|

|

|

December 4th, 2008 at 10:06 pm

I believe that the greatest economic stimulus package that could have ever been implemented is LOWER GAS PRICES.

Seriously. I believe that super-high gas prices forced people to trim their spending to essentials and to restructure their spending - including eliminating gas hogs. Now that gas prices have eased there is extra money each month.

I do not know about you, but I saw a ton of people at Wal-Mart on Black Friday shopping with cash.

The average American family is getting an extra $50 to $200/month simply because of lower gas prices. That equates to an extra $600 to $2,400/year.

What do you think?

Posted in

Uncategorized

|

4 Comments »

December 2nd, 2008 at 04:38 pm

I am PUMPED about 2009! This crusade takes tons of people to make it work, and I am so honored that so many of you have participated in or volunteered to serve at one our events.

Here are the cities that the crusade will be visiting in the first three months of 2009.

* January 17 & 18 Houston, TX

* January 24 & 25 Royersford, PA (Philly area)

* January 28 Ottumwa, IA (Des Moines area)

* January 31 & February 1 Cheyenne, WY

* February 7 & 8 Dallas, TX

* February 22 Canton, GA (Atlanta area)

* March 7 & 8 Acworth, GA (Atlanta area)

* March 12 & 15 Anderson, SC

* March 22 Lakeland, FL (Tampa area)

I am also stoked to see that the crusade will be traveling in ways that do not require me to travel! The Text is I Was Broke. Now I'm Not. Group Study and Link is http://groupstudy.iwasbrokenowimnot.com/ I Was Broke. Now I'm Not. Group Study is being implemented into small groups and medium size groups in dozens of churches.

That PUMPS ME UP! I am so honored that I get to serve so many people, churches, and businesses and be a part of life changing work.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

December 1st, 2008 at 02:01 pm

The IWBNIN Team is pumped to offer the following Christmas 2008 Special to those of you who are on this crusade to help others accomplish far more than they ever thought possible with their personal finances.

Through December 18th, you can purchase 10 copies of I Was Broke. Now I’m Not. for $100 and shipping is FREE! To purchase these materials, click Text is HERE and Link is http://www.josephsangl.com/2008/11/18/christmas-2008-special/ HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

November 24th, 2008 at 01:49 pm

One of the most common questions I am asked is:

"Should I get a home equity loan to pay off all of my non-house debt?"

Here is my response.

I am not a big fan of consolidating one's non-house debt into a home equity loan. This is for several reasons, and I have outlined those reasons below.

* This is addressing a symptom, not the root cause. This question is usually motivated by our need for immediate action. It is the same motivation that causes us to purchase a car and finance it for five years.

* Borrowing from home equity makes it more difficult to sell the house. This is especially true in today's house market. There are a ton of people who now owe more on their house than it can be sold for. Consequently, they become trapped in the house.

* Changing spending behavior is a process. If one runs out and consolidates their debts, it might remove the urgency from the need to change spending behavior. Changing one's spending behavior takes time. I am convinced that if I had obtained a home equity debt consolidation loan in December 2002, I would not have changed my spending behavior. However, because it took fourteen months to address our debt, our spending behavior was completely changed. We have never looked back!

Having spoken with thousands of people and working one-on-one with nearly one thousand people in the past two years, I am convinced that obtaining a home equity loan is not the best way to eliminate debt. The most common result from obtaining a home equity loan is less equity in the house and the consumer debt shows back up because the spending behavior was not changed.

This is, in fact, my own story. I obtained a debt consolidation loan to move a pile of credit card and consumer debt to one payment. After paying $315.60 a month for an eternity, I wanted to celebrate, but I could not. Why? Because while I had finally paid off the debt consolidation loan, I had not changed my spending behavior and my credit card debt had grown back to more than I had consolidated in the first place!

What do you think?

Text is Read Recent Posts and Link is http://iwasbroke.savingadvice.com Read Recent Posts

Related Tools/Articles

* Text is Debt Elimination Tools and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/debt-freedom-date/ Debt Elimination Tools

* Text is SERIES: "How To Pay Off Debt" and Link is http://www.josephsangl.com/category/series/how-to-pay-off-debt-series/ SERIES: "How To Pay Off Debt"

Posted in

Uncategorized

|

2 Comments »

November 21st, 2008 at 02:57 am

This is a series written for those who are struggling mightily with their finances and tough decisions are being made about who will be paid and who will not be paid. It is my hope that this series will provide practical steps that can be taken to walk out of this situation and into financial freedom.

Part 4 Take Action!

I have found that whenever I am overwhelmed, I move toward doing nothing. I just want to shut down and ignore everything. Running away feels like the right thing to do.

Yet, the FACT is that running away will just make the situation worse. Will it be extremely difficult to work through this situation? AB-SO-LUTE-LY! But the cost of NOT doing something is even more difficult! You CAN do this.

Below are some practical tips that have worked for me when I have wrestled with overwhelming situations.

* Action List I prepare a list of items and prioritize them

* Establish accountability Someone who I trust who will hold me accountable to my actions

* Seek Help Here at NewSpring Church, we provide FREE one-on-one financial counseling for over 500 people each year. We provide this service on-site at all of our campuses. You can request this free counseling Text is HERE and Link is http://www.josephsangl.com/?page_id=2 HERE. We will not try to sell you anything. Our counselors are winning with their money and are passionate about helping folks do the same!

Text is Read the entire series and Link is http://iwasbroke.savingadvice.com/series-help-i-cant-pay-my-bills/ Read the entire series

Posted in

SERIES: Help! I Can't Pay My Bills.

|

0 Comments »

November 18th, 2008 at 06:29 pm

This is a series written for those who are struggling mightily with their finances and tough decisions are being made about who will be paid and who will not be paid. It is my hope that this series will provide practical steps that can be taken to walk out of this situation and into financial freedom.

Part 3 Prioritize

When the financial sky is falling down and the walls are closing in on you, it is imperative that spending is prioritized. Here is my suggested order of priority for spending when there just is not enough to pay everything.

1. Housing Must take care of the mortgage and utilities first. Now if the mortgage payment has run out of control and it is 60% of one's take home pay, then it is high time that the house be sold or income be tripled within a couple of months.

2. Food I am going to eat before one single bill is paid! We must be able to eat. I am not talking about Olive Garden or fast food. I am talking about groceries bought with coupons and much attention to frugality.

3. Transportation If transportation is required to produce income, then it is imperative that the vehicle payments, insurance, taxes, gasoline, and maintenance be funded.

4. Back Taxes Owing the government back taxes is a terrible thing, and it must be addressed. I would rather owe anyone besides owing Uncle Sam!

5. Secured Debts If there is additional money remaining after Housing, Food, and Transportation are taken care of, it is time to pay the secured debt payments. This is debt where the lender can come take something - like a car, boat, motorcycle, tractor, etc. If the lender repossesses the item, they will sell it at a wholesale auction and come after you for the difference.

6. Family & Friends Debts If you owe family and friends and you still have some money left, it is essential to pay on debts owed to family and friends. Unpaid debts to family and friends has been the cause of untold relationship issues since time began. Avoid this!

7. Unsecured Debts It is time to address the unsecured debts. Credit cards, student loans, signature loans, etc. One thing to note is that unsecured debt holders will be screaming and hollering the loudest because there is nothing they can come take from you. As a result, they will try to play upon your emotions to get you to pay them before you pay anyone else. And it works! I have met with a lot of people who have kept their credit cards current while letting the house payments fall behind. Not good!

Go back to the spending plan you have prepared and ensure that your priorities are in order.

Posted in

SERIES: Help! I Can't Pay My Bills.

|

0 Comments »

November 17th, 2008 at 02:17 pm

This is a series written for those who are struggling mightily with their finances and tough decisions are being made about who will be paid and who will not be paid. It is my hope that this series will provide practical steps that can be taken to walk out of this situation and into financial freedom.

Part 2 Ask Questions

It is extremely important to ask questions that help define the true root cause of the issue.

When I am counseling someone experiencing this sort of situation, I have a series of questions I ask to help me grasp the issues. Here are some of the questions for which I am seeking answers. These are not in any particular order.

* "What was the cause of this situation?" Ultimately, I am trying to determine if the current situation is the result of a long series of financial decisions or the result of a catastrophic event (job loss, medical issue without insurance, death of income provider, etc.)

* "Is this an INCOME or an OUTGO issue?" I want to see where the money is going. That is why Text is Part 1 and Link is http://iwasbroke.savingadvice.com/2008/11/13/help-i-cant-pay-my-bills-part-1_45058/ Part 1 is so important. The spending plan will help you more clearly determine the answer to this question. From experience, I have seen that it is an OUTGO issue in most cases.

* "What are the required debt payments?" Is this unsecured revolving debt (credit cards) or is this installment debt on an asset (car, boat, motorcycle, etc.)? This question will be key for Part 3 of this series.

* "Is there something that can be sold?" If there are items that can be sold, this needs to be fully investigated to understand how it can help the situation.

* "What expenses can be stopped?" Are there any "extras" in the OUTGO?

* "How can INCOME be increased?" An extra job or tons of OT may not be appealing, but living in a squalor of debt with no hope is even worse! It is very important to investigate short-term ways to increase income to get out of the current late bill payment situation.

Readers: What other questions would you add to this list?

Posted in

SERIES: Help! I Can't Pay My Bills.

|

0 Comments »

November 13th, 2008 at 01:40 pm

Welcome to the latest series - "Help! I Can't Pay My Bills."

This is a series written for those who are struggling mightily with their finances and tough decisions are being made about who will be paid and who will not be paid. It is my hope that this series will provide practical steps that can be taken to walk out of this situation and into financial freedom.

Part 1 Prepare a written spending plan

There is so much power in a written spending plan! I never realized where all of my money was going until the day that I began planning my spending.

You might say, "But Joe, I know that the outgo is more than my income so why should I even bother with preparing a spending plan?"

I would respond with this answer. "It is hard to slay a dragon if you do not know how many heads it has!" A spending plan will ensure that you know the ACTUAL situation instead of the IMAGINED situation.

So go ahead and prepare your plan - even if you know it is going to be awful. This is the start of your journey to financial freedom!

You can use the free budget tools Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com/tools/ HERE to get started on your plan.

Helpful Tools/Articles

* Text is FreeBudget Tools and Link is http://nextsteps.iwasbrokenowimnot.com/tools/ FreeBudget Tools

* Text is "How Do I Budget?" Series and Link is http://www.josephsangl.com/category/series/how-do-i-budget-series/ "How Do I Budget?" Series

Posted in

SERIES: Help! I Can't Pay My Bills.

|

0 Comments »

November 6th, 2008 at 07:33 pm

I am a HUGE fan of savings. I used to live with an average bank balance of $4.13, and I thought that we were doing really good because we had paid all of the bills on time.

The fact was that every single time life happened, our finances were crushed.

So today's question is: "Are You Prepared?"

As I share in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not., my family has experienced its fair share of "life happens" events. Here are some of them.

* Hospital My daughter could not breathe and went to the emergency room.

* Car Part Repairs The car broke down. Multiple times. Repairs included power steering rack, AC failure, ignition switch, and water pump.

* Car Body Work The car was involved in an accident with our truck. Yes, one of us in our family was backing up the car and scraped it along the side of the truck. We also had a small fishing boat fall over and hit our car leaving a huge dent.

* Appliances The dryer died.

* Healthcare Jenn had to have major surgery in 2003. Just ten months later, she had to have major surgery again. In 2007, I had hernia surgery. Now, Jenn has just had surgery again.

* House Repairs We purchased a thirty year old house in 2007. It required lots of repairs. LOTS more than we originally anticipated.

* Emergency Trips For death in the family.

We have experienced lots of "life happens" events that have cost a ton of money. Before December 2002, we would have just pulled out the credit card to cover these types of events. Since December 2002, we have been prepared with a fully-funded emergency fund.

Are YOU prepared?

Posted in

Uncategorized

|

2 Comments »

November 4th, 2008 at 04:45 pm

I am a big fan of receiving money for doing something that I already do, and that is why I am pumped about Swagbucks.

Let me tell about Swagbucks. It is a search engine that you use to find stuff on the internet. By signing up for and using Swagbucks for your internet searches, you can earn Swagbucks - a currency that can be converted into rewards ranging from five dollars to hundreds of dollars.

A single Swagbuck has a value of around $0.08, but it can add up! At the rate I have been earning Swagbucks, I believe that I will be able to obtain a $50 gift card every three months or so.

Based on what I have seen, Swagbucks returns the same results as Google.com but pays you to use it!

You can register for your own Swagbucks account Text is HERE and Link is http://swagbucks.prodege.com/?cmd=sb-register&rb=200791 HERE.

Find dozens more budget boosting ideas on the Text is Next Steps and Link is http://nextsteps.iwasbrokenowimnot.com/reward-programs/reward-programs/ Next Steps site.

Posted in

SERIES: Next Steps

|

1 Comments »

November 3rd, 2008 at 02:11 pm

I am PUMPED about Text is Next Steps and Link is http://nextsteps.iwasbrokenowimnot.com/ Next Steps, the newest division of IWBNIN. In this series, I will be sharing different components of this division which is solely focused on providing practical next steps toward financial freedom.

Eliminate Debt

The Text is Eliminate Debt and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/ Eliminate Debt section was developed to help folks develop a plan that will allow them to become 100% debt-free. I was in debt up to my eyeballs, and my bride and I made a commitment in December 2002 to rid ourselves of debt. In just fourteen months, we became debt-free except for the house and are now well on our way to eliminating the mortgage!

You can become debt-free too, and the Eliminate Debt section was prepared especially for you.

Here are the pages located in the Eliminate Debt section.

* Debt Freedom Date This page is focused on helping you understand your debt situation. There are links to obtain your free credit report (it truly is FREE), calculate your debt freedom date, calculate the actual cost of your debt, and an early pay-off calculator.

* 0% Interest Balance-Transfer Credit Cards I am not a fan of credit cards at all, but if you are carrying a balance and paying interest - why not surf the balance to a 0% card? That way ALL of your payment is applied toward the debt! We have searched the internet to find cards that charge a minimal transfer fee, but allow you to transfer the balance and pay 0% interest for an entire year. There are even a few cards that allow you to transfer the balance with no transfer fee.

* Debt Pay-Off Spectaculars Yes, these are also located in the Free Tools section, but for your convenience we have also located the page in the Eliminate Debt section.

Back when I was swimming in debt, I asked myself the two following questions that changed my life forever.

* "How much do I pay each month to debt?"

* "What else could I do with this money?"

Use the Next Steps Eliminate Debt section to get started on your own Debt Freedom March!

Text is Read more of the series on Next Steps and Link is http://iwasbroke.savingadvice.com/series-next-steps/ Read more of the series on Next Steps

Posted in

SERIES: Next Steps

|

0 Comments »

October 30th, 2008 at 05:07 pm

I am PUMPED about Text is Next Steps and Link is http://nextsteps.iwasbrokenowimnot.com/ Next Steps, the newest division of IWBNIN. In this series, I will be sharing different components of this division which is solely focused on providing practical next steps toward financial freedom.

Free Tools

The Free Tools are organized into logical subgroups (sorry, some of my engineering nerdiness there  ) )

Here are some of the sections in the Text is Free Tools and Link is http://nextsteps.iwasbrokenowimnot.com/tools/ Free Tools section.

* Budgeting Tools Monthly; Weekly; Bi-Weekly; Bi-Monthly; Specific Project or Event - Every budget tool you may need can be found on this page.

* Debt Reduction Tools Calculate your Debt Freedom Date and Actual Cost of Debt here. You can also use the Early Pay-Off Calculator to find out how much sooner a larger payment will make a debt leave!

* Calculators Chances are really good that the financial calculator you need is located on this page.

* Saving Tools Find out how much your monthly savings can equal in a few years on this page.

* Pay-Off Spectaculars These are some of the most popular tools, and this page takes the spectaculars to an entirely new level. There are now thumbnail pictures of each spectacular for you!

* Saving Spectaculars As with the Pay-Off Spectaculars, the Savings Spectaculars have been reorganized for ease of use.

I am PUMPED about Next Steps and the opportunity to help you take practical next steps toward financial freedom!

Read more of the series on Next Steps Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com HERE

Posted in

SERIES: Next Steps

|

0 Comments »

October 29th, 2008 at 12:43 pm

On October 3, 2008, I announced the formation of a new division of IWBNIN called Text is Next Steps and Link is http://nextsteps.iwasbrokenowimnot.com Next Steps.

For the next several days, I will be sharing some specifics about this new division.

Vision

It is my passion to help people accomplish far more than they ever thought possible with their personal finances so that they can be freed up to go do EXACTLY what they have been put on earth to do.

As I speak and teach about personal finances, I receive many questions like "Who do you recommend?" and "Where would you go?" Next Steps was created to answer these questions and provide practical next steps for those seeking to take their finances to a new level.

Prepare A Plan

The "Text is Prepare A Plan and Link is http://nextsteps.iwasbrokenowimnot.com/prepare-a-plan/ Prepare A Plan" link was created to share the key items that I believe are fundamental for a sound financial plan. These items include:

* Planned Spending It is so important to have a written plan! This link leads to a page chock full of budgeting tools.

* Freedom From Debt Want a huge pay raise? Eliminate the debt payments, and it will free up a ton of money! This link leads to the debt freedom date calculator, actual cost of debt calculator, and an early pay-off calculator.

* Saving & Investing I love saving and investing! This is what will allow me to accomplish my plans, hopes, and dreams. This page leads to links for high-interest paying on-line savings and checking accounts, mutual fund investment companies, and 529 college savings plan links.

* Insurance Insurance can be frustrating. This page was created to make it easy to obtain multiple quotes with just a few minutes of effort! The average annual savings on auto and home insurance for folks who have not obtained a new quote in the last two years is nearly $600. That will spend just like money!

* Leaving A Legacy According to Bankrate.com, 57% of Americans do not have a written will. This means that the government will be left in charge of determining who gets what! This page was prepared to help you get a written will at a very reasonable cost.

Read more of the series on Next Steps Text is HERE and Link is http://iwasbroke.savingadvice.com/series-next-steps/ HERE

Posted in

SERIES: Next Steps

|

0 Comments »

October 28th, 2008 at 05:54 pm

Before this moment, there were four key ways this crusade was carried out:

* Speaking (Churches, Businesses, and Civic Organizations - Upcoming Events Text is HERE and Link is http://www.josephsangl.com/upcoming-events/ HERE)

* Teaching (Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience, Text is Financial Freedom Experience and Link is http://www.josephsangl.com/FFE%20Details.htm Financial Freedom Experience)

* One-On-One Financial Counseling (Financial Counseling Experience)

* Resources (Text is I Was Broke. Now I'm Not. and Link is http://nextsteps.iwasbrokenowimnot.com/purchase-resources/joe-sangls-book/ I Was Broke. Now I'm Not. and its Text is Group Study and Link is http://groupstudy.iwasbrokenowimnot.com/ Group Study)

Today, I am PUMPED to introduce a fifth way that this crusade is carried out: Text is NEXT STEPS and Link is http://nextsteps.iwasbrokenowimnot.com/ NEXT STEPS

Let me tell you how this newest part of the crusade came about.

First I will start by reiterating my passion. It is my passion to see others accomplish far more than they ever thought possible with their personal finances. The reason I am so passionate about this is because I believe that when people are financially free, they are much more likely to go do EXACTLY what they have been put on this earth to do.

As I partner with churches and businesses throughout the nation to help teach PRACTICAL personal finance tools, my passion and this vision drives me to constantly ask the question, "What is a PRACTICAL next step that we can offer folks?"

Let me be more specific.

* "After this message series on money, what is the PRACTICAL next step we can offer to help people take their finances to the next level?"

* "After Joe speaks at our business, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

* "After the Financial Learning Experience or Financial Freedom Experience, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

* "After someone reads I Was Broke. Now I'm Not., what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

* "After someone participates in the I Was Broke. Now I'm Not. Group Study, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

Next Steps is a website created to answer these questions. Over the next several weeks, there will be several series written about the practical tools and solutions that we have placed on the site. I encourage you to check it out Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com HERE, and see if there are ways that can help you achieve YOUR next steps!

Posted in

SERIES: Next Steps

|

0 Comments »

October 27th, 2008 at 01:44 pm

This is a series about a certain purse owned by the Sangl Family. Unlike every other series I have written, I am NOT excited to be writing this one.

Part 5 - A Final Word

Losing a purse is terrible, but it happens. It has caused me to give serious thought to the actions one should take when personal items go missing. I have made a list of the actions I took and some I was preparing to take once we knew the purse was lost.

* Stopped all debit cards (should stop credit cards too if you have them)

* Placed stop-payment on all checks in the checkbooks

* File a police report to let them know you have misplaced an item. I am told by the bank that many recovered items end up being taken to a police station.

* Cut off the cell phone number from the phone

* Place an alert on your credit report. You can do so by contacting one of the three credit reporting agencies (TransUnion, Equifax, or Experian) and placing a "fraud alert" on your account. This will require the credit reporting agencies to actually make contact with you before a new line of credit can be opened. The person at the bank recommended Experian because they are open for twenty-four hours. You can click Text is HERE and Link is https://www.experian.com/consumer/cac/InvalidateSession.do?code=SECURITYALERT HERE to access Experian's Fraud Alert page.

* Contact the Social Security Administration if your SSN has been compromised. You can click Text is HERE and Link is http://www.ssa.gov/oig/guidelin.htm HERE to visit the SSA's Fraud page.

I hope this sort of event never happens to you! If it does, I hope it turns out as well as this situation has for us.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Text is Read the entire "Lost Purse" series and Link is http://iwasbroke.savingadvice.com/series-the-lost-purse/ Read the entire "Lost Purse" series

Posted in

SERIES: The Lost Purse

|

1 Comments »

October 23rd, 2008 at 02:56 pm

This is a series about a certain purse owned by the Sangl Family. Unlike every other series I have written, I am NOT excited to be writing this one.

Part 4 - The Conclusion

On Wednesday this week, Jenn received a package at the house! Below is a picture!

The purse with ALL of its contents - including cash, iPod, cell phone, and the kitchen sink were still there!

I am so humbled by the honesty of all the people who saw the unattended purse and left it alone, and we are blown away by the kindness and quick action of the McDonald's staff at the following address:

McDonald's 331 Harding Place Nashville, TN

I called the manager of the McDonald's that same day and profusely thanked them for their kindness and told her of her employee's great work.

The reward has been mailed. It is substantial, and it is worth it.

We are so blessed.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Text is Read the entire "Lost Purse" series and Link is http://iwasbroke.savingadvice.com Read the entire "Lost Purse" series

Posted in

SERIES: The Lost Purse

|

4 Comments »

October 22nd, 2008 at 02:49 pm

This is a series about a certain purse owned by the Sangl Family. Unlike every other series I have written, I am NOT excited to be writing this one.

Part 3 - A Chance

Jenn was devastated over the loss of her purse. I gave her some money to go get the Chinese food and started unloading the car.

About ten minutes after Jenn had left, my cell phone rang with the caller ID reading "Jennifer Sangl". I thought, "Jenn has found her phone!"

I answered the phone and said, "Jenn! You found your purse!"

A voice on the other end said, "Hello?"

Short story - the caller was the McDonald's employee. They had went out in the lobby and Jenn's purse was still sitting IN THE LOBBY. It had been there for over seven hours!

I asked the caller to tell me her name and told her that if she would mail it to me, there would be a reward. I think she is a teenager - she had no clue about how to mail something. No clue! I had to walk her through exactly how to mail it.

That was on Sunday evening.

On Monday, late in the morning, I received another phone call from Jenn's phone. The girl was at the post office to mail the purse! She said, "I have no money. Can I use some of the money in the purse?" Apparently, the money was still in the purse!!!

My answer? AB-SO-LUTE-LY!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Text is Read the entire "Lost Purse" series and Link is http://iwasbroke.savingadvice.com/series-the-lost-purse/ Read the entire "Lost Purse" series

Posted in

SERIES: The Lost Purse

|

4 Comments »

October 21st, 2008 at 06:15 pm

This is a series about a certain purse owned by the Sangl Family. Unlike every other series I have written, I am NOT excited to be writing this one.

Part 2 - The Panic

Upon discovery that the purse was missing, I immediately logged in to our bank accounts to see how much of our money was missing with fraudulent charges. $0 of unexpected charges were there. Whew!

I then had Jenn prepare a list of everything that was in the purse. It was a mile-long list.

I called the bank and had them shut off the debit cards. The person at the bank was extremely helpful. I could not believe how helpful they were!

Then I tried to remember where exactly the McDonald's was. I remembered that there was a Red Box outside the store that was not working. I looked up on Red Box's website to find the McDonalds in the Nashville area. There were none that made sense.

So I pulled up Google Maps and searched "McDonald's Nashville, TN". I found two that were located about where I thought we had pulled off. When I zoomed in on the "Satellite" view, I was able to narrow in on the store.

I called the store and confirmed that they had a Red Box outside that was not working and the type of interior the store had. I asked them if a purse had been turned in. They said, "Yes!" I was PUMPED! Then they told me that it was actually a backpack with a bunch of clothes in it. I was SAD!

They said that they did not have a purse, but that I should call back each day to see if it were turned in. Right. Like that is going to flippin' work!

Oh - one more thing - did I mention that Jenn left her cell phone in her purse? Now we have no purse, all the cash is gone, the iPod is gone, the checkbooks are gone, our old Purdue college IDs are gone. It is ALL gone.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Text is Read the entire "Lost Purse" series and Link is http://iwasbroke.savingadvice.com/series-the-lost-purse/ Read the entire "Lost Purse" series

Posted in

SERIES: The Lost Purse

|

2 Comments »

October 20th, 2008 at 12:27 pm

This is a series about a certain purse owned by the Sangl Family. Unlike every other series I have written, I am NOT excited to be writing this one.

Part 1 - The Loss

If you follow me on Text is Twitter and Link is http://twitter.com/jsangl Twitter, you know that Jenn and I traveled to southern Illinois recently to celebrate her grandfather's 90th birthday party. It was a wonderful trip. Her grandfather is a real-life WWII and Korean War hero. He was machine gunned down in WWII in the Battle of the Bulge and fought in the Koren War too. He is an amazing man, and it was our honor to attend his birthday party.

Anyway, we headed home on Sunday. It was about a nine hour drive home. We stopped and grabbed some lunch at a McDonald's just outside of Nashville, Tennessee. We then stopped one more time for some gas. As we arrived home at around 8PM on Sunday evening, I told Jenn that it would be great to grab some Chinese food.

Jenn said, "No problem. I will unload the car while you go pick it up. Let me get you some cash for the food."

She reached down to grab her purse, and the feeling of dread set in. She immediately knew that it was not in the car and that it had to be at the McDonald's that we had stopped at nearly SIX HOURS ago.

Panic might be an understatement. Many of our cash envelopes were in the purse. It also contained debit cards, checks, an iPod, and a lot of other stuff. Frankly, I could not believe everything that Jenn said was in that purse. Ladies who read this blog - HOW do you fit all of that stuff in your purses?????

So ... what do you do when you lose your purse?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: The Lost Purse

|

3 Comments »

October 16th, 2008 at 01:03 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

Good things this month

We are seeing balances come down due to making higher payments (National City) and lower or no interest on the others! YEAH!!!!

Challenges this month

Still gas prices … BUT we have restructured our schedules to only run errands once a week if possible and it has really helped out!

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

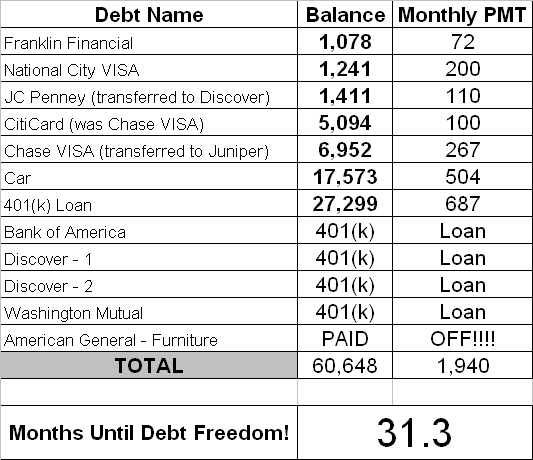

You can see the progress being made by Couple #3 now! There were several months where the debt was being restructured by transferring credit card balances to 0% and low interest rate credit cards. Now that all of that money is going directly to the principal, look at how swiftly they are dropping!!! Couple #3 dropped their debt by a huge amount last month! Outstanding.

Readers

Are you paying high interest on your credit cards? Move the balances to zero percent and low interest cards! That can really help one gain traction toward debt freedom. There are several 0% balance transfer credit cards available on the Text is Next Steps and Link is http://nextsteps.iwasbrokenowimnot.com/ Next Steps page.

My book, Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not., is available via Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM, Text is BORDERS.COM and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go BORDERS.COM, and Text is PAYPAL and Link is http://www.josephsangl.com/iwasbroke/ PAYPAL. In this book, you will learn exactly how Jenn and I became debt-free in just fourteen months.

Posted in

SERIES: Debt Freedom March - Couple #3

|

0 Comments »

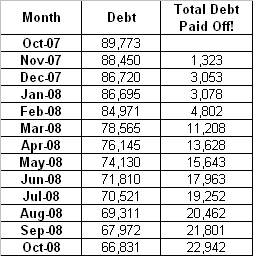

October 15th, 2008 at 02:39 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now over a year into their Debt Freedom March.

Couple #1's Thoughts This Month

I am so thankful for your help and encouragement in these tough times. If we were carrying our previous levels of debt it would be stressful to say the least. We are seeing our 401k shrivel but we all know that will return with time and stability. I only hope Americans now see that being in debt is dangerous combination of timing and chance.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Another boring month of debt reduction … Couple #1 has figured this thing out. They have a plan that is working, and that means more debt has left. Way to go!

Readers

How is your Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction Text is HERE and Link is http://josephsangl.com/iwasbroke/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

October 14th, 2008 at 12:43 am

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Text is Part 1 - Recognize How Much A Car Really Costs and Link is http://iwasbroke.savingadvice.com/2008/09/25/series-sell-car-with-negative-equity-par_43517/ Part 1 - Recognize How Much A Car Really Costs

Text is Part 2 - Determine Your Car's Negative Equity and Link is http://iwasbroke.savingadvice.com/2008/09/29/series-sell-car-with-negative-equity-par_43634/ Part 2 - Determine Your Car's Negative Equity

Text is Part 3 - Sell The Car With Negative Equity - Option A - Pay Off The Balance and Link is http://iwasbroke.savingadvice.com/2008/10/07/series-sell-car-with-negative-equity-par_43880/ Part 3 - Sell The Car With Negative Equity - Option A - Pay ...

Text is Part 4 - Sell The Car With Negative Equity - Option B - Transfer The Negative Equity Balance and Link is http://iwasbroke.savingadvice.com/2008/10/08/series-sell-car-with-negative-equity-par_43936/ Part 4 - Sell The Car With Negative Equity - Option B - Tran...

Part 5 - Benefits Of Selling A Car With Negative Equity

Lower Debt!

This is obvious, but it is a wonderful benefit of eliminating the car with negative equity. In the example used in this series, debt has been reduced by $18,000 in Option A or $12,000 in Option B. Either one is fantastic!

Money Freed Up Every Month!

This is also obvious, but the monthly payment will be eliminated or vastly reduced. This allows one to have more margin in their monthly finances to give, save, or invest (three of my favorite parts of money!).

Not so obvious is the reduction in other fringe expenses. Car insurance will go down. Car property taxes will go down. Gasoline consumption will go down. Car repair costs will go down. These can total up to hundreds of dollars in savings each month!

Margin

When all of the money leaves as soon as it is earned and one is living paycheck-to-paycheck with zero margin for life to happen, it creates serious stress. By eliminating debt and its related payments, one gains tons of financial freedom and drops loads of stress.

Final Note: I know that this stuff is HARD, but I am convinced that financial freedom is worth all of the effort that it takes. When Jenn and I embarked on our debt freedom march, it seemed like it would take forever. Fourteen months later, we were debt free. That was in February 2004. We have never looked back. No car, TV, boat, lawn mower, or Llama has looked good enough for payments. Frankly, a new house does not even look good enough for house payments. We have worked way too hard to achieve financial freedom to fall back into the debt trap. It has been SO WORTH IT! You can read more of my family's story Text is HERE and Link is http://www.josephsangl.com/iwasbroke/read-the-introduction HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

October 9th, 2008 at 12:29 am

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Text is Part 1 - Recognize How Much A Car Really Costs and Link is http://iwasbroke.savingadvice.com/2008/09/25/series-sell-car-with-negative-equity-par_43517/ Part 1 - Recognize How Much A Car Really Costs

Text is Part 2 - Determine Your Car's Negative Equity and Link is http://iwasbroke.savingadvice.com/2008/09/29/series-sell-car-with-negative-equity-par_43634/ Part 2 - Determine Your Car's Negative Equity

Text is Part 3 - Sell The Car With Negative Equity - Option A - Pay Off The Balance and Link is http://iwasbroke.savingadvice.com/2008/10/07/series-sell-car-with-negative-equity-par_43880/ Part 3 - Sell The Car With Negative Equity - Option A - Pay ...

Part 4 - Sell The Car With Negative Equity - Option B - Transfer The Negative Equity Balance

In this series, we are assuming that we have a car with an actual value of $12,000 but the loan balance is $18,000. This means that the car has negative equity of $6,000.

This is quite the lovely situation, but it is possible to make the car leave.

Obtain A Signature Loan From The Bank or Credit Union

One usually must have decent credit to obtain a signature loan. Obtain a $6,000 loan from the bank. Next, find a purchaser who is willing to pay $12,000 for the vehicle. Use the signature loan money to pay off the negative equity portion so that the title is clear. With this one transaction, the debt has been reduced by 66% - from $18,000 to $6,000!

Transfer The Negative Equity Balance To A 0% Credit Card

I really do not like credit cards, but I really do not like huge car payments and car loans either! If one has the option to roll the negative equity to a credit card at 0%, it will allow the car to be sold and all of the subsequent payments on the remaining $6,000 will go directly to principal! I have also seen several credit cards that offer 2.99% for the life of a balance transfer. You can find some 0% credit cards Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com/0-credit-cards/ HERE.

Option B does not entirely eliminate the debt or the payment, but it will substantially reduce it! It will certainly help one's journey to financial freedom obtain serious traction.

In the final part of this series, I will be sharing some side benefits to eliminating a car with negative equity.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

October 7th, 2008 at 02:12 pm

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Text is Part 1 - Recognize How Much A Car Really Costs and Link is http://iwasbroke.savingadvice.com/2008/09/25/series-sell-car-with-negative-equity-par_43517/ Part 1 - Recognize How Much A Car Really Costs

Text is Part 2 - Determine Your Car's Negative Equity and Link is http://iwasbroke.savingadvice.com/2008/09/29/series-sell-car-with-negative-equity-par_43634/ Part 2 - Determine Your Car's Negative Equity

Part 3 - Sell The Car With Negative Equity - Option A - Pay Off The Balance

Let's assume that a car has an actual value of $12,000 but the loan balance is $18,000. This means that the car has negative equity of $6,000.

This is quite the lovely situation, but it is possible to make the car leave.

Use Savings

If one wants to sell the car, then the negative equity must be covered in order to provide a clear title to the purchaser. The fastest way to clear out the negative equity is to find a purchaser who is willing to pay $12,000 for the car and use $6,000 from savings to clear up the negative equity. This is by far the fastest and easiest way to clear up the negative equity situation - IF you have $6,000 in savings!

Earn the Difference

If one does not have the money to cover the negative equity, then another way to accomplish the exact same thing is to earn additional income. Work overtime or acquire a second job to earn enough to cover the negative equity.

This is definitely not a fun answer, but I do not like negative equity situations either. The tough part about this option is the fact that it takes additional time and it is possible that the negative equity will increase because the car will continue to go down in value.

Sell Something Else

If one has an item that they no longer need, want, or use that has value, it can be sold to cover some of the negative equity.

I prefer Option A the most because it eliminates the entire debt and frees up the entire car payment to use for additional debt pay-off, savings, giving, and investing.

In the next part of this series, we will continue to discuss ways to sell the car even with negative equity.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

1 Comments »

September 29th, 2008 at 08:00 pm

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Text is Part 1 - Recognize How Much A Car Really Costs and Link is http://iwasbroke.savingadvice.com/2008/09/25/series-sell-car-with-negative-equity-par_43517/ Part 1 - Recognize How Much A Car Really Costs

Part 2 - Determine Your Car's Negative Equity

Equity is determined by the following equation:

Vehicle Actual Value - Vehicle Loan Balance = Equity

If the Equity number is negative, then that means that the vehicle has negative equity.

As you prepare to sell your car, it is very important to know the actual value of the car and the actual amount owed.

I emphasize the word ACTUAL because most people tend to overestimate their car's value and underestimate what they still owe.

How does one determine how much their car is actually worth? Obtain a quote from Text is Kelley Blue Book and Link is http://www.kbb.com/ Kelley Blue Book and Text is Edmunds and Link is http://www.edmunds.com/ Edmunds. You will need to know the year and make of your vehicle including your engine type and mileage. These two sites will provide you a general idea of what used cars like yours are selling for in your area. Recognize that these are average selling prices. That means that cars are selling above and below that number, but this is the price that one can expect to sell the vehicle.

Now that you know the actual value of the vehicle, it is time to determine exactly what is owed. Contact your lender and obtain the actual pay-off balance of the car loan.

Now, use the equity calculation to determine your vehicle's equity. If it is negative, then you have a car that is known as "upside down". It has negative equity. You owe more than it is worth.

In the next part of this series, we will discuss ways to sell the car even with negative equity.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

September 25th, 2008 at 02:54 pm

Welcome to the latest series - "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Part 1 - Recognize How Much A Car Really Costs

Some of the actions in this series might be difficult to execute, but when one recognizes how much a car really costs it can really help solidify sound financial decisions.

I believe that having a car payment is a HUGE financial mistake. Here is why.

First, cars drop in value. New cars drop in value FAST. Most new cars drop in value by around sixty percent in the first four years. This is called depreciation, and it causes one's net worth to drop.

Second, car payments reduce one's ability to gain financial freedom. Loan interest can range from 0% to 20% or higher depending upon one's credit. Even 0% loans are negative financial events because the money is going toward a car that is dropping in value. What else could one do with a monthly car payment? Give more? Invest more? Spend more?

When I recognized how much my debt was costing me, it solidified my commitment to achieving financial freedom. I was so dad-blamed sick of debt and what it was doing to my family.

Read the entire "Sell Car With Negative Equity" series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-sell-car-with-negative-equity/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Sell Car With Negative Equity

|

0 Comments »

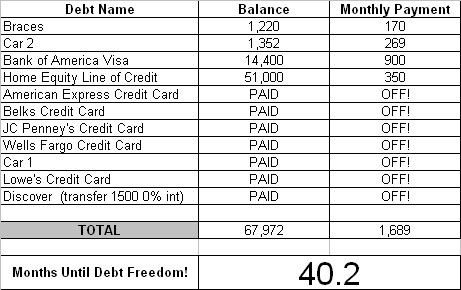

September 22nd, 2008 at 12:34 pm

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

Good things this month

We transferred JC Penney balance which was 21.99% to a 2.9% on Discover AND we transferred Chase that was 26% to a Juniper Mastercard at 7.9%. We were VERY excited about those transfers.

It is also very encouraging to see the balance on the National City card come down!! It won't be long until that one is GONE!

Challenges this month

Challenges this month have been the rising cost of gas and food, but we have just budgeted a little differently in some areas and made it work out fine! Again, this month I have to say THANK GOODNESS for the budget form!!! We were able to pay cash for all back to school items this year and MAN! Does that ever feel good!!!

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

It is so nice to see Couple #3 reap the rewards of the hard work they put forth to Text is restructure their debt and Link is http://iwasbroke.savingadvice.com/series-restructuring-debt/ restructure their debt. Look at the tremendous progress they are making. Instead of twenty percent of their payments going toward principal and eighty percent to banks, they have switched it around. Now, over 80% of all of their payments are going toward principal reduction! AWESOME!

Readers

If you have debt, have you considered restructuring it? This can really help your debt freedom march gain a ton of traction and speed up your journey to ZERO DEBT! I encourage you to read the series of posts I wrote called Restructuring Debt.

My book, Text is I Was Broke. Now I'm Not and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not, is available via AMAZON.COM, BORDERS.COM, and PAYPAL. You can read the Introduction Text is HERE and Link is http://www.josephsangl.com/iwasbroke/ HERE. In this book, you will learn exactly how Jenn and I became debt-free in just fourteen months.

Posted in

SERIES: Debt Freedom March - Couple #3

|

0 Comments »

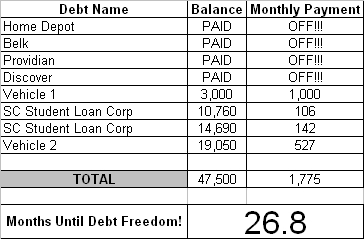

September 18th, 2008 at 01:31 pm

Introduction

This couple is THROUGH with debt! They announced that they were breaking up with debt in October 2007. They have agreed to share their Debt Freedom March with everyone in the hopes of inspiring others to do the same!

Here is this month's update.

We didn't put $1000 on Vehicle 1 last month which is why it only went from $3500 to $3000. We used that money for a few other things we wanted to do.

Everything is going GREAT!!!! We are still sticking to our cash envelopes and are looking forward to paying off Vehicle 1 soon!

Here is their updated Text is Debt Freedom Date and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation

Month By Month Progress

Sangl Says

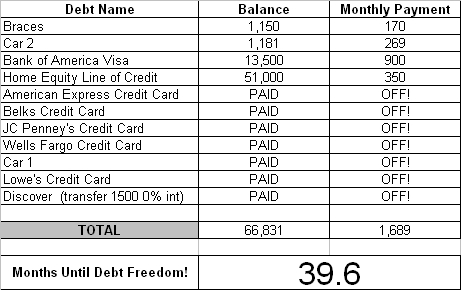

This is the one year anniversary of Couple #2's Debt Freedom March and look at how much debt they have paid off! They started out in the $70,000 range and are now in the $40,000 range. They have paid off $24,410 in ONE YEAR!

I am so excited for Couple #2. They are being blessed financially and instead of running out and blowing all of it, they are using it as an opportunity to completely change their entire financial future!

Readers

Couple #2 is on a roll. You can do the exact same thing! Pull up the Text is Debt Freedom Date Calculator (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=4 Debt Freedom Date Calculator (Excel) and put together your own Debt Freedom Date!

If not now, when?

My wife and I became debt-free (except for the house) in just fourteen months, and I share exactly how we did it in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

Text is Read Previous Updates For Couple #2 and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-2/ Read Previous Updates For Couple #2

Posted in

SERIES: Debt Freedom March - Couple #2

|

0 Comments »

September 17th, 2008 at 12:58 pm

I read Text is THIS ARTICLE and Link is http://money.cnn.com/2008/09/09/news/economy/cbo_budget_update/index.htm?cnn=yes THIS ARTICLE recently on CNN.com.

I am reminded yet again of why I am on this crusade.

In the United States, we are being taxed at the highest levels ever YET the government (people that WE elect) are spending it even faster.

Guess what? Whether you are dealing with four dollars, four million dollars, or four trillion dollars the fact remains that INCOME - OUTGO = EXACTLY ZERO.

Why don't we have a balanced budget that also has debt reduction in it?

I thought about this question for a few minutes, and here are some reasons I believe we do not have a balanced budget.

* It is hard to tell ourselves "No."

* It is even harder to tell others "No." Especially people we care about.

* There are a lot of good causes out there, and we want to fund all of them.

* Elected officials who cut spending for their district run a high risk of being run out of office.

* The "I'm going to put America on a budget." campaign speech is about as appealing as the spouse who announces "We're going on a budget." Instead of thinking "financial freedom" (that's what I think of when I hear the word "budget"), most people think "NO!", "No Fun!", and "Boring" and believe that it will be incredibly restricting, constricting, and beans & rice all of the time.

* Many people do not typically think toward the future. It takes time, effort, and organization to think about the future implications of such financial management. Many Americans are hugely short of time, effort, and organization.

What are you thoughts?

Posted in

Uncategorized

|

3 Comments »

September 16th, 2008 at 06:17 pm

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now ELEVEN months into their Debt Freedom March.

Good/Bad This Month

This month went to plan. It is great to see these balances going down. On the other hand, it is difficult for expenses to go up so much. It seems as though all of our extra spending money is going in the tank and into the grocery cart, but I can't complain. I feel very lucky. We have a house that is not in foreclosure, and we have two great jobs with benefits and insurance. We are so blessed.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Couple #1 is now twelve months into their debt freedom march. What a fantastic year it has been! They have paid off $21,801. This is what can happen when one is intensely focused on debt freedom and recognizes what life will be like when there is ZERO DEBT.

When Couple #1 started out, they had $35,695 in non-house debt. They now have only $16,000 of non-house debt remaining. Outstanding!

Couple #1 is doing a great job of sticking to their debt freedom march. There are times that it seems almost unattainable, but it IS attainable and it IS so worth it!

Readers …

How is your own Debt Freedom March progressing?

In I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction Text is HERE and Link is http://josephsangl.com/iwasbroke/ HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

|