microsoft Money and have never looked back.

Here is how this software has helped us take our finances to the next level:

* It made me realize how crazy we were spending our money. We were debit card kings! Everything was a debit card purchase. $2.46 purchase. $1.03 purchase. $3.21 purchase. We averaged 90 transactions per month. When we switched to cash envelopes, we cut our transactions by over 60%! We now average less than 30 transactions per month.

* It made me realize that we did not have a plan for our money. When you have to categorize an average of $500 of spending as "Miscellaneous" each month because you don't really know where it went, you have a problem! That is exactly what we were doing. By using this software, I SWIFTLY realized where it was going - the grocery store, restaurants, and impulse purchases on "wants".

* It makes me vote. When I enter paychecks, I enter the gross income and all of the deductions. When you see how much you pay in taxes on an annual basis, it will drive you to the polling booth every time you have the chance! I want to ensure that tax money is managed well.

* It helped me become even more organized. Microsoft Money (and I'm sure other personal finance software) allows you to set up recurring reminders on certain bills. It ensures that I pay them on time! AND if someone ever disputes a payment, I can quickly find the transaction and end that discussion.

* It allows me to track multiple accounts at the same time. I love having all of my financial information in one place. It allows me to quickly see a snapshot of my overall financial condition. That's a good thing!

I highly recommend that you use Microsoft Money, Quicken, or other similar software. Many times it comes already installed on your new computer. Check out your computer and see if you have it. If you do, try it out right!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Text is Receive posts automatically in your E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US Receive posts automatically in your E-MAIL

Posted in

Uncategorized

|

0 Comments »

February 2nd, 2008 at 03:38 pm

Welcome to the latest series at www.JoeSangl.com - Financial Software!

One of the keys to maximizing your financial potential is to GET ORGANIZED. Organization helps in so many ways. It helps ensure that bills are paid on time, helps you locate a financial record swiftly, and allows you to focus on "doing" instead of "searching".

I am a huge fan of financial software, and in this series I will be reviewing different types of software that is available.

I personally use Microsoft's Money Software. Microsoft recently changed the name of their Microsoft Money software to Microsoft Money Plus.

I have used Text is Microsoft Money software and Link is http://astore.amazon.com/wwwjosephsang-20/detail/B000SKZHM8/002-8206364-8578457 Microsoft Money software since 2000.

The top reasons I use this software are:

* Ease of use. Above everything else, financial software needs to be straight-forward and easy to use. Microsoft Money is exactly that for me.

* Multiple Accounts. I can manage multiple bank accounts and investment accounts within the same program

* Reports. It has tons of built-in reports that allow me to see where my money is going!

* I always know exactly how much money is in all of my accounts! This alone is worth the entire cost. I know my balance to the exact penny, and I know if a transaction has cleared the bank or not.

* When I earn or spend money, I am able to categorize the transaction. For instance, when I pull out money for my Text is cash envelopes and Link is http://www.josephsangl.com/?p=217 cash envelopes, I am able to split the transaction into multiple categories. Let's say I pull out $600. I can split the cash withdrawal into the different categories I will use the money for - $300 for groceries, $100 for clothes, $100 for spending money, and $100 for restaurants.

In the next part of this series, I will share how I use Microsoft Money to better manage my money.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Click Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE to receive each post automatically in your E-MAIL

Posted in

Uncategorized

|

1 Comments »

February 1st, 2008 at 09:44 pm

I ran across an interesting link the other day.

You type in your age and income, and it tells you how you stack up against your peers.

It is ALARMING to see how little Americans are saving!

How do you stack up? Check it out Text is HERE and Link is http://cgi.money.cnn.com/tools/networth_ageincome/index.html HERE.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

6 Comments »

|