|

|

|

|

You are viewing: Main Page

|

|

April 9th, 2010 at 08:49 pm

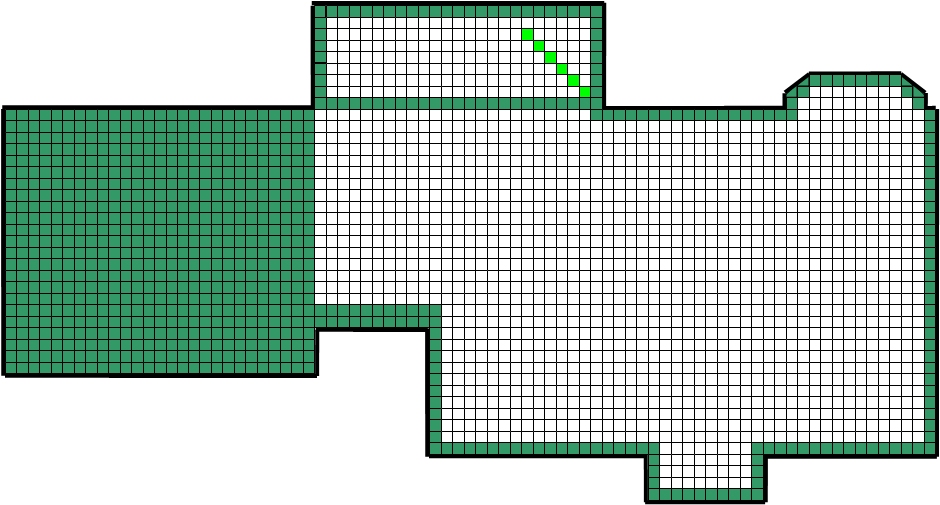

Every month there will be an update of Joe & Jenn�s Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 836 IS 842

Squares Remaining: WAS 1590 IS 1584

% of House Owned By The Sangl's: WAS 34.5% IS 34.7%

% of House Owned By Wells Fargo: WAS 65.5% IS 65.3%

Here is the updated "Sangl Home Pay-Off Spectacular"

We were able to color in six squares this month. We are still working through all of the hospital bills from our son's arrival and rebuilding the emergency fund. This stuff takes patience, but the plans of the diligent lead to profit as surely as haste leads to poverty. I am committed to diligently crushing the mortgage (I submit as evidence the fact that I have been posting our progress since October 2007).

How are you doing on YOUR house payoff spectacular? If you do not have one, you can get one here => Text is Pay Off Spectacular - House and Link is http://nextsteps.iwasbrokenowimnot.com/tools/pay-off-spectaculars/ Pay Off Spectacular - House.

Read previous Text is Sangl Home Pay-Off Spectacular Updates and Link is http://iwasbroke.savingadvice.com/series-home-pay-off-spectacular/ Sangl Home Pay-Off Spectacular Updates

Posted in

SERIES: Home Pay-Off Spectacular

|

1 Comments »

March 7th, 2010 at 10:45 pm

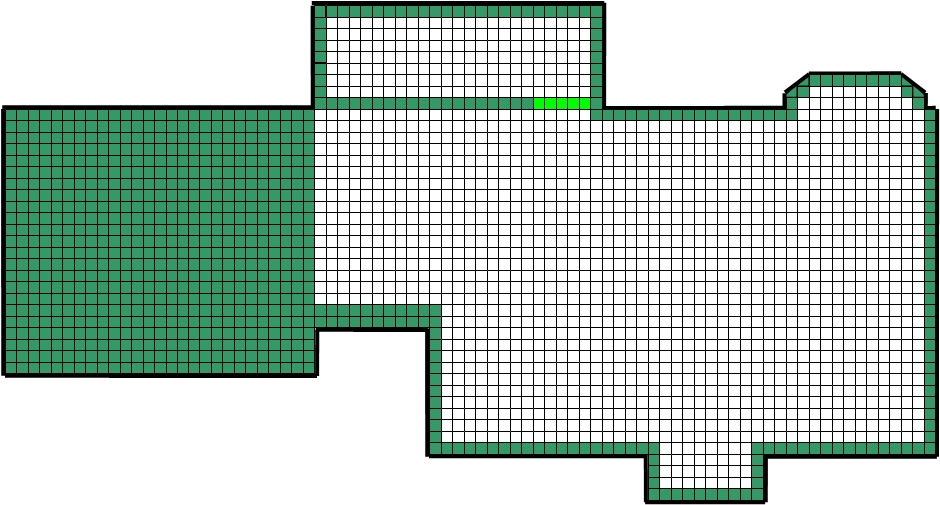

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: 831 836

Squares Remaining: 1595 1590

% of House Owned By The Sangl's: 34.3% 34.5%

% of House Owned By Wells Fargo: 65.7% 65.5%

Here is the updated "Sangl Home Pay-Off Spectacular"

Baby Sangl (Keaton) has finally arrived and now we are awaiting the final hospital bills. Once those are paid off, we will replenish the emergency funds and then re-attack this mortgage with renewed vigor. We are praying to be able to CRUSH this mortgage in short order. Will you pray this for us?

We now also own the perimeter of our sunroom. The next time around the sunroom will not take as long. We can't wait to say we completely own this room as it is one of our favorite rooms of the house.

How are you doing on YOUR house payoff spectacular? If you do not have one, you can get one here => Text is Pay Off Spectacular - House. and Link is http://nextsteps.iwasbrokenowimnot.com/tools/pay-off-spectaculars/ Pay Off Spectacular - House.

Read previous Text is Sangl Home Pay-Off Spectacular Updates and Link is http://iwasbroke.savingadvice.com/series-home-pay-off-spectacular/ Sangl Home Pay-Off Spectacular Updates

Posted in

SERIES: Home Pay-Off Spectacular

|

5 Comments »

December 23rd, 2009 at 01:23 pm

I am EXCITED and PUMPED about my new book for high school students, college students, and twenty-somethings - What Everyone Should Know About Money Before They Enter THE REAL WORLD.

To celebrate the release of this book, I am sharing one of the chapters of this book (see all of the chapter titles Text is HERE and Link is http://www.josephsangl.com/whateveryoneshouldknowaboutmoney/table-of-contents/ HERE)

Here is another section of the "Credit Scores" chapter:

========================================================

Everyone Should Know ...

The key measurements that determine a credit score.

The credit reporting agencies are secretive as to how they calculate credit scores, but it is well known that credit scores are directly impacted by the following items:

Type of credit issued

- Revolving debt (credit card)

- Installment debt (anything with payments and a pay-off - car loan, boat loan, student loan, etc.)

Age of the credit relationship

Amount of credit one can obtain (total of all credit limits)

Amount of credit one has consumed (percentage of total credit limit)

Payment timeliness

Requests for credit

Outstanding judgments

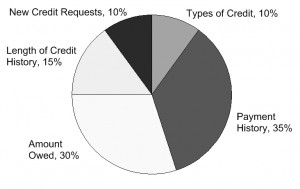

According to FICO's publication, Understanding Your FICO Score, a FICO credit score is determined in the following way for the general population.

FICO scoring breakdown [from FICO's publication, Understanding Your Credit Score]

For people who are just establishing credit, it will be different since payment history is not yet available.

========================================================

More from this chapter tomorrow!

Read the entire series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-high-school-money-book/ HERE

Learn more about the book and PURCHASE YOUR COPY (released 12/15!) at its dedicated website Text is HERE and Link is http://www.josephsangl.com/whateveryoneshouldknowaboutmoney/ HERE

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: High School Money Book

|

0 Comments »

December 8th, 2009 at 01:08 pm

I am EXCITED and PUMPED about my new book for high school students, college students, and twenty-somethings - Text is What Everyone Should Know About Money Before They Enter THE REAL WORLD. and Link is http://www.josephsangl.com/whateveryoneshouldknowaboutmoney What Everyone Should Know About Money Before They Enter THE ...

This book has been in the works for over a year. Over that time, I sought out feedback from YOU, from people I have taught, and from my own experience.

My primary question for students was: "What confuses/scares/intimidates you most about money?"

My primary question for "older" people was: "What do you wish you had known about money before you entered the real world?"

The feedback was amazing, and I am SO EXCITED to have this resource to help us in our crusade to help others accomplish far more than they ever thought possible with their personal finances.

With that introduction, I want to share a portion of one of the chapters with you. It is about "Credit Scores".

========================================================

Everyone Should Know ...

Your credit score will have an impact on your life.

Credit scores are a measure of one's ability to manage debt. The dominant credit scoring system which is used by most lenders was created by Fair Isaac. This system provides a measure of an individual's credit worthiness and is commonly known as a FICO Score.

A credit score impacts many things. It determines whether or not you can obtain a loan. If you qualify for a loan, the credit score dictates the interest rate charged.

Credit scores also impact insurability. When you obtain auto, renter's or homeowner's insurance, the credit score directly impacts the insurance cost. The lower your credit score, the higher the insurance premium will cost. I have seen insurance premiums doubled because of poor credit.

Credit scores also impact the ability to obtain a cell phone contract or an apartment lease. It can affect utility connections. Utility providers usually require much larger deposits from people who have low credit scores. If you have an excellent credit score, a deposit might be waived entirely. Credit scores can even impact your ability to obtain a job.

========================================================

More from this chapter tomorrow!

Read the entire series Text is HERE and Link is http://iwasbroke.savingadvice.com/series-high-school-money-book/ HERE

Learn more about the book and RESERVE YOUR COPY (ships 12/15!) at its dedicated website Text is HERE and Link is http://www.josephsangl.com/whateveryoneshouldknowaboutmoney HERE

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: High School Money Book

|

1 Comments »

December 7th, 2009 at 10:33 pm

After prompting from several of you, I am back to posting on SavingAdvice.com.

I am excited about what has gone on with this crusade to help others accomplish far more than they ever thought possible with their personal finances!

We have been able to teach nearly 50,000 in 2009 ALONE (that accounts for the silence on this blog!). I can't believe I get to do this stuff for a living!

My new book for high school students, college students, and 20-somethings called What Everyone Should Know About Money Before They Enter THE REAL WORLD will officially release on December 15th!

I wrote this book because I wanted to provide a resource to young people that will help them PREVENT financial mistakes because it is so much harder to CURE them later!!!

If you have a blog and would be willing to write a post about the book, I would be happy to send you a review copy. All you need to do is click Text is HERE and Link is http://www.josephsangl.com/about/ HERE and provide the following information:

- Your blog address

- A name and shipping address

- A commitment to write about the book

Thanks so much to everyone who has made this book possible!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: High School Money Book

|

2 Comments »

June 3rd, 2009 at 06:38 pm

I announced Text is HERE and Link is http://iwasbroke.savingadvice.com/2009/05/20/need-your-help-writing-a-high-school-mon_51159/ HERE that I am in the process of writing my next book. It will be a book that is addressed to high school students, and I am sharing 12 Things I Wish I Had Learned About Money Before I Hit The Real World.

That is not necessarily the title, and it might end up being 10 things or 15 things. All I know is that I want (and need) your help in writing this book!

For the next few days, I am going to ask you to take a couple minutes of your time and share some things you wish you would have learned about specific money topics.

Part Five Financial Decision-Making

Here is the question that I want to hear your thoughts on today:

What is the best financial decision you have ever made? What led to that decision? How would you teach young people to make that type of decision?

Share stories!

Text is Read entire series and Link is http://iwasbroke.savingadvice.com/series-high-school-money-book/ Read entire series

Posted in

SERIES: High School Money Book

|

2 Comments »

May 28th, 2009 at 12:30 pm

I announced Text is HERE and Link is http://iwasbroke.savingadvice.com/2009/05/20/need-your-help-writing-a-high-school-mon_51159/ HERE that I am in the process of writing my next book. It will be a book that is addressed to high school students, and I am sharing 12 Things I Wish I Had Learned About Money Before I Hit The Real World.

That is not necessarily the title, and it might end up being 10 things or 15 things. All I know is that I want (and need) your help in writing this book!

For the next few days, I am going to ask you to take a couple minutes of your time and share some things you wish you would have learned about specific money topics.

Part Four Financial Decision-Making

Here is the question that I want to hear your thoughts on today:

What is the worst financial decision you have ever made? What led to that decision? How would you teach young people to avoid that type of decision?

Share stories!

Text is Read entire series and Link is http://iwasbroke.savingadvice.com/series-high-school-money-book/ Read entire series

Posted in

SERIES: High School Money Book

|

2 Comments »

May 26th, 2009 at 09:16 pm

I announced Text is HERE and Link is http://iwasbroke.savingadvice.com/2009/05/20/need-your-help-writing-a-high-school-mon_51159/ HERE that I am in the process of writing my next book. It will be a book that is addressed to high school students, and I am sharing 12 Things I Wish I Had Learned About Money Before I Hit The Real World.

That is not necessarily the title, and it might end up being 10 things or 15 things. All I know is that I want (and need) your help in writing this book!

For the next few days, I am going to ask you to take a couple minutes of your time and share some things you wish you would have learned about specific money topics.

Part Three Debt

Here is the question that I want to hear your thoughts on today:

What were the first debts you ever obtained, and how did they impact your financial situation?

Share stories!

Text is Read entire series and Link is http://iwasbroke.savingadvice.com/series-high-school-money-book/ Read entire series

Posted in

SERIES: High School Money Book

|

2 Comments »

May 22nd, 2009 at 03:51 pm

I announced Text is HERE and Link is http://iwasbroke.savingadvice.com/2009/05/20/need-your-help-writing-a-high-school-mon_51159/ HERE that I am in the process of writing my next book. It will be a book that is addressed to high school students, and I am sharing 12 Things I Wish I Had Learned About Money Before I Hit The Real World.

That is not necessarily the title, and it might end up being 10 things or 15 things. All I know is that I want (and need) your help in writing this book!

For the next few days, I am going to ask you to take a couple minutes of your time and share some things you wish you would have learned about specific money topics.

Part Two Impulsiveness

Here is the question that I want to hear your thoughts on today:

How have impulsive financial decisions impacted your overall financial situation? Share stories!

Posted in

SERIES: High School Money Book

|

1 Comments »

May 21st, 2009 at 08:45 pm

I announced Text is HERE and Link is http://iwasbroke.savingadvice.com/2009/05/20/need-your-help-writing-a-high-school-mon_51159/ HERE that I am in the process of writing my next book. It will be a book that is addressed to high school students, and I am sharing 12 Things I Wish I Had Learned About Money Before I Hit The Real World.

That is not necessarily the title, and it might end up being 10 things or 15 things. All I know is that I want (and need) your help in writing this book!

For the next few days, I am going to ask you to take a couple minutes of your time and share some things you wish you would have learned about specific money topics.

Planning Your Spending

Here is the question that I want to hear your thoughts on today:

What do you wish you would have known about planning your spending by the time you graduated high school?

Share your stories in the comment section!

Posted in

SERIES: High School Money Book

|

5 Comments »

May 20th, 2009 at 01:24 pm

I do not know what the title will be yet, but it will be something like:

12 Things I Wish I Had Learned About Money Before I Hit The Real World

It is our passion to help others accomplish far more than they ever thought possible with their personal finances. In Text is I Was Broke. Now I'm Not. and Link is http://nextsteps.iwasbrokenowimnot.com/all-iwbnin-resources/ I Was Broke. Now I'm Not. (and its related Text is Group Study and Link is http://groupstudy.iwasbrokenowimnot.com Group Study), I told my story of walking out of financial disarray, and I teach the tools we used to become debt-free. It is mostly focused on providing a CURE for an existing negative financial situation.

In this new resource, we are focusing on PREVENTION of negative financial situations. I know that I went through twenty years of formal education (13 years of K-12, 4 years of undergrad, 3 years of grad) and I had exactly zero classes on personal finances. It is my hope that we can provide a resource that can be utilized in schools and in churches to teach high school students how to manage their financial resources well.

I need your stories! For the next five days, I will be asking a series of questions about what you think teenagers need to know about money before they hit the real world.

Posted in

SERIES: High School Money Book

|

0 Comments »

March 2nd, 2009 at 06:23 pm

I have met a ton of people who are experiencing the harshness of the following two key items:

* No Plan, No Savings, Piles of Debt

* Loss/Reduction of Income

Here is what you can do when faced with this situation.

1. Cry. It is OK to be regretful for awhile!

2. Take time to prioritize who will get paid and who will not get paid. (Read the post I wrote Text is HERE and Link is http://iwasbroke.savingadvice.com/2008/11/18/help-i-cant-pay-my-bills-part-3_45239/ HERE about priority order.)

3. Write out your goals. Make sure they are SMART.

4. Prepare a written spending plan (even if you know that it will not balance to Exactly Zero). This will allow you to fully understand your "Go Get This!" number.

5. Take ACTION!

There can be a tendency to just focus on #1 and hope for everything to just work itself out. Usually, this is not the case. Recovering from this type of issue is emotional and gut-wrenching, but it requires one to take action.

You CAN recover from the mess!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

March 1st, 2009 at 11:40 pm

I heard several times that Crocs were great shoes. I finally heard it enough that I bought a pair. They are great! So great that I wear them everywhere. Including to Iowa in January in snow. When I finally tried out a pair, I thought, "Why didn't I listen and take action earlier?"

I heard several times that iPods were incredible. I finally heard it enough that I bought one. It is incredible! So great that I wear it while running, driving, and sitting on an airplane. When I finally tried out a pair, I thought, "Why didn't I listen and take action earlier?"

"Why didn't I listen and take action earlier?" This is a question I have asked myself many times after discovering a new thing that enhanced my life greatly.

It applies to my finances. When I first prepared a Text is written spending plan and Link is http://nextsteps.iwasbrokenowimnot.com/tools/budgeting-tools/ written spending plan before the month and the money arrived, I asked myself this key question.

I wonder how many more things I should be listening to and taking action earlier?

I challenge you to ask yourself the same question.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

February 16th, 2009 at 03:54 pm

"How do I build my credit?"

This is one of the most common questions I am asked. In this series, I will be sharing various ways that one can build credit while still winning with money.

Part Four - Understand Why Credit Scores Are Necessary

What is the number one reason why someone would want a great credit score?

To obtain more debt!

Think about it! I am not a fan of debt at all. It robs people of peace and places tremendous strain on relationships.

What exactly is debt anyway?

Debt is nothing more than pledging tomorrow's income to someone else.

If one has zero debt, then they will have no credit score. They could have $10,000,000 in the bank, but have a zero credit score.

A credit score does have an impact on other areas of life, however. It can affect insurance premiums, deposits required for utility hook-ups, and approval to rent real estate. It can also impact one's ability to be hired! Military personnel have been denied or lost security clearances due to their credit.

So Text is read the entire series and Link is http://iwasbroke.savingadvice.com/series-how-do-i-build-my-credit/ read the entire series, work on building a decent credit score, and do it all with a written spending plan!

Posted in

SERIES: How Do I Build My Credit?

|

0 Comments »

February 15th, 2009 at 03:04 pm

"How do I build my credit?"

This is one of the most common questions I am asked. In this series, I will be sharing various ways that one can build credit while still winning with money.

Part Three - Pay All Bills On Time - Consider Automatic Bill-Pay

If you do not pay your bills on time, the late payments will be reported to the credit reporting agencies.

This means that you need to pay your utility, cell phone, and other monthly bills on time. This is why I am such a huge fan of a written monthly spending plan (budget). When you have a plan, the chances of paying a bill late are greatly reduced.

If you live an exceptionally busy life or are notorious for procrastination, consider automating bill payments. This will ensure that bills are paid on time, and can greatly reduce stress and the potential for your credit score to be dinged.

Text is Read the entire series and Link is http://iwasbroke.savingadvice.com/series-how-do-i-build-my-credit/ Read the entire series

Posted in

SERIES: How Do I Build My Credit?

|

0 Comments »

February 6th, 2009 at 02:39 pm

"How do I build my credit?"

This is one of the most common questions I am asked. In this series, I will be sharing various ways that one can build credit while still winning with money.

Part Two - Swipe Purchase And Immediately Pay Off

A great way to boost one's credit score is to obtain a department store credit card. Here is how it works.

1. Ensure that a small purchase from that store (something you truly need) is included in your monthly budget.

2. Pull the money planned for that purchase out in cash and head to the store.

3. Purchase the item with the department store credit card.

4. Immediately after being given the receipt, tell the cashier that you want to make a payment on your credit account and give them the cash for the purchase to bring your credit account balance to EXACTLY ZERO.

5. Do this once each month.

Your credit score will soar as the length of the credit relationship increases and as the balance remains at zero. It might be helpful to go back to Part One to see what comprises of your credit score.

NOTE: If you do not trust yourself with a credit card and controlling your spending using a written monthly spending plan, then DO NOT use this method!

Text is Read the entire series and Link is http://iwasbroke.savingadvice.com/series-how-do-i-build-my-credit/ Read the entire series

Posted in

SERIES: How Do I Build My Credit?

|

0 Comments »

February 5th, 2009 at 03:16 pm

"How do I build my credit?"

This is one of the most common questions I am asked. In this series, I will be sharing various ways that one can build credit while still winning with money.

Part One - What Determines My Credit Score?

It is important to first understand how one's credit score is calculated. There are some key characteristics that are used by credit monitoring companies (Experian, Equifax, and TransUnion) to determine your credit score.

* Type of Credit There are two key types of credit. Installment (car payment, house payment) or Revolving (credit card, line of credit)

* Total Available Credit This is the total of all credit limits.

* Total Credit Utilized This is the total of all current debt.

* Length of Credit Relationship The longer the credit relationship, the better.

* Payment Timeliness Obviously, payments need to be paid on time to achieve the highest scores!

* Requests For Credit Made For Potential Purchases

* Public Records Bankruptcies and judgments are not helpful to one's credit score!

You can check out some of the related articles/links below to learn more about credit scores.

Related Articles/Links

* Text is Experian's "What's In A Credit Score?" and Link is http://www.experian.com/credit-scores/what-is-a-good-credit-score.html Experian's "What's In A Credit Score?"

* Text is TransUnion's "Credit Scoring 101" and Link is http://content.truecredit.com/sites/LearningCenter/creditScores/creditScoring101.page TransUnion's "Credit Scoring 101"

* Text is Equifax's "Keeping Score On Your Credit Score" and Link is http://learn.equifax.com/cs/Satellite?c=DS_General_Cont_C&childpagename=DecisionSimple%2FDS_General_Cont_C%2FDSGeneralContentTemplate&cid=1189578994233&pagename=DecisionSimple%2FPage%2FDSLayoutTemplate&ParentLinkID=1162919656130 Equifax's "Keeping Score On Your Credit Score"

Posted in

SERIES: How Do I Build My Credit?

|

0 Comments »

February 3rd, 2009 at 01:54 pm

I had the outstanding opportunity to go skiing on Friday before the Financial Learning Experience in Cheyenne, Wyoming.

I went skiing at Copper Mountain in Colorado, and it was INCREDIBLE! Over a foot of fresh snow over the past week had fallen, and the slopes were in terrific shape. It was the warmest day of the week (33 degrees) and sunshine too!

Here is a picture.

It was incredible, and I want to go back RIGHT NOW!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

February 2nd, 2009 at 09:42 pm

I recently spoke in Ottumwa, Iowa.

I was there to teach the Financial Learning Experience at Text is thebridge and Link is http://www.ottumwabridge.org/ thebridge church (pastor is Marty Schmidt).

I learned a lot about Ottumwa, Iowa.

* It is the hometown of Radar from M.A.S.H. and Tom Arnold

* It is about 1.5 hours south and east of Des Moines

* There is a huge need for financial training (just like all other areas of America!)

* I like Ottumwa

* It is home to a cool new church called "thebridge"

I also have realized that I have been living in the South for awhile. I showed up in Des Moines (8 degrees F and snow) wearing a light jacket, running socks, and Crocs.

Guess what? I was cold. Snow came in direct contact with my legs just above the ankles, and snow went right through the holes in the Crocs and soaked my socks.

So for those of you who were wondering: Crocs do not work well in snow.

It made me think about the number of times I have showed up ill-prepared to address financial issues. For example, I used to think that earning more money would solve my credit card balance and impulsive spending decisions. I was wrong. The fact was that I could earn millions of dollars a year, and I would still have an outgo problem.

I was ill-equipped. My monthly written spending plan using INCOME - OUTGO = EXACTLY ZERO was the correct tool to address my problem.

My Crocs have been replaced with nice leather waterproof shoes.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

2 Comments »

January 29th, 2009 at 08:49 pm

A person who recently attended a Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience e-mailed me the following question:

I had the privilege of hearing you speak both during the message and the class that followed. My wife and I are committed to eliminating our debt. With that in mind, I have a question. I have three credit cards one for 6,000.00, one for 1956.00 and one for 5775.00 I am paying high interest rates 27.98, 24.00 and 20.4% respectively.

I tried to reduce my rates, but they were unwilling and the reality is that I don't get [0%] offers in the mail anymore.

I responded with the following question: Have you applied for one of the cards on my "Next Steps" site [Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/0-credit-card-balance-transfers/ HERE]?

His response FIRED ME UP!

Here is his response.

I just applied for the discover card and I put two of the cards to be transferred totaling 11,500.00 and I was accepted! After talking to Bank of America earlier today I felt as if I were a heathen slug that had delinquent deadbeat written on my forehead and the reality was that I had always paid them!

Thank you. You will get my phone call with a loud yahoo! You have an awesome ministry keep up the good work.

So let's look at the math. $6,000 was moved from 27.98% and $5,500 was moved from 20.4%. That one move saved $205/month in INTEREST!!! That is over $2,400 per year in INTEREST that was eliminated.

If you are paying interest on a credit card, why?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

2 Comments »

January 20th, 2009 at 08:57 pm

I was able to achieve my goal of completing the marathon in under four hours!

I am PUMPED! More to follow in the next week on the similarities between finances and marathons.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

3 Comments »

January 12th, 2009 at 07:47 pm

Welcome to the latest series - "Helpful Real Estate Sites".

It is my hope that this series will equip you with new information that helps you make excellent real estate decisions!

It is my hope that this series will equip you with new information that helps you make excellent real estate decisions!

Part Three - CNNMoney.com's Real Estate Section

CNN has partnered with Money Magazine to provide helpful and very timely information about real estate - both on the macro level and the personal level.

Some specific reasons I like this site are:

* Timely Articles - Helps me keep up with national trends in real estate

* Calculators - I love all of CNNMoney's calculators - not just the real estate section. In the real estate section, you can find calculators for renovations, refinancing, cost of living comparisons, and shop for a mortgage. You can check out their calculators Text is HERE and Link is http://cgi.money.cnn.com/tools/index.html HERE.

* Real Estate Tips - Whenever you learn something new regarding real estate, it has the potential to save you thousands of dollars! I like saving money!

Those are some of the reasons that I love CNNMoney's Real Estate Section. Have you used this resource before?

Visit Text is CNNMoney's Real Estate Section and Link is http://money.cnn.com/real_estate/index.html CNNMoney's Real Estate Section

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Helpful Real Estate Sites

|

1 Comments »

January 7th, 2009 at 03:12 pm

Welcome to the latest series - "Helpful Real Estate Sites".

It is my hope that this series will equip you with new information that helps you make excellent real estate decisions!

Part Two - Zillow.com

This is another way to research homes that are for sale in your area.

I like the clean feel of Zillow.com, and its of use. Here are some additional reasons I like Zillow.com:

* Market Dynamics Just below the search bar, Zillow provides an up-to-date number of homes that are on the market in the entire US. I like seeing the macroeconomic view of the housing market.

* Days on Zillow A key measure in real estate is "Days on Market" or DOM. Zillow has created a similar measurement called "Days on Zillow". This information can be utilized to construct a better offer.

* Make Me Move Feature Zillow has a feature where you can list your house without actually listing it. Basically, you provide a price that you would be willing to sell your house for and if someone decides to purchase your home, the "make me move" happens. Interesting concept!

* Recently Sold Feature This feature allows you to see the houses in your search area that have sold most recently and the price at which they sold.

* Home Values Index You can see what homes are selling for you in your area by a number of measures - including $/SF, Selling Price, and flips.

Those are some of the reasons that I love Realtor.com. Have you used this resource before?

Visit Text is Zillow.com and Link is http://www.zillow.com Zillow.com

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Helpful Real Estate Sites

|

0 Comments »

January 6th, 2009 at 03:37 pm

Welcome to the latest series - "Helpful Real Estate Sites".

It is my hope that this series will equip you with new information that helps you make excellent real estate decisions!

Part One - Realtor.com

I have used Realtor.com to find each of the four houses that I have purchased.

This web site is an excellent way to understand market prices and to understand market availability.

Here are some specific reasons I love Realtor.com:

* Easy to search You are able to select the specific items you are interested in. For example, if you are interested in a three bedroom, two bathroom house with a garage, you can search for that. If you want to search for listings that include land, then you can select that also. Another key search criteria is square footage.

* Price range specific You can search for specific price ranges of houses within your set criteria. This really helps one understand what is available within that price range.

* Listings are mapped You can see all of the listings on a map. This is a great feature that allows you to understand the inventory available within the location you have selected.

* Pictures Many of the listings have photos of the exterior and interior. Instead of setting up a walkthrough, you can do so from your computer!

* Seamlessness Once you find some homes that you are interested in, you can select "Request a showing" from the actual listing. Awesome!

Those are some of the reasons that I love Realtor.com. Have you used this resource before?

Visit Text is Realtor.com and Link is http://www.realtor.com Realtor.com

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

SERIES: Helpful Real Estate Sites

|

1 Comments »

December 31st, 2008 at 02:34 pm

The Federal Reserve Board has implemented some substantial rule changes that govern how credit card companies interact with cardholders.

I am PUMPED about some of the rules changes, but I am disappointed that most of these will not be implemented until July 2010.

Here are some rule changes that I am excited about:

* Double cycle billing is eliminated. This eliminates double-billing on interest (robbery).

* Can't raise rates unless payments are more than 30 days behind. Provides some margin for error before default rates go into effect.

* Payments will be applied to highest interest balances first. YAY!

And here is my personal favorite - No more universal default rules! This means that credit card companies can not raise your rate on a card that has been paid on time simply because you have paid late on another credit card!

You can read a complete article about the credit card lending rules at CNNMoney - Text is HERE and Link is http://money.cnn.com/2008/12/18/pf/credit_card_rules/index.htm?postversion=2008121817 HERE.

As a reminder, there is a way to prevent credit card companies from controlling your life - PAY THEM OFF!!! If you are carrying a balance on your credit card and are paying interest, it can be very worthwhile to transfer the debt to Text is 0% balance transfer credit cards and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/0-credit-card-balance-transfers/ 0% balance transfer credit cards so that ALL of your payment is applied to principal. PAY THEM OFF, and apply the first rule of holes - stop digging! No more debt.

Posted in

Uncategorized

|

1 Comments »

December 17th, 2008 at 02:34 pm

Introduction

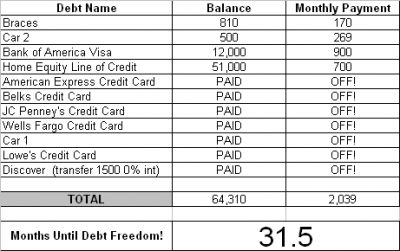

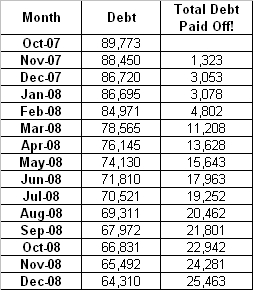

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now over a year into their Debt Freedom March.

Couple #1's Thoughts This Month

The current economic environment is flipping crazy. I can only think that God had his hand in my wife and I deciding to get out of debt long before this downturn.

* We paid half the balance of car 2 and owe just $500.

* We increased the payment on the HELOC to $700.

* The property taxes are already paid when in years past I would have to wait until my tax check came back.

* Christmas is bought and paid for and under the tree. Instead of buying useless presents for friends this year, I made gifts out in my shop.

We have a lot to be thankful for. We have our jobs, we have our health, and we have each other. May God bless you all as I have been blessed. Merry Christmas!

Updated Debt Freedom Date

Month By Month Progress

Sangl says

Another excellent month! Couple #1 has a fully-functioning Known, Upcoming Expenses account that has enabled them to stay the course even in difficult economic times. If your budget is constantly smashed by things like property taxes, quarterly insurance premiums, vacation, or Christmas, I highly recommend clicking Text is HERE and Link is http://www.josephsangl.com/2008/11/26/known-upcoming-expenses/ HERE to learn how to set up a Known, Upcoming Expenses account.

Read Previous Monthly Updates For Couple #1 Text is HERE and Link is http://iwasbroke.savingadvice.com/series-debt-freedom-march-couple-1/ HERE

Posted in

SERIES: Debt Freedom March - Couple #1

|

0 Comments »

December 10th, 2008 at 03:50 pm

I love giving. Love it!

I have seen the the simple act of giving completely transform lives. My education is a direct result of GIFTS.

Purdue University

* My beloved university where I received my bachelor's degree in Mechanical Engineering (BSME) was founded through gifts.

* In 1862, President Lincoln signed the Morrill Land Grant Act that would give public owned land to any state that would use the land or proceeds from the sale of that land to found a college teaching agriculture and engineering.

* In 1869, Indiana signed on and accepted GIFT from John Purdue ($150,000 - in 1869! At 4% annual inflation, that equates to a gift of $38,614,733!). They also accepted a GIFT of $50,000 from Tippecanoe County (where Purdue is located) and 100 acres from local residents.

Clemson University

* The university where I received my masters degree in Business Administration (MBA) was founded through the same Morrill Land Grant Act!

* In Thomas Green Clemson's will, he bequeathed the Fort Hill plantation and a considerable sum from his personal assets for the establishment of an educational institution of the kind he envisioned.

Giving made my education a possibility. John Purdue, the residents of Tippecanoe County, and the local residents who donated land all made Purdue a possibility. Thomas Green Clemson made Clemson a possibility. Although the residents of Tippecanoe County who donated tax dollars and land are not mentioned, they are just as much a part of it as John Purdue and Thomas Clemson.

Key Lesson: GIVING allows me to make a difference in future generations.

Sources

* Purdue University web site

* Clemson University web site

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

December 9th, 2008 at 06:11 pm

I love filling in the squares on the Sangl Family Home Pay-Off Spectacular every month. It is so satisfying to visibly watch the debt leave.

Over the past year, we have developed an entire set of Text is Debt Pay-Off and Link is http://nextsteps.iwasbrokenowimnot.com/tools/pay-off-spectaculars/ Debt Pay-Off and Text is Saving Spectaculars and Link is http://nextsteps.iwasbrokenowimnot.com/tools/saving-spectaculars/ Saving Spectaculars. In fact, they have been downloaded thousands of times! That floors me.

I would love to hear your ideas on additional Spectaculars we can provide.

So … ask yourself the following questions:

What are you paying off? and What are you saving money for?

Put your suggestions in the comments below, and the team will work to provide spectaculars for them over the next several weeks!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

December 8th, 2008 at 01:57 pm

Marathon training is like planning.

I am currently training for a full marathon that I will run on January 18 in Houston, TX. I am neck deep in to the training plan right now, and there have been several times that I have asked myself, "WHY am I doing this? AGAIN?!!"

Since this is my second marathon, I am much more aware of the importance of good planning.

In my first marathon, I had a great training plan that I obtained from Text is HalHigdon.com and Link is http://www.halhigdon.com/ HalHigdon.com. He has training plans for all lengths and types of runs, but I pulled up the novice marathon training plan.

It was a great plan. It started out with moderate runs and slowly but surely it stretched out to longer runs. I remember specifically a day that the plan called for a twenty mile run. A twenty mile run. I was training in Indiana for the race, and it was horribly cold outside so I ran on a treadmill.

Shortly after I got on the treadmill, a young mother showed up and placed her baby in a car seat attachment next to her. She then proceeded to change the TV to "Bob The Builder". She ran for twenty minutes and then left me stranded there watching "Bob The Builder" - SIX STRAIGHT EPISODES!

After running for seventeen miles, I could not take "Bob The Builder" anymore so I got off the treadmill to go change the TV channel. I never got back on the treadmill. I never ran the other three assigned miles.

I ended up shortchanging one more twenty mile run that was on the plan.

Guess what happened? During the marathon, I ran great until mile 17. By mile 19, I was hurting so bad that I stopped and walked for awhile. I ran-walked the final 7.2 miles. I finished, but I really paid dearly for not following the plan.

Have you ever planned your spending and then failed to follow it? I know I have in the past. I made it through the month, but I paid dearly for not following the plan.

That is how marathon training is like … plannning.

Will Rogers said that "even if you are on the right track, you will get run over if you just sit there."

Text is Read Recent Posts and Link is http://iwasbroke.savingadvice.com Read Recent Posts

Posted in

Uncategorized

|

2 Comments »

December 4th, 2008 at 10:06 pm

I believe that the greatest economic stimulus package that could have ever been implemented is LOWER GAS PRICES.

Seriously. I believe that super-high gas prices forced people to trim their spending to essentials and to restructure their spending - including eliminating gas hogs. Now that gas prices have eased there is extra money each month.

I do not know about you, but I saw a ton of people at Wal-Mart on Black Friday shopping with cash.

The average American family is getting an extra $50 to $200/month simply because of lower gas prices. That equates to an extra $600 to $2,400/year.

What do you think?

Posted in

Uncategorized

|

4 Comments »

|