|

|

|

|

Home > Category: Uncategorized

|

|

Viewing the 'Uncategorized' Category

March 2nd, 2009 at 06:23 pm

I have met a ton of people who are experiencing the harshness of the following two key items:

* No Plan, No Savings, Piles of Debt

* Loss/Reduction of Income

Here is what you can do when faced with this situation.

1. Cry. It is OK to be regretful for awhile!

2. Take time to prioritize who will get paid and who will not get paid. (Read the post I wrote Text is HERE and Link is http://iwasbroke.savingadvice.com/2008/11/18/help-i-cant-pay-my-bills-part-3_45239/ HERE about priority order.)

3. Write out your goals. Make sure they are SMART.

4. Prepare a written spending plan (even if you know that it will not balance to Exactly Zero). This will allow you to fully understand your "Go Get This!" number.

5. Take ACTION!

There can be a tendency to just focus on #1 and hope for everything to just work itself out. Usually, this is not the case. Recovering from this type of issue is emotional and gut-wrenching, but it requires one to take action.

You CAN recover from the mess!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

March 1st, 2009 at 11:40 pm

I heard several times that Crocs were great shoes. I finally heard it enough that I bought a pair. They are great! So great that I wear them everywhere. Including to Iowa in January in snow. When I finally tried out a pair, I thought, "Why didn't I listen and take action earlier?"

I heard several times that iPods were incredible. I finally heard it enough that I bought one. It is incredible! So great that I wear it while running, driving, and sitting on an airplane. When I finally tried out a pair, I thought, "Why didn't I listen and take action earlier?"

"Why didn't I listen and take action earlier?" This is a question I have asked myself many times after discovering a new thing that enhanced my life greatly.

It applies to my finances. When I first prepared a Text is written spending plan and Link is http://nextsteps.iwasbrokenowimnot.com/tools/budgeting-tools/ written spending plan before the month and the money arrived, I asked myself this key question.

I wonder how many more things I should be listening to and taking action earlier?

I challenge you to ask yourself the same question.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

February 3rd, 2009 at 01:54 pm

I had the outstanding opportunity to go skiing on Friday before the Financial Learning Experience in Cheyenne, Wyoming.

I went skiing at Copper Mountain in Colorado, and it was INCREDIBLE! Over a foot of fresh snow over the past week had fallen, and the slopes were in terrific shape. It was the warmest day of the week (33 degrees) and sunshine too!

Here is a picture.

It was incredible, and I want to go back RIGHT NOW!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

February 2nd, 2009 at 09:42 pm

I recently spoke in Ottumwa, Iowa.

I was there to teach the Financial Learning Experience at Text is thebridge and Link is http://www.ottumwabridge.org/ thebridge church (pastor is Marty Schmidt).

I learned a lot about Ottumwa, Iowa.

* It is the hometown of Radar from M.A.S.H. and Tom Arnold

* It is about 1.5 hours south and east of Des Moines

* There is a huge need for financial training (just like all other areas of America!)

* I like Ottumwa

* It is home to a cool new church called "thebridge"

I also have realized that I have been living in the South for awhile. I showed up in Des Moines (8 degrees F and snow) wearing a light jacket, running socks, and Crocs.

Guess what? I was cold. Snow came in direct contact with my legs just above the ankles, and snow went right through the holes in the Crocs and soaked my socks.

So for those of you who were wondering: Crocs do not work well in snow.

It made me think about the number of times I have showed up ill-prepared to address financial issues. For example, I used to think that earning more money would solve my credit card balance and impulsive spending decisions. I was wrong. The fact was that I could earn millions of dollars a year, and I would still have an outgo problem.

I was ill-equipped. My monthly written spending plan using INCOME - OUTGO = EXACTLY ZERO was the correct tool to address my problem.

My Crocs have been replaced with nice leather waterproof shoes.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

2 Comments »

January 29th, 2009 at 08:49 pm

A person who recently attended a Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience e-mailed me the following question:

I had the privilege of hearing you speak both during the message and the class that followed. My wife and I are committed to eliminating our debt. With that in mind, I have a question. I have three credit cards one for 6,000.00, one for 1956.00 and one for 5775.00 I am paying high interest rates 27.98, 24.00 and 20.4% respectively.

I tried to reduce my rates, but they were unwilling and the reality is that I don't get [0%] offers in the mail anymore.

I responded with the following question: Have you applied for one of the cards on my "Next Steps" site [Text is HERE and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/0-credit-card-balance-transfers/ HERE]?

His response FIRED ME UP!

Here is his response.

I just applied for the discover card and I put two of the cards to be transferred totaling 11,500.00 and I was accepted! After talking to Bank of America earlier today I felt as if I were a heathen slug that had delinquent deadbeat written on my forehead and the reality was that I had always paid them!

Thank you. You will get my phone call with a loud yahoo! You have an awesome ministry keep up the good work.

So let's look at the math. $6,000 was moved from 27.98% and $5,500 was moved from 20.4%. That one move saved $205/month in INTEREST!!! That is over $2,400 per year in INTEREST that was eliminated.

If you are paying interest on a credit card, why?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

2 Comments »

January 20th, 2009 at 08:57 pm

I was able to achieve my goal of completing the marathon in under four hours!

I am PUMPED! More to follow in the next week on the similarities between finances and marathons.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

3 Comments »

December 31st, 2008 at 02:34 pm

The Federal Reserve Board has implemented some substantial rule changes that govern how credit card companies interact with cardholders.

I am PUMPED about some of the rules changes, but I am disappointed that most of these will not be implemented until July 2010.

Here are some rule changes that I am excited about:

* Double cycle billing is eliminated. This eliminates double-billing on interest (robbery).

* Can't raise rates unless payments are more than 30 days behind. Provides some margin for error before default rates go into effect.

* Payments will be applied to highest interest balances first. YAY!

And here is my personal favorite - No more universal default rules! This means that credit card companies can not raise your rate on a card that has been paid on time simply because you have paid late on another credit card!

You can read a complete article about the credit card lending rules at CNNMoney - Text is HERE and Link is http://money.cnn.com/2008/12/18/pf/credit_card_rules/index.htm?postversion=2008121817 HERE.

As a reminder, there is a way to prevent credit card companies from controlling your life - PAY THEM OFF!!! If you are carrying a balance on your credit card and are paying interest, it can be very worthwhile to transfer the debt to Text is 0% balance transfer credit cards and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/0-credit-card-balance-transfers/ 0% balance transfer credit cards so that ALL of your payment is applied to principal. PAY THEM OFF, and apply the first rule of holes - stop digging! No more debt.

Posted in

Uncategorized

|

1 Comments »

December 10th, 2008 at 03:50 pm

I love giving. Love it!

I have seen the the simple act of giving completely transform lives. My education is a direct result of GIFTS.

Purdue University

* My beloved university where I received my bachelor's degree in Mechanical Engineering (BSME) was founded through gifts.

* In 1862, President Lincoln signed the Morrill Land Grant Act that would give public owned land to any state that would use the land or proceeds from the sale of that land to found a college teaching agriculture and engineering.

* In 1869, Indiana signed on and accepted GIFT from John Purdue ($150,000 - in 1869! At 4% annual inflation, that equates to a gift of $38,614,733!). They also accepted a GIFT of $50,000 from Tippecanoe County (where Purdue is located) and 100 acres from local residents.

Clemson University

* The university where I received my masters degree in Business Administration (MBA) was founded through the same Morrill Land Grant Act!

* In Thomas Green Clemson's will, he bequeathed the Fort Hill plantation and a considerable sum from his personal assets for the establishment of an educational institution of the kind he envisioned.

Giving made my education a possibility. John Purdue, the residents of Tippecanoe County, and the local residents who donated land all made Purdue a possibility. Thomas Green Clemson made Clemson a possibility. Although the residents of Tippecanoe County who donated tax dollars and land are not mentioned, they are just as much a part of it as John Purdue and Thomas Clemson.

Key Lesson: GIVING allows me to make a difference in future generations.

Sources

* Purdue University web site

* Clemson University web site

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

December 9th, 2008 at 06:11 pm

I love filling in the squares on the Sangl Family Home Pay-Off Spectacular every month. It is so satisfying to visibly watch the debt leave.

Over the past year, we have developed an entire set of Text is Debt Pay-Off and Link is http://nextsteps.iwasbrokenowimnot.com/tools/pay-off-spectaculars/ Debt Pay-Off and Text is Saving Spectaculars and Link is http://nextsteps.iwasbrokenowimnot.com/tools/saving-spectaculars/ Saving Spectaculars. In fact, they have been downloaded thousands of times! That floors me.

I would love to hear your ideas on additional Spectaculars we can provide.

So … ask yourself the following questions:

What are you paying off? and What are you saving money for?

Put your suggestions in the comments below, and the team will work to provide spectaculars for them over the next several weeks!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

December 8th, 2008 at 01:57 pm

Marathon training is like planning.

I am currently training for a full marathon that I will run on January 18 in Houston, TX. I am neck deep in to the training plan right now, and there have been several times that I have asked myself, "WHY am I doing this? AGAIN?!!"

Since this is my second marathon, I am much more aware of the importance of good planning.

In my first marathon, I had a great training plan that I obtained from Text is HalHigdon.com and Link is http://www.halhigdon.com/ HalHigdon.com. He has training plans for all lengths and types of runs, but I pulled up the novice marathon training plan.

It was a great plan. It started out with moderate runs and slowly but surely it stretched out to longer runs. I remember specifically a day that the plan called for a twenty mile run. A twenty mile run. I was training in Indiana for the race, and it was horribly cold outside so I ran on a treadmill.

Shortly after I got on the treadmill, a young mother showed up and placed her baby in a car seat attachment next to her. She then proceeded to change the TV to "Bob The Builder". She ran for twenty minutes and then left me stranded there watching "Bob The Builder" - SIX STRAIGHT EPISODES!

After running for seventeen miles, I could not take "Bob The Builder" anymore so I got off the treadmill to go change the TV channel. I never got back on the treadmill. I never ran the other three assigned miles.

I ended up shortchanging one more twenty mile run that was on the plan.

Guess what happened? During the marathon, I ran great until mile 17. By mile 19, I was hurting so bad that I stopped and walked for awhile. I ran-walked the final 7.2 miles. I finished, but I really paid dearly for not following the plan.

Have you ever planned your spending and then failed to follow it? I know I have in the past. I made it through the month, but I paid dearly for not following the plan.

That is how marathon training is like … plannning.

Will Rogers said that "even if you are on the right track, you will get run over if you just sit there."

Text is Read Recent Posts and Link is http://iwasbroke.savingadvice.com Read Recent Posts

Posted in

Uncategorized

|

2 Comments »

December 4th, 2008 at 10:06 pm

I believe that the greatest economic stimulus package that could have ever been implemented is LOWER GAS PRICES.

Seriously. I believe that super-high gas prices forced people to trim their spending to essentials and to restructure their spending - including eliminating gas hogs. Now that gas prices have eased there is extra money each month.

I do not know about you, but I saw a ton of people at Wal-Mart on Black Friday shopping with cash.

The average American family is getting an extra $50 to $200/month simply because of lower gas prices. That equates to an extra $600 to $2,400/year.

What do you think?

Posted in

Uncategorized

|

4 Comments »

December 2nd, 2008 at 04:38 pm

I am PUMPED about 2009! This crusade takes tons of people to make it work, and I am so honored that so many of you have participated in or volunteered to serve at one our events.

Here are the cities that the crusade will be visiting in the first three months of 2009.

* January 17 & 18 Houston, TX

* January 24 & 25 Royersford, PA (Philly area)

* January 28 Ottumwa, IA (Des Moines area)

* January 31 & February 1 Cheyenne, WY

* February 7 & 8 Dallas, TX

* February 22 Canton, GA (Atlanta area)

* March 7 & 8 Acworth, GA (Atlanta area)

* March 12 & 15 Anderson, SC

* March 22 Lakeland, FL (Tampa area)

I am also stoked to see that the crusade will be traveling in ways that do not require me to travel! The Text is I Was Broke. Now I'm Not. Group Study and Link is http://groupstudy.iwasbrokenowimnot.com/ I Was Broke. Now I'm Not. Group Study is being implemented into small groups and medium size groups in dozens of churches.

That PUMPS ME UP! I am so honored that I get to serve so many people, churches, and businesses and be a part of life changing work.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

December 1st, 2008 at 02:01 pm

The IWBNIN Team is pumped to offer the following Christmas 2008 Special to those of you who are on this crusade to help others accomplish far more than they ever thought possible with their personal finances.

Through December 18th, you can purchase 10 copies of I Was Broke. Now I’m Not. for $100 and shipping is FREE! To purchase these materials, click Text is HERE and Link is http://www.josephsangl.com/2008/11/18/christmas-2008-special/ HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

0 Comments »

November 24th, 2008 at 01:49 pm

One of the most common questions I am asked is:

"Should I get a home equity loan to pay off all of my non-house debt?"

Here is my response.

I am not a big fan of consolidating one's non-house debt into a home equity loan. This is for several reasons, and I have outlined those reasons below.

* This is addressing a symptom, not the root cause. This question is usually motivated by our need for immediate action. It is the same motivation that causes us to purchase a car and finance it for five years.

* Borrowing from home equity makes it more difficult to sell the house. This is especially true in today's house market. There are a ton of people who now owe more on their house than it can be sold for. Consequently, they become trapped in the house.

* Changing spending behavior is a process. If one runs out and consolidates their debts, it might remove the urgency from the need to change spending behavior. Changing one's spending behavior takes time. I am convinced that if I had obtained a home equity debt consolidation loan in December 2002, I would not have changed my spending behavior. However, because it took fourteen months to address our debt, our spending behavior was completely changed. We have never looked back!

Having spoken with thousands of people and working one-on-one with nearly one thousand people in the past two years, I am convinced that obtaining a home equity loan is not the best way to eliminate debt. The most common result from obtaining a home equity loan is less equity in the house and the consumer debt shows back up because the spending behavior was not changed.

This is, in fact, my own story. I obtained a debt consolidation loan to move a pile of credit card and consumer debt to one payment. After paying $315.60 a month for an eternity, I wanted to celebrate, but I could not. Why? Because while I had finally paid off the debt consolidation loan, I had not changed my spending behavior and my credit card debt had grown back to more than I had consolidated in the first place!

What do you think?

Text is Read Recent Posts and Link is http://iwasbroke.savingadvice.com Read Recent Posts

Related Tools/Articles

* Text is Debt Elimination Tools and Link is http://nextsteps.iwasbrokenowimnot.com/eliminate-debt/debt-freedom-date/ Debt Elimination Tools

* Text is SERIES: "How To Pay Off Debt" and Link is http://www.josephsangl.com/category/series/how-to-pay-off-debt-series/ SERIES: "How To Pay Off Debt"

Posted in

Uncategorized

|

2 Comments »

November 6th, 2008 at 07:33 pm

I am a HUGE fan of savings. I used to live with an average bank balance of $4.13, and I thought that we were doing really good because we had paid all of the bills on time.

The fact was that every single time life happened, our finances were crushed.

So today's question is: "Are You Prepared?"

As I share in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not., my family has experienced its fair share of "life happens" events. Here are some of them.

* Hospital My daughter could not breathe and went to the emergency room.

* Car Part Repairs The car broke down. Multiple times. Repairs included power steering rack, AC failure, ignition switch, and water pump.

* Car Body Work The car was involved in an accident with our truck. Yes, one of us in our family was backing up the car and scraped it along the side of the truck. We also had a small fishing boat fall over and hit our car leaving a huge dent.

* Appliances The dryer died.

* Healthcare Jenn had to have major surgery in 2003. Just ten months later, she had to have major surgery again. In 2007, I had hernia surgery. Now, Jenn has just had surgery again.

* House Repairs We purchased a thirty year old house in 2007. It required lots of repairs. LOTS more than we originally anticipated.

* Emergency Trips For death in the family.

We have experienced lots of "life happens" events that have cost a ton of money. Before December 2002, we would have just pulled out the credit card to cover these types of events. Since December 2002, we have been prepared with a fully-funded emergency fund.

Are YOU prepared?

Posted in

Uncategorized

|

2 Comments »

September 17th, 2008 at 12:58 pm

I read Text is THIS ARTICLE and Link is http://money.cnn.com/2008/09/09/news/economy/cbo_budget_update/index.htm?cnn=yes THIS ARTICLE recently on CNN.com.

I am reminded yet again of why I am on this crusade.

In the United States, we are being taxed at the highest levels ever YET the government (people that WE elect) are spending it even faster.

Guess what? Whether you are dealing with four dollars, four million dollars, or four trillion dollars the fact remains that INCOME - OUTGO = EXACTLY ZERO.

Why don't we have a balanced budget that also has debt reduction in it?

I thought about this question for a few minutes, and here are some reasons I believe we do not have a balanced budget.

* It is hard to tell ourselves "No."

* It is even harder to tell others "No." Especially people we care about.

* There are a lot of good causes out there, and we want to fund all of them.

* Elected officials who cut spending for their district run a high risk of being run out of office.

* The "I'm going to put America on a budget." campaign speech is about as appealing as the spouse who announces "We're going on a budget." Instead of thinking "financial freedom" (that's what I think of when I hear the word "budget"), most people think "NO!", "No Fun!", and "Boring" and believe that it will be incredibly restricting, constricting, and beans & rice all of the time.

* Many people do not typically think toward the future. It takes time, effort, and organization to think about the future implications of such financial management. Many Americans are hugely short of time, effort, and organization.

What are you thoughts?

Posted in

Uncategorized

|

3 Comments »

September 15th, 2008 at 12:57 pm

For the past several weeks, I have had an overwhelming sense of thankfulness. I am so blessed that it is hard to put it into words.

Here are some random things for which I am thankful:

* My healthy family

* The opportunity to run a marathon - not everyone has the health to even attempt one

* An emergency fund and the peace it brings to my family

* Great friends - I have met so many cool people through this crusade to help others with their personal finances

* HOPE

* Opportunity

* My friend who was diagnosed with cancer has been given a clean bill of health

* Being able to participate in life-changing work and the FLE, FFE, IWBNIN, Money Help, and other resources that help make the life-change possible.

* Volunteers who help me with this crusade. There are literally dozens of people who make this thing work.

* NewSpring Church

* Two paid-for cars that run well.

* A wife who participates in the budgeting process.

As I look at this list, I realize that many of them are interconnected. Many of them could not exist alone. But I can tell you this, as I wrote this list, my heart overflows with thankfulness, and I am overwhelmed. I simply can not believe I get to do this stuff for a living.

If you were to take three minutes to write down what you are thankful for, what would you write?

Posted in

Uncategorized

|

2 Comments »

September 9th, 2008 at 05:42 pm

In keeping with the completely PRACTICAL nature of this website, I thought I would provide some important reminders.

* Christmas is 107 days away

* Car tires wear out

* Water heaters fail

* Kids grow

* Debt freedom is worth every sacrifice it took to achieve

* Third-graders will enter college in ten years

* Wives appreciate nice anniversary gifts - especially the years that have multiples of 5

* Property taxes are known, upcoming expenses for those who own property

* Income is necessary to make Income - Outgo = Exactly Zero

* Payday loans are destructive to one's finances

* Purdue University did not lose a football game last week

* It is now nine days into September. Did you prepare a written budget BEFORE the month began?

What other reminders do you have?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

1 Comments »

September 8th, 2008 at 02:59 pm

Pardon me while I rant for a moment �

For some reason, I have been encountering a lot of people lately who simply can not believe that they can become debt free.

They present numerous reasons as to why they can not become debt free - income, uncooperative spouse, children, huge home mortgage, student loans, interest rates on various loans, and the fact that it takes too long.

I agree that all of these reasons can create obstacles to achieving debt freedom, but NONE has the ability to prevent you from becoming debt free. ALL of them can be addressed. ALL of them might require tough, hard, and gut-wrenching decisions, but it is worth it to become free from debt!

If freedom from debt is your goal, you CAN do it! I believe that one of the most important things one can do when launching their Debt Freedom March is to prepare a written spending plan every single month.

If today is the day that you are going to start planning your spending, I recommend that you read the series of posts I wrote titled Text is "How Do I Budget?" and Link is http://www.josephsangl.com/category/series/how-do-i-budget-series/ "How Do I Budget?".

Chances are that if you have already launched your March To Debt Freedom, you have encountered the naysayers who say it is not possible. Stick with it! It is so worth it.

In summary, let me just say that I have been Debt-Free (Text is except for the house and Link is http://iwasbroke.savingadvice.com/series-home-pay-off-spectacular/ except for the house) and LOVING IT since February 2004.

Posted in

Uncategorized

|

0 Comments »

September 2nd, 2008 at 12:12 am

I am not sure why I am doing this again, but I have signed up for another full marathon. That is 26.2 miles of nonstop running. That is 26.2 MILES. That is a 10K race PLUS 20 more miles!

I decided to re-read Text is THIS POST and Link is http://www.josephsangl.com/2006/05/30/how-a-marathon-is-like-personal-finances/ THIS POST I wrote before I ran my first full marathon back in June 2006. I found myself saying "Amen." and "Absolutely." as I read that post. (Sidenote: Is it OK to do that for stuff you have written yourself?)

On Sunday, January 18, 2009 @ 7:00AM, I will embark on another marathon with 18,000 runners in the Chevron Houston Marathon in Houston, TX. The great thing is that I will have two brothers running with me (the other three are slackers). If, strike that, WHEN we all finish, we are going to Ruth's Chris Steakhouse for a fine celebration meal.

There are so many parallels between marathon training and personal finances. Not the least of which is self-discipline. Look for a ton of posts focused on my training and how I feel that it relates to personal finances over the next several months.

I have started training several months ago, but the formal training program begins September 15th.

I ran my last marathon in 4 hr 27 min 35 sec. My goal this time? 4 hr 10 min 00 sec

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive posts automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

August 31st, 2008 at 01:29 pm

Jenn and I budget every single month. We spend all of the money we expect to receive in the upcoming month in the Text is Monthly Budget Form (Excel) and Link is http://www.josephsangl.com/wp-content/plugins/download-monitor/download.php?id=1 Monthly Budget Form (Excel) and AGREE on how that money will be spent.

THAT is the easy part. The hard part is following the plan for the entire month - especially at the end of the month.

It is easy to follow the budget at the start of the month because I have spending money, we have grocery money, we have dining out money, and we have entertainment money.

But as we arrive at the end of the third week and the start of the fourth week, it is not so glorious of a picture. You can bet that I have spent every dime of my spending money. The dining out fund is at or near zero. The grocery envelope is tapped out, and the entertainment envelope has kicked the bucket as well.

That is our story nearly every single month of the 62 consecutive months that we have planned our spending. Yet we stick with the budget, and it is where I see a ton of people fall off of the wagon.

How do we ensure that we stick to our plan? We hold each other accountable. We KNOW that if we spend more than we planned on these fun categories, then that extra money will be taken from another fund like vacation, Christmas, car repairs, retirement savings, or college savings. We simply refuse to mortgage our future just so we can have a little extra fun today.

That is HOW we stick to our plan and that is WHY we stick to our plan.

I would love to hear from others on HOW you ensure that you stick to your plan and WHY. Start the conversation in the comments below!

Posted in

Uncategorized

|

2 Comments »

August 30th, 2008 at 11:59 pm

Many of you know that I have a house cat named Kiki. My daughter was given this nice kitty cat four years ago for Christmas, and it has been a great cat.

Until we moved back to South Carolina and bought an older home. An older home that used to have other animals in it. The smell of the other animals has ignited the stupid instinct to spray and mark its territory.

The cat has peed all over the tile floor of the laundry room. It has peed all over a box of shipping envelopes for my book. (Don't worry - I threw them away.)

It has pooped all over the new carpet. And we decided that the cat was going to get ONE MORE CHANCE to stop being instinctive with its pooping and peeing.

Well, it seemed as if our cat was behaving and things have went OK for a couple of months.

Let me stop that story to introduce a new storyline.

A new kitten showed up on our back deck two weeks ago. It was emaciated with its ribs sticking out and it had no tail. Melea immediately fell in love with it and started nursing it back to health. Me, being the sucker that I am, agreed that after a trip to the vet this new kitten could move in with us last Thursday.

Last Wednesday, the day before the kitten was going to move in, Jenn discovered that Kiki had been spraying FOR MONTHS in an undiscovered area. The undiscovered area? On our brand new carpet and TWO BOXES OF I Was Broke. Now I'm Not.!!!!!! Now, I know some budget-haters would love to do what Kiki has done, but THAT WAS IT.

Kiki has been kicked outside. The new kitten is not being allowed in the house. I wanted to see if Kiki could fly through the floor at a very high rate of speed, but I kicked her out instead.

In spite of ALL of that, this was still a very hard decision. You see, Kiki slept next to Melea every single night. Snuggled right up next to her, purring so nicely. Ever since Melea can remember, Kiki has been bounding around the house with her. Now, Kiki sits outside in tropical storm Faye, meowing forlornly and totally confused as to why she can not come inside.

In spite of the fact that the stupid cat had ruined two boxes of books. In spite of the fact that our new carpet smells like cat pee. In spite of the fact that it had sprayed an entire box of shipping envelopes. In spite of the tremendously annoying damage, it was still a very difficult decision.

It made me pause. This situation helps me understand just a little bit more why some people can not bring themselves to make the decisions necessary for them to win with their money. They KNOW that the car payments are peeing all over their ability to gain financial traction. They KNOW that the credit cards need to be chopped up because they are stinking up their ability to win with money. They KNOW that their finances are continually being trashed because they are unwilling to make a tough decision.

Folks - throwing out your eight year old daughter's cat is a difficult decision. So is selling a car and taking a second job. But I will tell you this - the relief I feel now that the decision has been made is AWESOME!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Posted in

Uncategorized

|

5 Comments »

August 11th, 2008 at 01:17 pm

I had an amazing Monday a week ago.

First, I had an incredible weekend teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE Details.htm Financial Learning Experience and the Financial Counseling Experience at NewSpring Church.

And then Monday showed up. As I walked out of the door, I saw a FedEx envelope wedged in the door. It said it was from "First National Bank". I was not expecting anything from FedEx, especially from a bank. Then I noticed that it was from First National Bank of Omaha. FNBO. As in FNBO Direct. As in the on-line savings account provider that is currently paying 3.50% interest.

Let me set this up before I tell you what was in the envelope.

A couple of months ago, a reader wrote me saying that I should enter a contest being sponsored by FNBO Direct called "Pay Yourself First". All I had to do was prepare a video that shared a major savings obstacle and why I was focused on paying myself first. I did that and uploaded it to YouTube as instructed. A few weeks later, I was awarded a $10 Amazon.com gift card for being one of the early entrants.

Well, here is where Monday and the FedEx envelope rolls in.

The letter inside stated that I have been selected as one of the twenty semi-finalists and that I have been awarded $500 for reaching the semi-finalist level! FIVE HUNDRED DOLLARS!!! I am BLOWN AWAY!

From the twenty semi-finalists, FNBO Direct will select five finalists who will compete in a six-month savings journey. FNBO Direct will match the savings dollar-for-dollar up to $5,000! FIVE THOUSAND DOLLARS! Are you kidding me?! I am so blessed. SO BLESSED.

You can check out my YouTube entry Text is HERE and Link is http://www.youtube.com/watch?v=m6TJVxmoj3g HERE. In the video, you will see/hear me mention the Sangl Home Pay-Off Spectacular. I am so focused on eliminating our mortgage that I provide monthly updates on our pay-off spectacular.

What a great Monday!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

4 Comments »

August 7th, 2008 at 03:45 pm

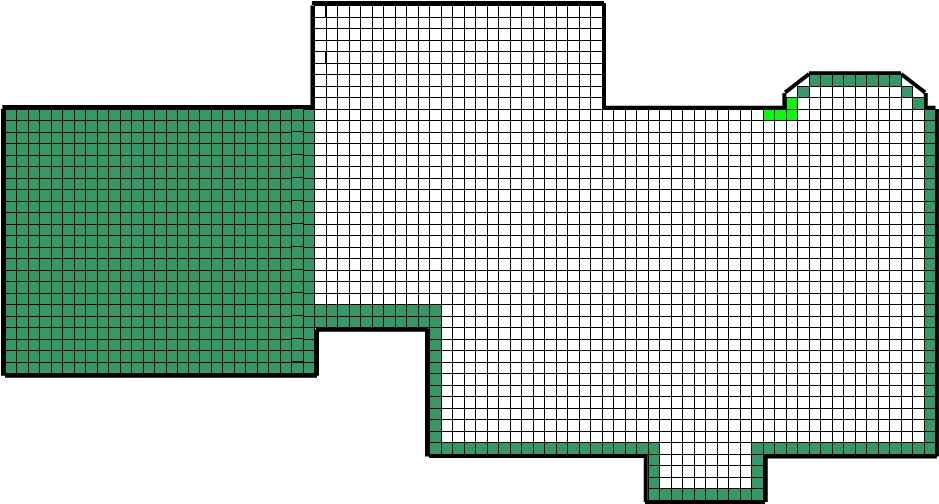

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 748 IS 752

Squares Remaining: WAS 1678 IS 1674

% of House Owned By The Sangl's: WAS 30.8% IS 31.0%

% of House Owned By Wells Fargo: WAS 69.2% IS 69.0%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

You can read about how Jenn and I stopped being broke and won with our money in Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

Posted in

Uncategorized

|

0 Comments »

August 6th, 2008 at 02:28 pm

After nearly two years of pursuing this crusade to help others accomplish far more than they ever thought possible with their personal finances I still can not believe I get to do this for a living!

In less than two years, this thing has went from a mere passion and a book manuscript to a full-service, full-tilt crusade.

If you are preparing to teach about personal finances at your church or business organization, I would love to be able to partner with you! It is my passion and call to help people win with their money. Why? Because when people are financially free they are much more likely to go do EXACTLY what they have been put on this earth to do!

This stuff FIRES ME UP!

Here are options that are available to help you implement a finance curriculum at your church or business.

* Speaking I love to speak and teach on personal finances. But be ready for a FIRED-UP, high-energy speech as I am more than a little PUMPED to teach people about money management. You can watch me speak Text is HERE and Link is http://www.josephsangl.com/hearsee-joe-speak/ HERE.

* Experiences Some call them classes. Others call them seminars. I call them experiences. Why? Because I teach PRACTICAL tools that can be immediately applied. I do not teach theoretical and hypothetical material. The tools that I teach are what Jenn and I personally did to win with our money. The two-hour experience is the most popular - Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience, but the six-hour Text is Financial Freedom Experience and Link is http://www.josephsangl.com/FFE%20Details.htm Financial Freedom Experience has been very successful too.

* Group Study Course This six session study is based on my book, I Was Broke. Now I'm Not. I have found that my home group is where I am challenged AND held accountable. Accountability is so huge when it comes to making the tough decisions that might be necessary to win with money. Find out more about the Group Study Text is HERE and Link is http://www.josephsangl.com/IWBNINHomeGroupStudy/IWBNINHGS.htm HERE.

* Financial Counseling Training In the Financial Counseling Experience, I train people to use the process that we have used here at NewSpring Church to provide one-on-one financial counseling to over 400 people each year! If you are interested in providing financial counseling, this is a great place to start! Since I am an engineer, you can bet that this training will involve a checklist or two.

* Personal Finance Book In I Was Broke. Now I'm Not., I share my family's story of walking out of financial mismanagement and into financial freedom. THEN I share exactly HOW we did it. I share exactly HOW to use the tools and all of the tools are available FREE through the web site. Find out more about the book Text is HERE and Link is http://www.josephsangl.com/iwasbroke/ HERE.

You can contact me Text is HERE and Link is http://www.josephsangl.com/about/ HERE.

I LOVE THIS STUFF!

Posted in

Uncategorized

|

0 Comments »

August 5th, 2008 at 01:50 pm

John Bartlett had some really kind words about Text is I Was Broke. Now I'm Not. and Link is http://www.josephsangl.com/iwasbroke/ I Was Broke. Now I'm Not.

I am so humbled by this type of feedback. I am a teacher through and through and any teacher will tell you that seeing others carry the message on to others is the ultimate compliment.

Thanks, John, for the kind words.

You can read his post Text is HERE and Link is http://barlaybrainstorm.blogspot.com/2008/07/goals.html HERE.

Posted in

Uncategorized

|

1 Comments »

August 3rd, 2008 at 10:17 pm

I had the opportunity to meet with Text is Chris Kakaras and Link is http://www.josephsangl.com/wp-admin/www.chriskakaras.com Chris Kakaras this week. He is a young man who is passionate about helping people manage their money God's way. One of the key groups that he speaks to are college students, and I had the opportunity to review some of his materials when we met.

There was a section of questions in his training that really caught my eye. It was good. Very good.

Here is one of the questions (participants in the class are required to answer these questions).

Did you eat today? YES NO

If YES is the answer, then you are blessed and have enough.

So basic, but SO TRUE!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

1 Comments »

July 31st, 2008 at 01:59 pm

I wonder how many people are currently at risk of having an article like Text is THIS ONE and Link is http://www.independentmail.com/news/2008/jul/24/anderson-woman-suffers-22k-loss-when-sock-stolen/ THIS ONE written about them?

This is why I am in favor of "cash envelopes" and not "cash socks".

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

July 29th, 2008 at 01:16 pm

Text is Tony and Link is http://www.tonymorganlive.com Tony has placed a picture of his desktop picture on his website with the question, "Does your desktop picture say anything about you?"

So I am posting my desktop picture to see if it says anything about me.

What do you think? Does my desktop picture say anything about me?

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

3 Comments »

July 28th, 2008 at 06:54 pm

I have written before about the fact that I have a thirty-year-old house that has thirty-year-old house problems. One of the problems is that the downstairs AC is the original AC for the house.

Problem 1 - January 2008

It was making a "banging" sound.

Diagnosis: Low on refrigerant - $75.

Problem 2 - May 2008

It was not cooling at all, and it was making a loud electrical "HUMMMMMMMM" sound.

Diagnosis: Condenser unit fan was not operating - $200+

Problem 3 - June 2008

It stopped cooling again. It was a day before vacation so I decided to have it looked at when I got back home two weeks later.

Diagnosis: Electrical wiring insulation had worn through and was shorting out the fan - $105

So we are back to enjoying the nice cool air conditioning in the dead-middle of a South Carolina summer.

I wonder when I will have to replace this unit? Part of me wants to bury my head in the sand and hope that it runs another thirty years. The realistic side of me says I should go ahead and start pricing out units. Initial looks have shown a cost of $5K - $7K. Just what I want to spend my money on � an air conditioner.

Why do I bring all of this up? Because it is so important to look ahead when preparing a financial plan. Jenn and I could pretend that this issue does not exist and then have a financial "emergency" when this AC really does fail permanently. In the past (when we were always broke), we would ignore this issue and then be surprised when it failed. Now, we recognize it as a known, upcoming expense, and we plan for it.

I do hope that it lasts another thirty years, though.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

|