|

|

|

|

Home > Archive: March, 2008

|

|

Archive for March, 2008

March 28th, 2008 at 12:40 am

Welcome to the latest series - "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One - What is a Mutual Fund?

This is THE number one question that I receive when I am teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience and Text is Financial Freedom Experiences and Link is http://www.josephsangl.com/FFE%20Details.htm Financial Freedom Experiences. Mutual funds can certainly sound confusing - especially when there are so many options available. So for those who do not know what a mutual fund is, let me explain it the best I know how.

If something has been FUNDED, it means that money has been given to it.

If you and I come to a MUTUAL agreement, it means that we both were involved in making the agreement.

So if you and I have MUTUALLY FUNDED a project, then it means that we both provided money for the project.

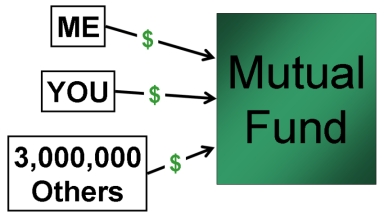

A MUTUAL FUND means that you and I have both put our money in the same place. It is not unusual for a mutual fund to have over 5,000,000 people MUTUALLY FUNDING the same investment.

So we have mutually funded an investment along with three or four million of our closest friends. The amount you have invested is different from how much I have invested, but it is all in the same place. I have drawn a picture to illustrate this. Please marvel at my graphic art skills.

So, we now all understand that we have mutually funded this investment and that it is called a mutual fund. The next question to answer is: "Where does the money go once it is in the mutual fund?"

Well, each mutual fund has a specific objective. Some mutual funds have an objective to produce income. Others have an objective to maximize the long-term growth of the invested money. Still others may have an objective to invest only in international companies. The bottom line is that each mutual fund has a specific objective or charter.

Based upon a mutual fund's charter, the mutual fund managers will purchase part-ownership in a lot of companies. I have employed my terrific graphics skills to illustrate this.

The Mutual Fund managers use the money provided by you, me, and three million of our closest friends to purchase ownership in anywhere from 50 to over 1,000 companies. As these companies earn profits and grow, the value of the investment grows. This means that each individual who owns a portion of the mutual fund can enjoy that growth as well.

So that is what a mutual fund is. I hope that it helped those who may have been confused. In the next part of this series, I will discuss how individual investment goals help guide one's mutual fund selection decisions.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

SERIES: Choosing Mutual Funds

|

0 Comments »

March 24th, 2008 at 12:38 pm

Just found out that my book, I Was Broke. Now I'm Not., is now available at Borders.com!

YAY!

So now, I Was Broke. Now I'm Not., is now available via �

Text is Borders.com and Link is http://www.amazon.com/s/ref=nb_ss_bgi/103-0843693-8655025?url=search-alias%3Dstripbooks&field-keywords=Joseph+Sangl&Go.x=0&Go.y=0&Go=Go Borders.com

Text is Amazon.com and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& Amazon.com

Text is Paypal and Link is http://www.josephsangl.com/IWBNIN%20Book.htm Paypal

Woohoo! By the way, if you want to read the Introduction you can click Text is HERE and Link is http://www.josephsangl.com/IWBNIN%20Book.htm HERE.

Posted in

Uncategorized

|

1 Comments »

March 23rd, 2008 at 08:22 pm

In Text is THIS POST and Link is http://www.josephsangl.com/?p=384 THIS POST back in August 2007, I shared several of the mutual funds that I own. A quick glance will reveal the name "American Funds" six times in my mutual fund portfolio. Why do I own them? Because they had great track records and lower ongoing management fees than most of their peer mutual funds.

Image borrowed from www.AmericanFunds.com

However, American Funds mutual funds are front-end loaded mutual funds. A load means that there is a sales charge to purchase a share of the mutual fund. If one is just getting started out, there is a 5.25% sales charge. This means that if you have a $100 bill to invest, only $94.75 will make it to the mutual fund. Which is annoying.

BUT, I still invested in American Funds' mutual funds because they simply had great track records.

So, as I was reading CNN's Personal Finance web site, I was very interested to read an article titled "Text is Are American Funds A Good Buy? and Link is http://money.cnn.com/2008/03/18/pf/funds/Ask_the_mole.moneymag/index.htm?postversion=2008031910 Are American Funds A Good Buy?"

Very interesting.

By the way, I don't sell mutual funds or ANY investment product. I DO sell copies of my book, I Was Broke. Now I'm Not. I truly believe that the information in this book will help you take control of your finances and achieve financial freedom. You can purchase a copy via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL or Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

Uncategorized

|

0 Comments »

March 22nd, 2008 at 04:16 pm

Welcome to the latest series on this wildly popular website. With this series, I will be sharing how you can use some of the calculators from the " Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" page to take your financial plan to the next level.

A mortgage or real estate loan is really the only type of debt that I can tolerate (barely), so here is another FREE tool from the "TOOLS" section of the web site.

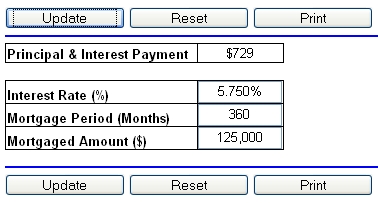

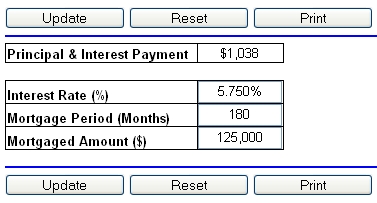

To calculate your principal and interest mortgage payment (does NOT include any escrow such as PMI, property taxes, HOA Fees, or hazard insurance), you will need to know three things.

1. Interest Rate

2. Mortgage Period

3. Mortgaged Amount

If you want to calculate the monthly principal & interest payment for a fixed-rate 5.750%, thirty-year $125,000 mortgage, pull up the "Text is Mortgage Payment Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Mortgage%20Payment%202007-02-21.htm Mortgage Payment Calculator".

Suppose you want to understand what the P&I payment would be for the same mortgage, but for a 15-year term. Change the mortgage period to 180 months.

The payment goes up $309/month, but one will become debt-free FIFTEEN years sooner!

One could also use this calculator when considering refinancing.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

SERIES: TOOLS

|

0 Comments »

March 22nd, 2008 at 02:52 am

CNN posted Text is THIS ARTICLE and Link is http://money.cnn.com/2008/03/17/pf/taxes/rebates_payment_schedule/index.htm?postversion=2008031713 THIS ARTICLE that shows the dates that the IRS will be shipping out the Economic Stimulus Payments.

Not sure what to do with your rebate check? Consider reading the "Text is Best Utilize Your Tax Refund and Link is http://www.josephsangl.com/?cat=26 Best Utilize Your Tax Refund" series at www.JosephSangl.com.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

Uncategorized

|

0 Comments »

March 20th, 2008 at 12:46 pm

Welcome to the latest series on this wildly popular website. With this series, I will be sharing how you can use some of the calculators from the " Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" page to take your financial plan to the next level.

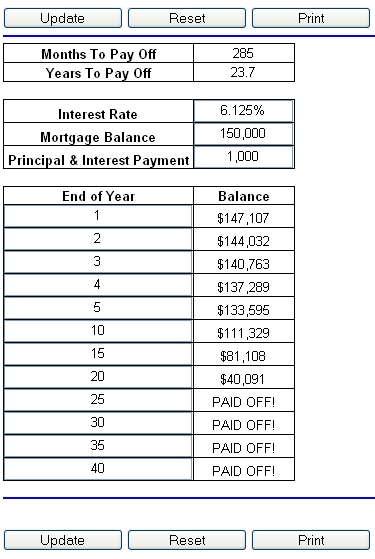

I remember the first day that I put together my "Text is Sangl Family Home Pay-Off Spectacular and Link is http://www.josephsangl.com/?cat=16 Sangl Family Home Pay-Off Spectacular". I realized just how little of my home I actually owned! When the question was asked of me, "Are you a homeowner?", I could no longer answer, "Yes." Wells Fargo was my homeowner!

With that realization, I decided to pay off my mortgage early. And, God-willing and if the creek doesn't rise, Jenn and I will pay off our house in two years and nine months. How do I know that? Because of another FREE tool on this wildly popular website!

The tool is called the "Text is Early Pay-Off Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Debt%20Pay-Off%20Calculator%202007-11-28.htm Early Pay-Off Calculator".

Here is how it works. You need to know three things to use this calculator.

1. Mortgage interest rate

2. Mortgage balance

3. Amount of principal & interest payment that you will be paying (don't include the escrow!)

Let's say that one has a thirty-year mortgage with a $150,000 balance and a 6.125% fixed interest rate and a $911/month principal & interest payment.

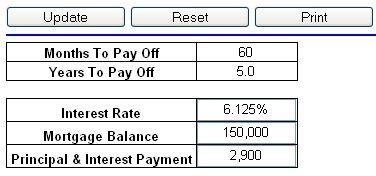

Suppose you want to know what a monthly principal & interest payment of $1,000 will accomplish. Use the "Text is Early Pay-Off Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Debt%20Pay-Off%20Calculator%202007-11-28.htm Early Pay-Off Calculator" to calculate it for you!

Just by paying $89/month extra, the thirty-year mortgage will pay off 6.3 YEARS sooner! How awesome is that?!

One item to note is to designate all extra money to be applied to "principal reduction"! Some of the sly mortgage companies will attempt to apply it to "prepaid interest". That would be a bank error in their favor! Make sure that all extra money is applied to your mortgage principal.

What if the above mortgage holder wanted to pay off their mortgage in five years? You can use the calculator to find out how much would need to be sent each month.

For the low-low price of $2,900 each month, the mortgage will leave in just FIVE years! Can you do that?

Let me ask you another question, if you were debt-free except for the house, could you do this? It is amazing what you can accomplish when you are not bound up in debt!

How early will you pay off your mortgage?

Oh, by the way, you can use this calculate to calculate the early pay-off of ANY type of loan!

In the next part of this series, I will be sharing how you can calculate your mortgage payment.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

SERIES: TOOLS

|

0 Comments »

March 19th, 2008 at 01:43 pm

Welcome to the latest series on this wildly popular website. With this series, I will be sharing how you can use some of the calculators from the " Text is TOOLS and Link is http://www.josephsangl.com/?page_id=151 TOOLS" page to take your financial plan to the next level.

In the Text is last post and Link is http://iwasbroke.savingadvice.com/2008/03/18/tools-calculate-amount-needed-for-retire_36770/ last post, I shared how you can calculate the amount you need to save for retirement.

For many people, the number revealed by completing the retirement nest-egg calculation leads to an "Oh Crap" Moment, but it is usually easier to achieve than one would initially think.

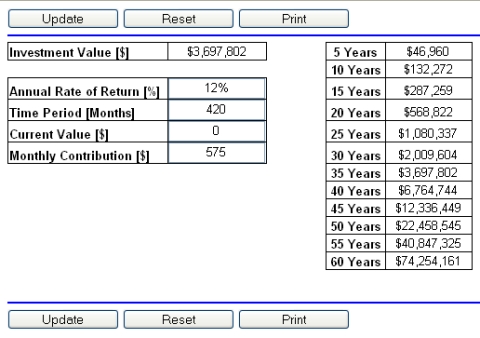

Introducing another great tool available via the "TOOLS" link at the top of the page � the Text is Investment Value Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Investment%20Value%202007-02-21.htm Investment Value Calculator.

In the previous post, I calculated that one would need $3,699,458 to receive the equivalent of $75,000 per year upon retirement in 35 years.

The immediate next question is "How much do I need to invest each month to achieve $3,699,458 in 35 years?"

Using the Text is Investment Value Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Investment%20Value%202007-02-21.htm Investment Value Calculator, I can quickly calculate the number.

If one has not started investing, then $575 needs to be invested every single month with an annual return of 12% to achieve the goal.

Isn't that cool? I LOVE this stuff! For just $6,900 per year, one can ensure a secure non-Social Security-reliance retirement!

What is your number?

In the next post, I will be sharing about another tool that shows you how extra money toward your mortgage each month reduces the life of that mortgage!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

My first book, "I Was Broke. Now I'm Not.", was released on January 20th. It is available via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL or Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.

Posted in

SERIES: TOOLS

|

1 Comments »

March 18th, 2008 at 03:05 pm

Welcome to the latest series on this wildly popular website. With this series, I will be sharing how you can use some of the calculators from the "TOOLS" page to take your financial plan to the next level.

One of the things that I do as part of both of the classes that I teach is to have people calculate how much they will need to retire well.

The calculation usually yields what I call an "Oh crap!" Moment with the majority of folks responding with "YIKES!" and "Oh no!".

I have people calculate this number for the following reasons:

1. Most people have never seen how much they will need to retire well.

2. When people realize how large the number is, it helps them realize how important it is to have a solid plan.

3. It hammers home the point that investing needs to start early and often.

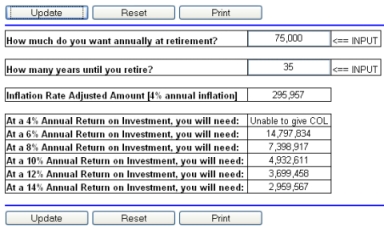

So, how much DO you need for retirement? Well, it is really simple to calculate with the Text is Retirement Nest-Egg Required Calculator and Link is http://www.josephsangl.com/wp-content/uploads/Tools/Calculator%20Retirement%20Nest%20Egg%20Required%202007-02-21.htm Retirement Nest-Egg Required Calculator.

Here are couple of things to note about this retirement calculator

1. This calculation assumes that you will never touch the principal.

2. This calculation assumes that you will give your nest-egg a "cost-of-living-raise" of 4% each year.

3. This calculator adjusts the "annual amount you want" for average annual inflation of 4%.

Below is a calculation I ran for an "annual amount I want" of $75,000.

Note that the calculator shows that with 4% annual inflation, I will need $295,957 per year in 35 years to have the same purchasing power that $75,000 has today.

If I expect my retirement nest-egg to grow at an annual rate of 8%, then I will need $7,398,917 when I retire. If I expect my retirement nest-egg to grow at an annual rate of 12%, then I will only need $3,699,458.

So � What's your number?

In the next post, I will share a tool that helps you determine the amount you need to save each month to fully-fund your nest-egg.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Automatically receive each post in your Text is E-MAIL and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US E-MAIL

Posted in

SERIES: TOOLS

|

0 Comments »

March 17th, 2008 at 01:50 pm

I love hearing the success stories of those who have had their Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment and began the journey to debt freedom!

Would you take the time to inspire others with your success story? Click the blue "Success Stories" box on the sidebar and share your story. While you are there, check out some of the other stories that have been shared!

I (and the readers) want to hear YOUR success story and celebrate with you - no matter how large or small!

Best story shared by Wednesday receives a FREE copy of "I Was Broke. Now I'm Not." (available via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL or Text is AMAZON and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON)!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 14th, 2008 at 01:15 pm

I will be saving a ton of money by following the advice of the Text is Coupon Mom and Link is http://www.couponmom.com Coupon Mom!

I recommend you click on the YouTube link on the first page of Coupon Mom's web site to see how it works.

Genius!

Posted in

Uncategorized

|

0 Comments »

March 12th, 2008 at 12:39 pm

I had a BLAST sharing my story at the three Sunday morning services at Text is Hyde Park Baptist Church and Link is http://www.lovinglumberton.com/templates/cushydepark/default.asp?id=21533 Hyde Park Baptist Church in Lumberton, NC this past weekend! After speaking on Sunday morning, Pastors Dennis Harrell and Text is Mike Pittman and Link is http://wholeheartedlife.typepad.com/ Mike Pittman had everything ready to roll for the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience to launch on Sunday afternoon.

We had a fantastic turnout and the audience was ENTHUSIASTIC (to say the least!) about putting together a plan that enables them to go do EXACTLY what they have been put on this earth to do! That FIRES ME UP!

Thanks Hyde Park! You can read what Mike had to say about the weekend Text is HERE and Link is http://wholeheartedlife.typepad.com/wholeheartedlife_dot_com/2008/03/sunday-nite.html HERE and Text is HERE and Link is http://wholeheartedlife.typepad.com/wholeheartedlife_dot_com/2008/03/really-proud-of.html HERE.

With that, I am PUMPED to announce the next two month's upcoming events!

Text is FLE and Link is http://www.josephsangl.com/FLE%20Details.htm FLE (2 hour class) & Text is FFE and Link is http://www.josephsangl.com/FFE%20Details.htm FFE (6 hour weekend conference OR 5 week class)

March 13, 2008 Text is NewSpring Church UNLEASH CONFERENCE and Link is http://www.newspringonline.com/245602.ihtml NewSpring Church UNLEASH CONFERENCE Anderson, SC

March 14 & 15, 2008 FFE Text is 5 Point Fellowship and Link is http://www.5pointfellowship.org/ 5 Point Fellowship Easley, SC

All Tuesdays in April FFE Text is NewSpring Church and Link is http://www.newspring.cc NewSpring Church Anderson, SC

April 4 & 5, 2008 FFE Text is Cornerstone Community Church and Link is http://www.mycornerstone.org/index.php?pr=Home Cornerstone Community Church Galax, VA

April 16, 2008 FLE Text is Oak Leaf Church and Link is http://www.oakleafchurch.com/ Oak Leaf Church Cartersville, GA

April 20, 2008 FLE Text is Fusion Church and Link is http://www.createfusion.com/ Fusion Church Suwanee, GA

May 4, 2008 FLE Text is Avalon Church and Link is http://www.avalonchurch.net/ Avalon Church McDonough, GA

I am FIRED UP! Lives are being changed, and I get to be a part of it! Can I just say (again) that I am so glad I was able to fire myself from Corporate America and go do this?

I would love to take the crusade to California, Texas, New York, and Wyoming. If you are interested in having me speak, contact me by clicking Text is HERE and Link is http://www.josephsangl.com/?page_id=2 HERE.

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 11th, 2008 at 01:53 pm

There was a time when I was not passionate about my job. There used to be a time where I went to work at a J.O.B every day and wondered what I was put on earth to do.

Ever been there? It is not fun to go through such times, but I have found that it was absolutely necessary for me to go through that time to be adequately prepared for "what was next".

When you have been through the passionless, listless, awful, and confusing times, you can truly understand how awesome it is to a have a clear, unmistakable, resounding call on your life.

My calling became immensely clear as I began to take real action to improve my financial condition. As Jenn and I broke free financially, it was as if cataracts fell off of my eyes. I saw how huge and real the financial burden was for the majority of my neighbors, co-workers, friends, and family. I saw how huge the problem was for all of America! I simply couldn't take it anymore. I HAD to do something. In fact, the day that I announced that I had fired myself from Corporate America I wrote Text is THIS POST and Link is http://www.josephsangl.com/?p=116 THIS POST which really captured what I was feeling at that decisive moment.

Reading that post from eighteen months ago really brings the emotion of the moment back to me.

Here is why I do what I do �

* Person 1 - Put together a written plan, became debt-free, and is going on a cash paid-for-in-advance vacation to Europe this summer!

* Couple 2 - Put together a written plan, sold the fine luxury car, and will be debt-free before the end of the year. Yes, he cried when the Jaguar left (I would too!), but it is just a car.

* Person 3 - Put together a written plan and will become debt-free in less than HALF the time calculated using the Debt Freedom Date Calculator!

* Couple 4 - Put together a written plan, and are now able to give faithfully to their local church for the first time in their lives!

* Couple 5 - Put together a written plan, built an emergency buffer fund, and are now experiencing a job lay-off - BUT they have savings to help them weather the storm! They have PEACE even in the midst of this issue.

* Person 6 - Put together a written plan because his gift to his bride on their wedding day is for BOTH of them to be 100% debt-free. On the day they are married!

* Couple 7 - Put together a written plan, they will become debt-free before their children start college AND be able to pay for their children's college - something they did not even think was possible! But it was - and is!

* Couple 8 - Did not do so well with money management the first thirty years of marriage, but now have a written plan that will allow them to retire with ZERO debt and with SOME retirement savings - way ahead of what they thought was possible.

* Person 9 - Has always had a written plan, and is flat killing it - but he is buying tons of copies of I Was Broke. Now I'm Not. for his friends and family to ensure they also learn how to win!

* Couple 10 - Put together a written plan, and it has ROCKED their marriage (in a great way!) - it is the first time they have ever talked about money - let alone have a plan they both agree on! (Why do I hear Barry White singing?)

Those are just some of the HUNDREDS of stories of life change that FIRE ME UP! They are THE REASON I do what I do.

I can't believe I get to do this for a living! I am truly living a dream!

Text is Read recent posts and Link is http://iwasbroke.savingadvice.com Read recent posts

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

March 11th, 2008 at 12:05 am

I have the great opportunity to help hundreds of people put together a great financial plan.

Something that has been rocking my world lately is the frequency that I hear the following statement during my meetings �

"My parents - UGH! They are terrible with their money."

Is that your story?

One thing that I have learned from my hero, Text is Dave Ramsey and Link is http://www.josephsangl.com/?p=389 Dave Ramsey, is to listen to HOW people say things. To hear the tone in which it is said. To listen to what is being left unsaid.

What do I hear? Regret. Disappointment. Sadness. Shame. Discouragement. Frustration. Anger.

Here is what I can say for certain. HOW you manage your money WILL impact your children!

Proverbs 22:6 comes to mind - "train a child in the way he should go �"

So does Proverbs 13:22 - "A good man leaves an inheritance for his children's children �"

Are you ashamed of your parent's financial management? Resolve to break the cycle with your family.

Are you ashamed of your own financial management? It's time to have your IHHE Moment and change the story!

You CAN do this! I believe in you.

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

2 Comments »

March 7th, 2008 at 01:27 pm

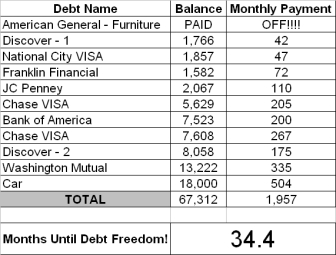

I am excited to introduce Couple #3 - the newest members of the "Marching To Debt Freedom" crusade.

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

What went well this month �

We transferred our Bank of America card balance to another card at a much lower interest rate. We also got the interest rate reduced on one of the Discover cards. We "spent" our tax refund before we actually received it, and it went much further! Half of it funded our emergency fund which is now over $2,900!

What were the challenges/struggles this month �

Not really any this month � except we want it all paid off!

Updated Debt Freedom Date �

Sangl Says �

I am excited about the progress of Couple #3! One debt is already paid off, and more are getting ready to fall! It is AMAZING how fast debt can leave when you have your IHHE Moment!

I challenge everyone to seek lower interest rates on any debt you are carrying. Many times you can obtain a lower interest rate just by calling your credit card. Or you can avoid the conflict altogether by rolling the balance over to a "0% for 12 months" card.

Readers �

Will you take a moment to leave a comment for Couple #3 and thank them for sharing their personal financial information with everyone? It takes a lot of courage to do this, and I am PUMPED to watch this debt fly away!

Read the Debt Freedom March updates for Text is Couple #1 and Link is http://www.josephsangl.com/?cat=19 Couple #1 and Text is Couple #2 and Link is http://www.josephsangl.com/?cat=20 Couple #2

Want to start your own Debt Freedom March? Check out the free tools Text is HERE and Link is http://www.josephsangl.com/?page_id=151 HERE. My book also teaches you how to use all of the free tools. You can purchase your copy at Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM or via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL!

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

1 Comments »

March 6th, 2008 at 06:22 pm

Introduction

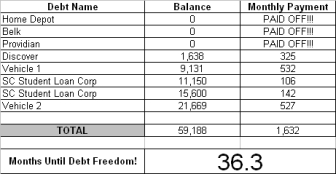

This couple is THROUGH with debt! It has now been five months since they announced that they were breaking up with debt.

Here is this month's update!

What went well this month �

Things are going great, and we are sticking to the plan.

Challenges and struggles this month �

I really don't have anything different to say as far as the challenges and struggles for this month.

Here is their updated Text is Debt Freedom Date calculation and Link is http://www.josephsangl.com//?page_id=151 Debt Freedom Date calculation �

Month By Month Progress �

What are the biggest changes you have seen as a result of the first six months of this march �

The biggest changes we have seen as a result of the first six months of this debt freedom march is that we don't take our money for granted anymore. Before we met Joe we spent our money very foolishly and unconsciously. As a result, we are still paying for our past purchases today (aka: DEBT!). We appreciate our money now and make it a point to think about each purchase we make. I have to say, the march to debt freedom is one of the best things we have ever done. We have not accumulated any new debt and we are well on our way to paying off what we owe.

I am very proud of my husband and myself and extremely thankful for Joe and his brilliant plan. We really started this year off right. As of right now we have a plan for just about everything; Christmas, vacation, vehicle maintenance, taking care of the yard for Spring & Summer, car insurance, car taxes, pet care, birthdays, holidays, etc. Knowing we have the money set aside to take care of the "known upcoming expenses" takes a lot of stress off of us each month. There are no surprises!!

Overall, it feels great knowing we have a plan. This makes us feel in control of our money and our future. If there is anyone questioning whether or not to give Joe a call, please do not hesitate. If I had one regret it would be that we did not meet with Joe and start our journey to debt freedom sooner!!!!!

My husband and I want to say Thank You to Joe for all of his encouragement and support. He has been a wonderful blessing to us and our future. God Bless You, Joe!!

Sangl says �

[BLUSH] I am humbled by the kind words that Couple #2 has shared. All I did was show Couple #2 the tools that I used to become financially free. They have taken it to heart, and I can not wait until I receive an invitation to their debt freedom party. My prediction is that this couple will be debt-free (except for the house) in 24 months or less. I know. I know. The Debt Freedom Date Calculation says 36.3 months, but I have seen way to many people who have had their IHHE Moment. They become debt-free way sooner than the calculation.

Way to go Couple #2!

Readers �

Everything I taught Couple #1 and Couple #2 and thousands of others is in my newly released book, I Was Broke. Now I'm Not. It can be purchased via Text is PayPal and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PayPal or Text is Amazon. and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& Amazon. It is NOT rocket science. I wrote this book in such a way that it can be read in less than 1.5 hours and can be immediately applied to your financial situation.

Would you share with Couple #2 how their sharing of their personal financial situation is inspiring you?

Text is Read Previous Updates For Couple #2 and Link is http://www.josephsangl.com//?cat=20 Read Previous Updates For Couple #2

You can receive each post via E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE!

Posted in

Uncategorized

|

0 Comments »

March 5th, 2008 at 01:29 pm

Introduction

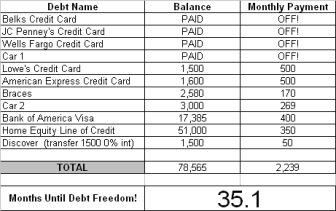

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now SIX months into their march. Here is this month's update.

What went well this month �

WOW! This is like when you can fit into your skinny jeans again. God blessed us and sent us a bonus check and instead of blowing it, I put it to good use. I paid off my car, and paid $3,000.00 on the other car. I am stoked! In about three months, I will be shed of all debt except the big stuff. We are also getting a tax refund, and I am hurling that at debt too. I feel like David reaching for the stones, baby!

What were the challenges/struggles this month �

The only struggle is feeling guilty because we did not do this early on. I would be a freaking gazillionare by now. God rocks. Joe rocks. Not being broke rocks. Yee Ha!

What are the biggest changes you have seen as a result of the first six months of this march �

This has made us focus like a laser beam on our finances - both good and bad. It has let us have a glimpse of what life will be like with no debt, and I like it. I can only wish that anyone who reads this takes it to heart. Don't let credit cards ruin your happiness. I will always remember my Text is IHHE Moment and Link is http://www.josephsangl.com/?p=488 IHHE Moment!

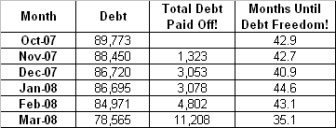

Updated Debt Freedom Date �

Month By Month Progress �

Sangl Says �

ANOTHER DEBT IS GONE! Couple #1 has definitely had enough. Look at the progress they have made in just six months! Their initial Debt Freedom Date calculation was 42.9 months. They are now down to 35.1 months AND they have avoided all new debt. They had to slow down during Christmas so that they could avoid debt that month, but it allowed them to stay on the path toward financial freedom. In just six months, Couple #1 has made FOUR different debts leave their life!

Way to go, Couple #1! I am FIRED UP by the progress you guys are making!

Readers �

How are you doing on YOUR debt freedom march? You can do this!

Read Previous Monthly Updates For Couple #1 Text is HERE and Link is http://www.josephsangl.com//?cat=19 HERE

Like what you are reading? Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE.

Posted in

Uncategorized

|

0 Comments »

March 4th, 2008 at 02:52 pm

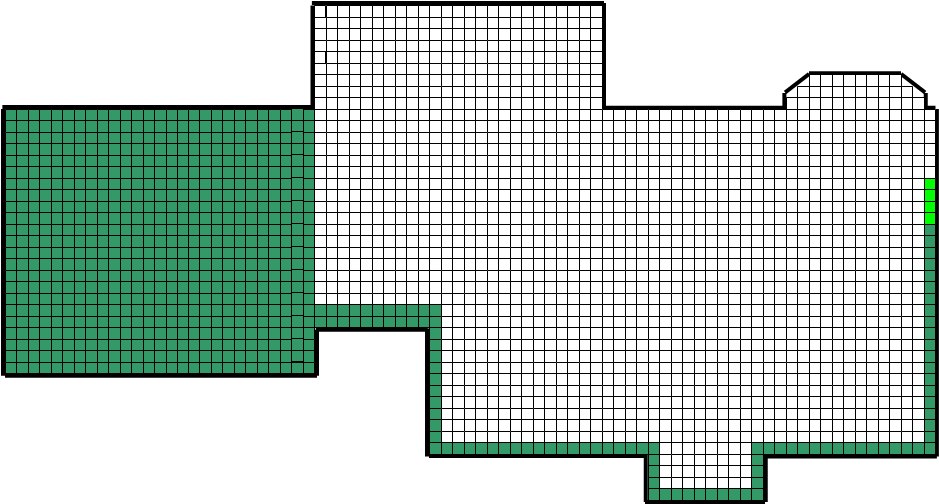

Every month there will be an update of Joe & Jenn's Home Pay-Off Spectacular! The fifth monthly update is TODAY!

Here's this month's update!

Total Squares: 2,426

Paid-For Squares: WAS 727 IS 731

Squares Remaining: WAS 1699 IS 1695

% of House Owned By The Sangl's: WAS 30.0% IS 30.1%

% of House Owned By Wells Fargo: WAS 70.0% IS 69.9%

Here is the updated "Sangl Home Pay-Off Spectacular" (Click on the picture to view the larger version)

Yes. We slowed down this month. We have some known, upcoming expenses approaching, and we are slowing down for a short period of time. One of the most essential things that I have learned about money is that there WILL be known, upcoming expenses and they WILL come due. Jenn and I are ensuring that we are more than prepared for these expenses.

By the way, we are STILL committed to paying the mortgage off by October 2011 with the same stretch goal of October 2010!

Read previous Sangl Home Pay-Off Spectacular Updates Text is HERE and Link is http://www.josephsangl.com//?cat=16 HERE

Get your own Debt Pay-Off Spectacular Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE and join the FUN!

Already debt-free? Get your own SAVINGS Spectaculars Text is HERE and Link is http://www.josephsangl.com//?p=442 HERE.

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Posted in

Uncategorized

|

0 Comments »

March 2nd, 2008 at 09:53 pm

I had a blast carrying the crusade over to Text is Gateway Community Church and Link is http://www.gatewaycommunity.cc/ Gateway Community Church in Goldsboro, NC this weekend!

Pastor Text is Thayer Stamper and Link is http://www.virb.com/thayer/blog Thayer Stamper, David Morrow, and the entire team at Gateway made the Text is Financial Freedom Experience and Link is http://www.josephsangl.com/FFE%20Details.htm Financial Freedom Experience a first-class event!

It took less than one hour to be completely set up for the event and at 6:30PM Friday evening, the FFE launched. It was awesome!

Here is what I LOVE about teaching this material - lives are changed every single time! There were tears and laughter as we progressed through the FFE, but more than anything else HOPE was restored, marriages were encouraged, and dreams were brought front and center.

Every time that I teach, I start and end with stating my passion �

To help others accomplish far more than they ever thought possible with their personal finances. Why? Because when people are financially free they are much more likely to go do EXACTLY what they have been put on this earth to do - Regardless of the income potential!

Gateway CC - Thanks for allowing me the opportunity to do do EXACTLY what I have been made to do!

This coming weekend, the crusade will continue on to Lumberton, NC where I will be speaking during the Sunday morning services at Text is Hyde Park Baptist Church and Link is http://www.lovinglumberton.com/templates/cushydepark/default.asp?id=21533 Hyde Park Baptist Church and then teaching the Text is Financial Learning Experience and Link is http://www.josephsangl.com/FLE%20Details.htm Financial Learning Experience in the afternoon. I can't wait!

Text is Read recent posts by Joe and Link is http://iwasbroke.savingadvice.com Read recent posts by Joe

Receive each post automatically in your E-MAIL by clicking Text is HERE and Link is http://www.feedburner.com/fb/a/emailverifySubmit?feedId=1041637&loc=en_US HERE

Purchase my book on Text is AMAZON.COM and Link is http://www.amazon.com/dp/1605301906?tag=wwwjosephsang-20&camp=0&creative=0&linkCode=as1&creativeASIN=1605301906&adid=0204PMQZ57FG83VXGHMA& AMAZON.COM or via Text is PAYPAL and Link is http://www.josephsangl.com/IWBNIN%20Book.htm PAYPAL.

Posted in

Uncategorized

|

1 Comments »

|