|

|

|

|

Home > Archive: September, 2008

|

|

Archive for September, 2008

September 29th, 2008 at 08:00 pm

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Text is Part 1 - Recognize How Much A Car Really Costs and Link is http://iwasbroke.savingadvice.com/2008/09/25/series-sell-car-with-negative-equity-par_43517/ Part 1 - Recognize How Much A Car Really Costs

Part 2 - Determine Your Car's Negative Equity

Equity is determined by the following equation:

Vehicle Actual Value - Vehicle Loan Balance = Equity

If the Equity number is negative, then that means that the vehicle has negative equity.

As you prepare to sell your car, it is very important to know the actual value of the car and the actual amount owed.

I emphasize the word ACTUAL because most people tend to overestimate their car's value and underestimate what they still owe.

How does one determine how much their car is actually worth? Obtain a quote from Text is Kelley Blue Book and Link is http://www.kbb.com/ Kelley Blue Book and Text is Edmunds and Link is http://www.edmunds.com/ Edmunds. You will need to know the year and make of your vehicle including your engine type and mileage. These two sites will provide you a general idea of what used cars like yours are selling for in your area. Recognize that these are average selling prices. That means that cars are selling above and below that number, but this is the price that one can expect to sell the vehicle.

Now that you know the actual value of the vehicle, it is time to determine exactly what is owed. Contact your lender and obtain the actual pay-off balance of the car loan.

Now, use the equity calculation to determine your vehicle's equity. If it is negative, then you have a car that is known as "upside down". It has negative equity. You owe more than it is worth.

In the next part of this series, we will discuss ways to sell the car even with negative equity.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

September 25th, 2008 at 02:54 pm

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Part 1 - Recognize How Much A Car Really Costs

Some of the actions in this series might be difficult to execute, but when one recognizes how much a car really costs it can really help solidify sound financial decisions.

I believe that having a car payment is a HUGE financial mistake. Here is why.

First, cars drop in value. New cars drop in value FAST. Most new cars drop in value by around sixty percent in the first four years. This is called depreciation, and it causes one's net worth to drop.

Second, car payments reduce one's ability to gain financial freedom. Loan interest can range from 0% to 20% or higher depending upon one's credit. Even 0% loans are negative financial events because the money is going toward a car that is dropping in value. What else could one do with a monthly car payment? Give more? Invest more? Spend more?

When I recognized how much my debt was costing me, it solidified my commitment to achieving financial freedom. I was so dad-blamed sick of debt and what it was doing to my family.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

September 22nd, 2008 at 12:34 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

Good things this month

We transferred JC Penney balance which was 21.99% to a 2.9% on Discover AND we transferred Chase that was 26% to a Juniper Mastercard at 7.9%. We were VERY excited about those transfers.

It is also very encouraging to see the balance on the National City card come down!! It won't be long until that one is GONE!

Challenges this month

Challenges this month have been the rising cost of gas and food, but we have just budgeted a little differently in some areas and made it work out fine! Again, this month I have to say THANK GOODNESS for the budget form!!! We were able to pay cash for all back to school items this year and MAN! Does that ever feel good!!!

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

It is so nice to see Couple #3 reap the rewards of the hard work they put forth to Text is restructure their debt and Link is http://iwasbroke.savingadvice.com/series-restructuring-debt/ restructure their debt. Look at the tremendous progress they are making. Instead of twenty percent of their payments going toward principal and eighty percent to banks, they have switched it around. Now, over 80% of all of their payments are going toward principal reduction! AWESOME!

Readers

If you have debt, have you considered restructuring it? This can really help your debt freedom march gain a ton of traction and speed up your journey to ZERO DEBT! I encourage you to read the series of posts I wrote called Restructuring Debt.

My book, Text is I Was Broke. Now I'm Not and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not, is available via AMAZON.COM, BORDERS.COM, and PAYPAL. You can read the Introduction Text is HERE and Link is http://www.josephsangl.com/iwasbroke/ HERE. In this book, you will learn exactly how Jenn and I became debt-free in just fourteen months.

Posted in

SERIES: Debt Freedom March - Couple #3

|

0 Comments »

September 18th, 2008 at 01:31 pm

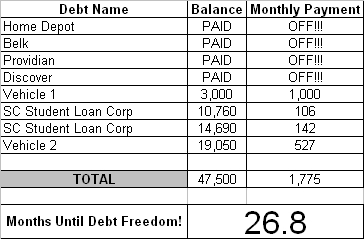

Introduction

This couple is THROUGH with debt! They announced that they were breaking up with debt in October 2007. They have agreed to share their Debt Freedom March with everyone in the hopes of inspiring others to do the same!

Here is this month's update.

We didn't put $1000 on Vehicle 1 last month which is why it only went from $3500 to $3000. We used that money for a few other things we wanted to do.

Everything is going GREAT!!!! We are still sticking to our cash envelopes and are looking forward to paying off Vehicle 1 soon!

Here is their updated Text is Debt Freedom Date and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation

Month By Month Progress

Sangl Says

This is the one year anniversary of Couple #2's Debt Freedom March and look at how much debt they have paid off! They started out in the $70,000 range and are now in the $40,000 range. They have paid off $24,410 in ONE YEAR!

I am so excited for Couple #2. They are being blessed financially and instead of running out and blowing all of it, they are using it as an opportunity to completely change their entire financial future!

Readers

Couple #2 is on a roll. You can do the exact same thing! Pull up the Text is Debt Freedom Date Calculator (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=4 Debt Freedom Date Calculator (Excel) and put together your own Debt Freedom Date!

If not now, when?

My wife and I became debt-free (except for the house) in just fourteen months, and I share exactly how we did it in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

Text is Read Previous Updates For Couple #2 and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-2/ Read Previous Updates For Couple #2

Posted in

SERIES: Debt Freedom March - Couple #2

|

0 Comments »

September 17th, 2008 at 12:58 pm

I read Text is THIS ARTICLE and Link is http://money.cnn.com/2008/09/09/news/economy/cbo_budget_update/index.htm?cnn=yes THIS ARTICLE recently on CNN.com.

I am reminded yet again of why I am on this crusade.

In the United States, we are being taxed at the highest levels ever YET the government (people that WE elect) are spending it even faster.

Guess what? Whether you are dealing with four dollars, four million dollars, or four trillion dollars the fact remains that INCOME - OUTGO = EXACTLY ZERO.

Why don't we have a balanced budget that also has debt reduction in it?

I thought about this question for a few minutes, and here are some reasons I believe we do not have a balanced budget.

* It is hard to tell ourselves "No."

* It is even harder to tell others "No." Especially people we care about.

* There are a lot of good causes out there, and we want to fund all of them.

* Elected officials who cut spending for their district run a high risk of being run out of office.

* The "I'm going to put America on a budget." campaign speech is about as appealing as the spouse who announces "We're going on a budget." Instead of thinking "financial freedom" (that's what I think of when I hear the word "budget"), most people think "NO!", "No Fun!", and "Boring" and believe that it will be incredibly restricting, constricting, and beans & rice all of the time.

* Many people do not typically think toward the future. It takes time, effort, and organization to think about the future implications of such financial management. Many Americans are hugely short of time, effort, and organization.

What are you thoughts?

Posted in

Uncategorized

|

3 Comments »

September 16th, 2008 at 06:17 pm

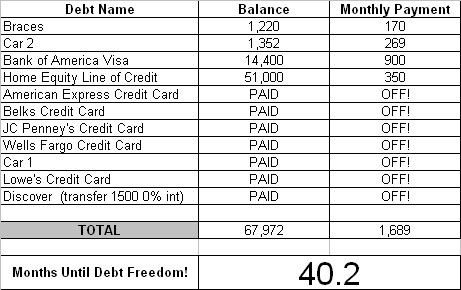

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now ELEVEN months into their Debt Freedom March.

Good/Bad This Month

This month went to plan. It is great to see these balances going down. On the other hand, it is difficult for expenses to go up so much. It seems as though all of our extra spending money is going in the tank and into the grocery cart, but I can't complain. I feel very lucky. We have a house that is not in foreclosure, and we have two great jobs with benefits and insurance. We are so blessed.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Couple #1 is now twelve months into their debt freedom march. What a fantastic year it has been! They have paid off $21,801. This is what can happen when one is intensely focused on debt freedom and recognizes what life will be like when there is ZERO DEBT.

When Couple #1 started out, they had $35,695 in non-house debt. They now have only $16,000 of non-house debt remaining. Outstanding!

Couple #1 is doing a great job of sticking to their debt freedom march. There are times that it seems almost unattainable, but it IS attainable and it IS so worth it!

Readers …

How is your own Debt Freedom March progressing?

In I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction Text is HERE and Link is http://josephsangl.com/iwasbroke/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

September 15th, 2008 at 12:57 pm

For the past several weeks, I have had an overwhelming sense of thankfulness. I am so blessed that it is hard to put it into words.

Here are some random things for which I am thankful:

* My healthy family

* The opportunity to run a marathon - not everyone has the health to even attempt one

* An emergency fund and the peace it brings to my family

* Great friends - I have met so many cool people through this crusade to help others with their personal finances

* HOPE

* Opportunity

* My friend who was diagnosed with cancer has been given a clean bill of health

* Being able to participate in life-changing work and the FLE, FFE, IWBNIN, Money Help, and other resources that help make the life-change possible.

* Volunteers who help me with this crusade. There are literally dozens of people who make this thing work.

* NewSpring Church

* Two paid-for cars that run well.

* A wife who participates in the budgeting process.

As I look at this list, I realize that many of them are interconnected. Many of them could not exist alone. But I can tell you this, as I wrote this list, my heart overflows with thankfulness, and I am overwhelmed. I simply can not believe I get to do this stuff for a living.

If you were to take three minutes to write down what you are thankful for, what would you write?

Posted in

Uncategorized

|

2 Comments »

September 11th, 2008 at 05:36 pm

As I look at my Sangl Family Home Pay-Off Spectacular, I get the very real feeling that I am mowing my lawn. (Click on the image below to see the actual spectacular.)

I am working along the outside perimeter of the house to ensure that we own at least all of our exterior walls. It makes me feel like I am mowing the lawn. I always start by mowing the outside perimeter and then work toward the center. I am certain that this is a mental game that I play, but here is why I mow my lawn with this technique (and color in the squares on the Sangl Family Home Pay-Off Spectacular).

* I want the longest and hardest part to be done first.

* As I work toward completion, the time to complete each complete pass is shorter.

* This method helps me see that I am making progress with every pass that I make.

Have you ever mowed your lawn for months or years with a small push mower and then had the opportunity to mow it with a riding mower that had a 48" deck? All of the sudden, the push mower seems totally puny and inferior. That is EXACTLY what it has felt like to slow down on our mortgage pay-off for the past six months. It felt like I had to jump off of the riding mower and start push mowing again. I am PUMPED to know that we are again back on the riding mower starting this month!

What techniques are you using to color in your Spectaculars?

If you do not have a Pay-Off or Saving Spectacular, click Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE to peruse the different ones available.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Home Pay-Off Spectacular

|

1 Comments »

September 9th, 2008 at 05:42 pm

In keeping with the completely PRACTICAL nature of this website, I thought I would provide some important reminders.

* Christmas is 107 days away

* Car tires wear out

* Water heaters fail

* Kids grow

* Debt freedom is worth every sacrifice it took to achieve

* Third-graders will enter college in ten years

* Wives appreciate nice anniversary gifts - especially the years that have multiples of 5

* Property taxes are known, upcoming expenses for those who own property

* Income is necessary to make Income - Outgo = Exactly Zero

* Payday loans are destructive to one's finances

* Purdue University did not lose a football game last week

* It is now nine days into September. Did you prepare a written budget BEFORE the month began?

What other reminders do you have?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

September 8th, 2008 at 02:59 pm

Pardon me while I rant for a moment �

For some reason, I have been encountering a lot of people lately who simply can not believe that they can become debt free.

They present numerous reasons as to why they can not become debt free - income, uncooperative spouse, children, huge home mortgage, student loans, interest rates on various loans, and the fact that it takes too long.

I agree that all of these reasons can create obstacles to achieving debt freedom, but NONE has the ability to prevent you from becoming debt free. ALL of them can be addressed. ALL of them might require tough, hard, and gut-wrenching decisions, but it is worth it to become free from debt!

If freedom from debt is your goal, you CAN do it! I believe that one of the most important things one can do when launching their Debt Freedom March is to prepare a written spending plan every single month.

If today is the day that you are going to start planning your spending, I recommend that you read the series of posts I wrote titled Text is "How Do I Budget?" and Link is http://www.josephsangl.com/category/series/how-do-i-budget-series/ "How Do I Budget?".

Chances are that if you have already launched your March To Debt Freedom, you have encountered the naysayers who say it is not possible. Stick with it! It is so worth it.

In summary, let me just say that I have been Debt-Free (Text is except for the house and Link is http://iwasbroke.savingadvice.com/series-home-pay-off-spectacular/ except for the house) and LOVING IT since February 2004.

Posted in

Uncategorized

|

0 Comments »

September 3rd, 2008 at 02:32 pm

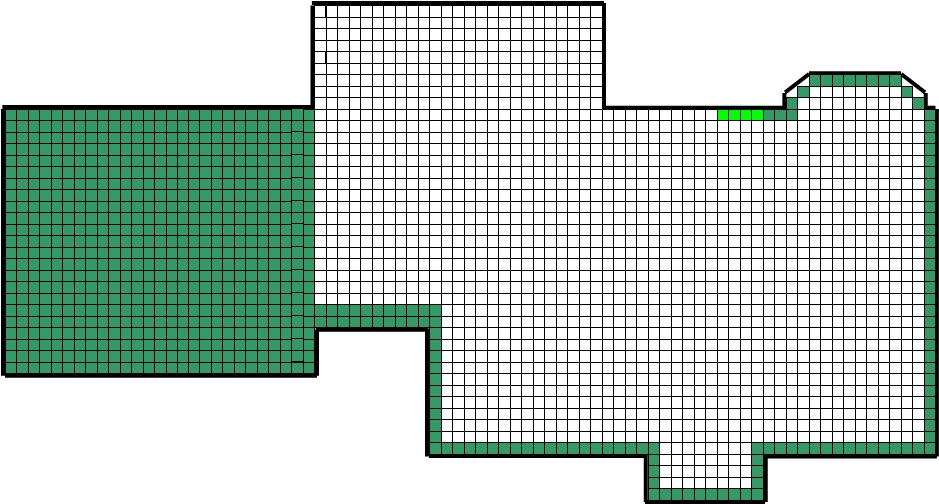

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 752 IS 756

Squares Remaining: WAS 1674 IS 1670

% of House Owned By The Sangl's: WAS 31.0% IS 31.2%

% of House Owned By Wells Fargo: WAS 69.0% IS 68.8%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger, cleaner version)

Next month, we are ramping up on the payoff spectacular again. After several months of backing off the attack on our mortgage, it looks like we will be able to sustain larger payments for the forseeable future. I am PUMPED to be able to start coloring in more squares every month!

At least eleven squares are going to be colored in this coming month due to the Text is FNBO Direct semi-finalist prize money and Link is http://iwasbroke.savingadvice.com/2008/08/11/i-can-not-believe-this_42044/ FNBO Direct semi-finalist prize money!

How are you doing on YOUR house payoff spectacular? Don't have one? Get yours here => Text is Pay Off Spectacular - House and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=14 Pay Off Spectacular - House.

Read previous Text is Sangl Home Pay-Off Spectacular Updates and Link is http://iwasbroke.savingadvice.com/cpanel/category_edit.php?category_id=3121 Sangl Home Pay-Off Spectacular Updates

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Home Pay-Off Spectacular

|

0 Comments »

September 2nd, 2008 at 12:12 am

I am not sure why I am doing this again, but I have signed up for another full marathon. That is 26.2 miles of nonstop running. That is 26.2 MILES. That is a 10K race PLUS 20 more miles!

I decided to re-read Text is THIS POST and Link is http://www.josephsangl.com/2006/05/30/how-a-marathon-is-like-personal-finances/ THIS POST I wrote before I ran my first full marathon back in June 2006. I found myself saying "Amen." and "Absolutely." as I read that post. (Sidenote: Is it OK to do that for stuff you have written yourself?)

On Sunday, January 18, 2009 @ 7:00AM, I will embark on another marathon with 18,000 runners in the Chevron Houston Marathon in Houston, TX. The great thing is that I will have two brothers running with me (the other three are slackers). If, strike that, WHEN we all finish, we are going to Ruth's Chris Steakhouse for a fine celebration meal.

There are so many parallels between marathon training and personal finances. Not the least of which is self-discipline. Look for a ton of posts focused on my training and how I feel that it relates to personal finances over the next several months.

I have started training several months ago, but the formal training program begins September 15th.

I ran my last marathon in 4 hr 27 min 35 sec. My goal this time? 4 hr 10 min 00 sec

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

|